As the summer season arrives and millions of Americans head to beaches, parks, and backyards to enjoy the quintessential tradition of a cold beer, most consumers remain blissfully unaware of the complex financial machinery operating behind the scenes of their favorite beverage. While the cost of barley, hops, yeast, water, and labor are standard variables in any product’s price, there is one “ingredient” that consistently outpaces them all: government taxation.

In the United States, the beer industry operates within a labyrinthine regulatory and fiscal landscape. When a consumer reaches for a six-pack, they are participating in a transaction that is, in many cases, heavily subsidized by taxes. In some instances, the cumulative tax burden—ranging from federal excise taxes to local municipality levies—can account for as much as 40.8 percent of the final retail price.

The Anatomy of the Beer Tax Burden

To the average shopper, a beer receipt looks straightforward: the price of the product plus a standard sales tax. However, this is an illusion of simplicity. The majority of taxes levied on beer are "baked in" to the wholesale and retail price. These are excise taxes—mandatory charges imposed on specific goods—that are collected at the manufacturing or distribution level. Because these costs are passed down the supply chain, the consumer pays them indirectly without ever seeing a line item on their receipt.

The federal government sets the baseline, with excise tax rates ranging from $0.113 per gallon for small domestic craft brewers to $0.581 per gallon for imported beer. However, the true complexity emerges at the state and local levels. Every one of the 50 states, plus the District of Columbia, imposes its own unique excise tax structure. When these are combined with local sales taxes, bottle fees, and ad valorem (value-based) taxes on wholesalers, the price of a pint becomes a reflection of regional fiscal policy rather than just market demand.

A Chronology of Fiscal Fragmentation

The history of beer taxation in America is one of layering. Initially, excise taxes were straightforward flat rates. Over the decades, however, states began to diversify their revenue streams, leading to the current fragmented environment.

The Rise of Complexity (20th Century)

Following the repeal of Prohibition, states were granted significant latitude to regulate and tax alcohol. This led to a patchwork of "dry" and "wet" counties, varying licensing requirements, and disparate tax codes that persists to this day. Throughout the 1990s and 2000s, many states began to use alcohol taxes as a "sin tax" mechanism, intended both to raise revenue and discourage consumption.

The Modern Era of Divergence (2010–2025)

In recent years, the trend has shifted toward volatility. Some states have attempted to modernize their codes to account for the explosion of the craft brewing industry, while others have doubled down on protectionist or revenue-generating measures.

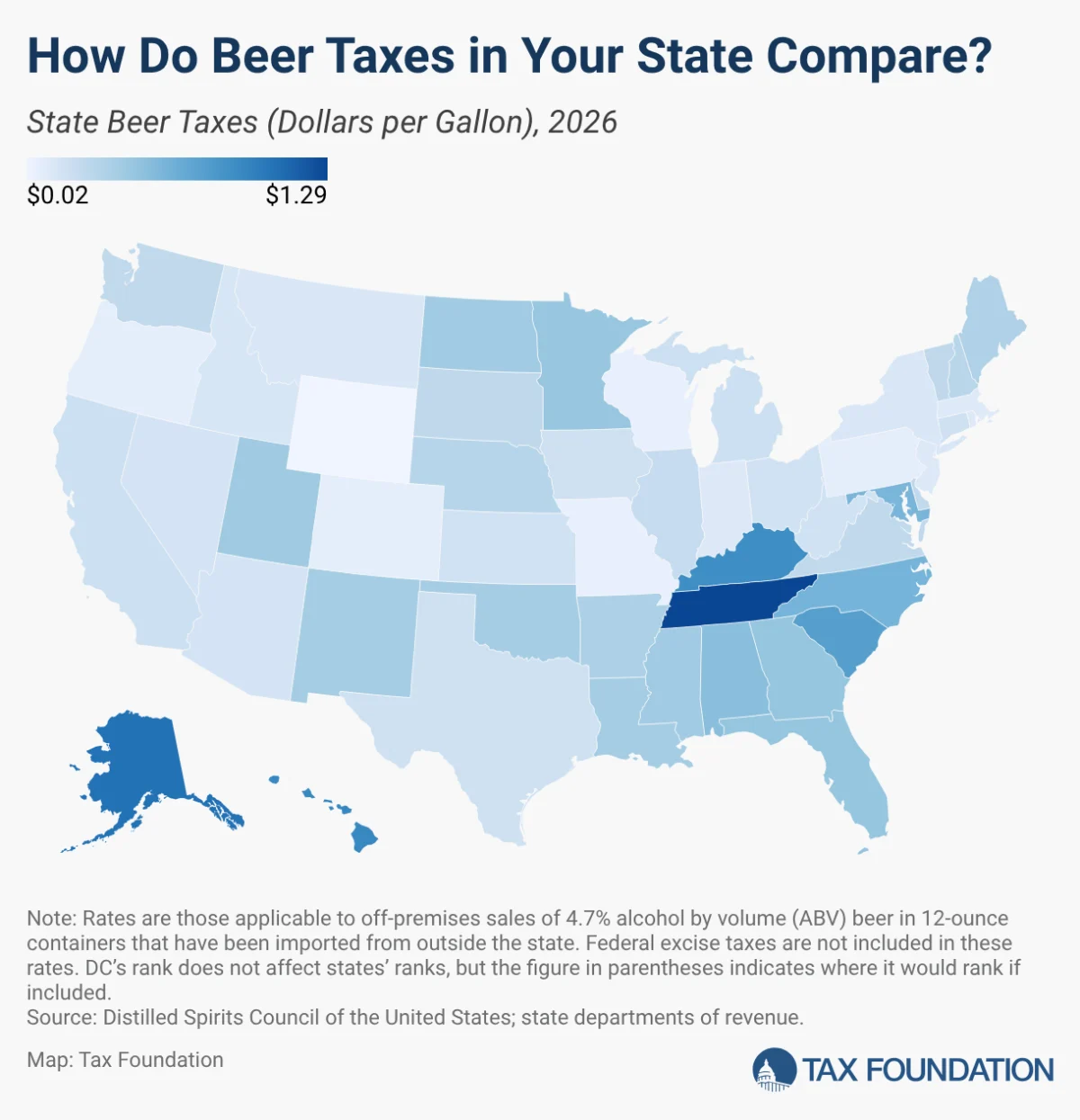

- 2023–2024: Several states, including Missouri, prioritized economic development by cutting taxes on locally manufactured beer. Missouri’s recent reduction to $0.02 per gallon stands in stark contrast to the high-tax environments of Tennessee or Alaska.

- 2025–2026 Outlook: As states face pressure to fill budget gaps, the beer tax remains a perennial target. The lack of uniformity means that a 12-ounce container of 4.7% ABV beer can cost significantly more in Nashville than it does in Cheyenne, purely due to the legislative environment.

Data Breakdown: The Cost of a Pint by Region

The disparity in state taxation is staggering. According to current data, the tax burden on beer fluctuates wildly across the U.S. map, creating an uneven playing field for both producers and consumers.

Highest Tax States (Per Gallon)

- Tennessee: $1.287

- Alaska: $1.07

- Hawaii: $0.93

Lowest Tax States (Per Gallon)

- Wyoming: $0.019

- Missouri: $0.06

- Wisconsin: $0.065

These figures represent only the state-level excise tax. In jurisdictions like Anchorage, Alaska, the local municipality adds an additional 5 percent sales tax specifically on alcohol. Meanwhile, Alabama and Georgia employ a "uniform local tax" that adds roughly 50 cents per gallon to the statewide burden, ensuring that the final cost of a brew in these states is significantly higher than the federal baseline.

Regulatory Anomalies and "Sin" Categories

Beyond simple per-gallon rates, states frequently manipulate taxes based on the characteristics of the product. This has created a regulatory environment that often penalizes innovation.

In Idaho, for instance, the law treats beer with more than 5% ABV differently, categorizing it alongside wine. This leads to a "tax cliff," where a slightly stronger beer is suddenly subject to a rate of $0.45 per gallon instead of the standard $0.15. Similarly, Virginia uses a tiered system based on container size—taxing beer differently depending on whether it is sold in a 7-ounce bottle, a 12-ounce bottle, or a larger container.

This categorical system is often criticized as "arcane." It fails to account for the fact that a light lager and a high-gravity IPA are both products of the same brewing process. By forcing beer into rigid statutory categories, states often create disincentives for brewers to experiment with new, higher-quality products.

Implications for the Future: A Shrinking Market

The brewing industry is currently facing a "perfect storm." Beyond the heavy tax burden, brewers are grappling with rising costs due to tariffs on imported aluminum and raw ingredients, as well as a significant shift in consumer behavior. Younger demographics, particularly Gen Z and Millennials, are increasingly moving toward low-alcohol or "sober-curious" lifestyles.

The Budgetary Risk

For state governments that rely on steady excise tax revenue, these shifts present a long-term fiscal risk.

- Currency Debasement: Because many excise taxes are ad quantum (fixed-rate, per-unit), their real value erodes over time due to inflation. Governments must constantly increase rates to keep up with purchasing power, which can lead to political backlash.

- Behavioral Volatility: As consumers shift to lower-alcohol or non-alcoholic options, the revenue from beer taxes becomes less predictable. Reliance on these funds for general budget spending could lead to unforeseen deficits.

The Case for Modernization

Industry experts and policy analysts at organizations like the Tax Foundation suggest that the current system is overdue for an overhaul. The recommendation is to shift toward a system based on actual alcohol content rather than arbitrary category definitions.

Modernizing the alcohol tax system would offer three primary benefits:

- Neutrality: It would treat all alcohol products equally based on their composition, rather than historical definitions that favor certain legacy products over new innovations.

- Simplicity: It would reduce the administrative burden on breweries that currently must navigate 50 different, highly complex state tax codes.

- Transparency: It would allow consumers to better understand the true cost of their purchases, fostering a more honest dialogue between the public and policymakers.

Conclusion: The Path Forward

As the U.S. beer industry navigates a changing landscape, the tax question remains central to its economic health. While excise taxes have long been viewed as a reliable "cash cow" for state and federal budgets, the industry’s recent stagnation suggests that this revenue source may be reaching its limit.

For the average consumer, the next time you toast to the summer, remember that the price of your beer is doing more than covering the costs of production—it is fueling a complex, often contradictory, and deeply fragmented system of taxation. Whether policymakers will choose to simplify this framework or continue to rely on the current, outdated model remains one of the most significant, yet overlooked, economic questions of our time. To preserve one of America’s most cherished social traditions, a transition toward a more neutral, alcohol-content-based tax system may be the only way to ensure the industry remains both profitable and accessible for the next generation of consumers.