For many, higher education is the traditional pathway to professional success and financial stability. Yet, the reality of the modern academic landscape is far more complex. According to data from the Education Data Initiative, 39% of first-time students pursuing a bachelor’s degree fail to complete their program within an eight-year window. Whether due to financial hardship, personal challenges, or a shift in career trajectory, millions of Americans find themselves carrying the burden of student debt without the benefit of a completed degree.

If you are part of this demographic, you may feel locked out of financial relief options. Many private lenders traditionally restrict refinancing opportunities to graduates, creating a cycle where non-graduates are stuck with higher interest rates and less favorable terms. However, the market is shifting. Refinancing remains a viable strategy for non-graduates, provided you understand the landscape, your eligibility, and the long-term trade-offs.

The Reality of Debt: Why Refinancing Matters

Even if you did not complete your degree, the legal obligation to repay your student loans remains unchanged. Managing this debt is critical to your long-term financial health. Refinancing—the process of replacing existing loans with a new, private loan—can be a powerful tool to lower interest rates, reduce monthly payments, and streamline your finances into a single, manageable bill.

While federal loan programs offer certain protections that private loans do not, private refinancing can potentially save borrowers thousands of dollars in interest over the life of a loan. For someone balancing the challenges of a career without a degree, this extra monthly cash flow can be the difference between financial stability and a debt spiral.

Top Lenders for Non-Graduates

While the pool of lenders willing to work with non-graduates is smaller, it is not empty. If you have a solid credit history and a reliable income, several reputable institutions offer pathways to refinance.

1. Earnest: Flexibility for Borrowers

Earnest is frequently cited as a top choice for those who left school before graduating. They require a minimum loan amount of $5,000. Key eligibility criteria include a strong credit history and at least six years since the borrower’s last enrollment. Furthermore, the original loans must have been used for an institution accredited by Title IV.

2. Citizens Bank: A Traditional Approach

Citizens Bank offers a pathway for non-graduates who have demonstrated a history of responsible repayment. Specifically, applicants must have completed at least 12 qualifying monthly payments after leaving their academic program. They offer loan terms ranging from five to 20 years, making it a flexible option for those seeking to lower monthly obligations.

3. Advantage Education Loan

This provider is specifically designed to be accessible to a broader range of borrowers. With a minimum loan amount of $7,500 and repayment terms between 10 and 20 years, it serves as a strong contender. Notably, for those who lack the required credit profile on their own, Advantage allows for the inclusion of a cosigner to improve the odds of approval.

4. EDvestinU

Focusing on loans used for Title IV, degree-granting institutions, EDvestinU provides refinancing for balances between $7,500 and $200,000. Their model is highly sensitive to the benefits of a cosigner, which can be the determining factor in securing a lower interest rate.

5. MEFA (Massachusetts Educational Financing Authority)

MEFA is a non-profit lender that offers refinancing without a degree requirement. They require a minimum balance of $10,000 and look for a consistent history of on-time payments. They are particularly popular for their fixed-rate options and terms ranging from seven to 15 years.

6. RISLA (Rhode Island Student Loan Authority)

Despite the name, RISLA’s services are available nationwide. They offer refinancing for balances from $7,500 to $250,000. Their application process is straightforward, and they are noted for being one of the more accessible lenders for non-graduates in the current market.

The Financial Implications: Is Refinancing Right for You?

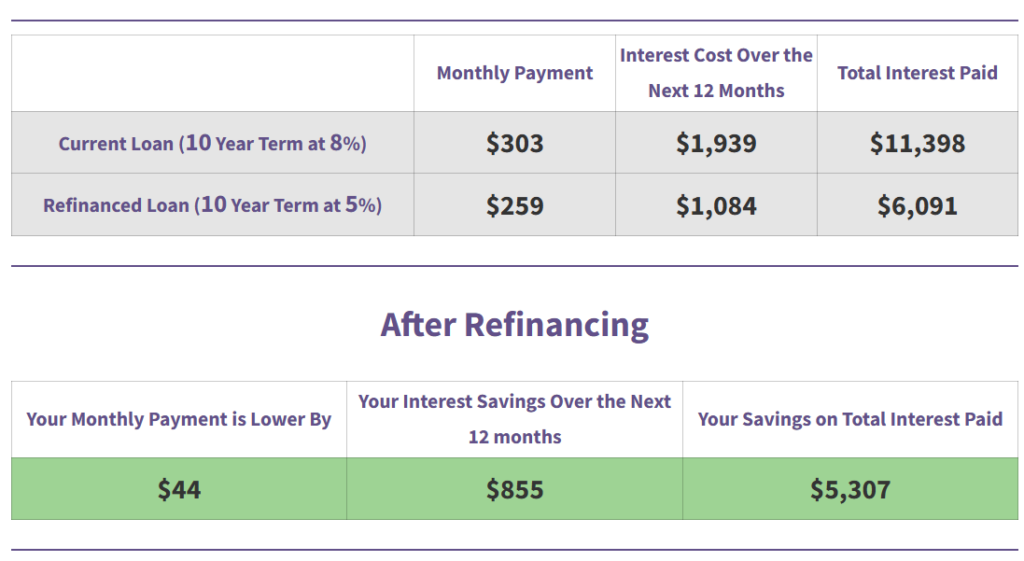

Before rushing to refinance, it is essential to weigh the math. Consider a scenario where you hold a $25,000 loan balance at an 8% interest rate. By successfully refinancing to a 4.5% rate, you could reduce your monthly payment from $303 to $259. Over the life of the loan, that equates to a saving of approximately $5,307 in interest.

The "Hidden" Cost: Losing Federal Protections

While the interest savings are compelling, they come with a major caveat. If you refinance federal student loans into a private loan, you permanently waive federal benefits. These include:

- Income-Driven Repayment (IDR) plans: These cap your monthly payments based on your income and family size.

- Public Service Loan Forgiveness (PSLF): This allows for the discharge of remaining debt after ten years of qualifying public service employment.

- Deferment and Forbearance: Federal loans offer built-in flexibility during periods of economic hardship or unemployment.

If you are a federal borrower, you must evaluate if the interest savings outweigh the loss of these safety nets. For many, the security of federal protections is worth the higher interest cost.

Requirements and Strengthening Your Profile

Qualifying for refinancing without a degree is not automatic. Lenders view these applications with higher scrutiny, focusing on:

- Credit Score: A score in the high 600s or 700s is often the baseline for competitive rates.

- Debt-to-Income (DTI) Ratio: Lenders want to ensure you have enough income to cover your debt obligations comfortably.

- Payment History: A clean track record of on-time payments is perhaps the most important metric for lenders evaluating non-graduates.

If your profile is not quite where it needs to be, do not despair. Many borrowers use a cosigner—a parent or spouse with strong credit—to gain access to these programs. Always inquire if the lender offers "cosigner release," which allows you to remove the cosigner from the loan once you have hit a certain number of on-time payments.

Alternative Paths: If Refinancing Isn’t an Option

If you do not meet the criteria for private refinancing, or if you decide that your federal protections are too valuable to lose, you still have options to manage your debt:

- Income-Driven Repayment (IDR): Programs like the Income-Based Repayment (IBR) or the Pay As You Earn (PAYE) plan remain the gold standard for federal borrowers struggling with high payments.

- Repayment Assistance Plans (RAP): These newer initiatives focus on adjusted gross income, providing more nuanced support for those with fluctuating earnings.

- Hardship Deferment: If you are facing a temporary crisis, federal lenders offer deferment or forbearance, allowing you to pause payments without penalty.

Moving Forward: A Strategic Approach

The process of managing student debt without a degree is a marathon, not a sprint. The first step is to conduct a thorough audit of your current loans. Understand the difference between your federal and private holdings. Use online calculators to model how different interest rates would impact your long-term wealth.

If you feel overwhelmed by the complexity of these choices, consider seeking professional help. A student loan consultant can provide a personalized roadmap, helping you decide whether to pursue forgiveness, consolidation, or refinancing.

In the modern economy, your value is not defined by a piece of paper, but by your financial literacy and your ability to manage your liabilities. By taking an active, informed role in your repayment strategy, you can turn a challenging situation into a manageable, successful financial future. Whether you decide to refinance today or wait until your credit and income profile are stronger, the path to debt management is open to you.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult with a licensed financial advisor before making decisions regarding your student loan portfolio.