For many, a college degree is viewed as the primary gateway to professional advancement and higher earning potential. However, the reality of modern education is often more complex. Life events—ranging from financial hardship and family emergencies to changing career interests—frequently interrupt the path to graduation. According to data from the Education Data Initiative, approximately 39% of first-time, bachelor’s degree-seeking students do not complete their programs within an eight-year window.

For these individuals, the burden of student loan debt remains, even without the credential to show for it. While the prevailing narrative suggests that refinancing is reserved for graduates, the landscape is shifting. It is entirely possible to refinance student loans without a degree, though the process requires a more nuanced approach and a stronger financial profile.

The Reality of Debt: Why Refinancing Matters

Regardless of whether you completed your degree, your obligation to repay your student loans remains unchanged. Many borrowers who leave school early find themselves struggling with high-interest rates, predatory loan terms, or monthly payments that do not align with their current income.

Refinancing acts as a financial tool to replace one or more existing loans with a single, new private loan, ideally carrying a lower interest rate or a more manageable monthly payment. For those who did not graduate, the goal is often to escape the crushing interest of original debt and gain breathing room in their monthly budgets. By securing a lower rate, borrowers can potentially save thousands of dollars over the life of their loans.

Chronology and Evolution of Lending Standards

Historically, the student loan industry maintained rigid requirements: a degree was the "gold standard" for creditworthiness. Lenders operated on the assumption that a degree correlated directly with future income stability. Consequently, non-graduates were largely excluded from the competitive private refinancing market.

In the last decade, however, the lending industry has evolved. As the workforce has become more skill-based rather than credential-based, several progressive lenders have begun to assess applicants based on their actual financial behavior—such as payment history, debt-to-income (DTI) ratios, and credit scores—rather than their academic status. This shift recognizes that a student who left school six years ago and has been working steadily is a significantly lower risk than a recent graduate with no employment history.

Leading Lenders for Non-Graduates

While the pool of lenders is smaller than that available to graduates, several reputable institutions now offer refinancing pathways for non-degree holders.

1. Earnest

Earnest has distinguished itself by focusing on the "whole applicant." They allow borrowers without a degree to refinance, provided they meet specific benchmarks. Applicants typically need to demonstrate at least six years since their last enrollment, and the loans must have been used for an institution accredited by Title IV.

2. Citizens Bank

Citizens Bank takes a performance-based approach. They require non-graduates to demonstrate stability by having made at least 12 consecutive, on-time monthly payments after leaving school. This serves as a proxy for financial responsibility, allowing the bank to bypass the traditional degree requirement.

3. Advantage Education Loan

For those seeking a more traditional structure, Advantage Education Loan provides options starting at $7,500. They are particularly flexible for borrowers who may have lower credit scores, as they allow for the inclusion of a cosigner to strengthen the application.

4. EDvestinU

EDvestinU serves as a strong candidate for larger balances, allowing for refinancing up to $200,000. Their requirement is straightforward: the original loans must have been utilized at a Title IV, degree-granting institution. Like others, they emphasize the benefit of a cosigner to secure the most favorable interest rates.

5. MEFA (Massachusetts Educational Financing Authority)

MEFA is a mission-driven lender that does not require a degree, provided the borrower has at least $10,000 in student debt. Their criteria focus heavily on a consistent history of on-time payments and U.S. residency, making them a reliable option for those who have spent several years in the workforce.

6. RISLA (Rhode Island Student Loan Authority)

Despite its name, RISLA provides nationwide service. They offer a broad range of loan amounts, from $7,500 to $250,000, with flexible terms between five and 15 years. Their transparent criteria make them a frequent choice for non-graduates looking for competitive, fixed-rate products.

Supporting Data: The Math of Refinancing

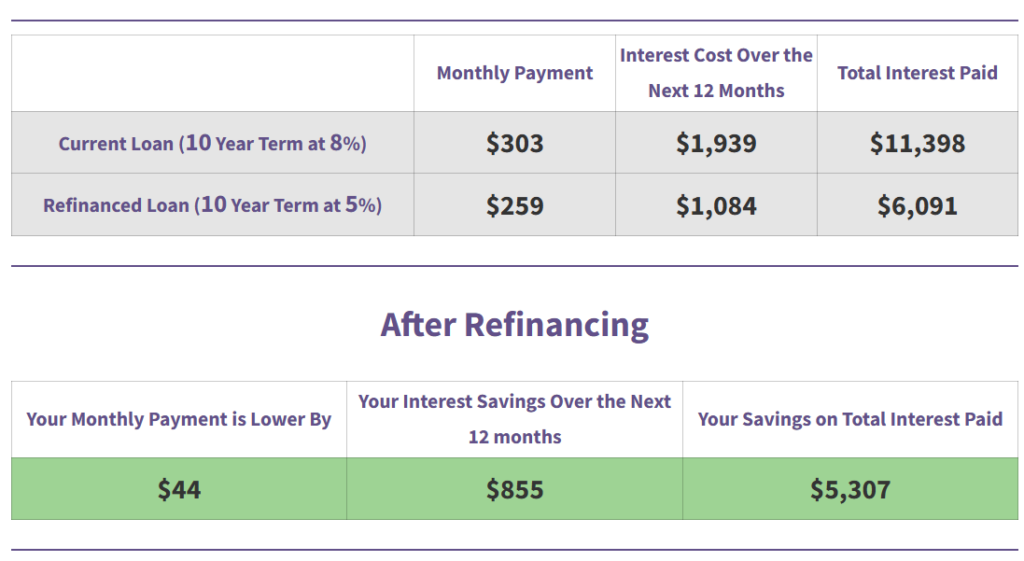

The economic justification for refinancing is best illustrated through a concrete example. Consider a borrower who holds $25,000 in student loan debt at an 8% interest rate.

- Current Monthly Payment: Approximately $303.

- Refinanced Rate (4.5%): Approximately $259.

- Monthly Savings: $44.

- Total Interest Saved: Over the life of a standard 10-year term, this move results in a savings of approximately $5,307.

These numbers highlight why even a small reduction in interest rates can have a compounding positive effect on personal wealth. Borrowers are encouraged to utilize online refinancing calculators to project these savings based on their specific loan balances and current market rates.

Implications of Refinancing: The "Hidden" Costs

While the financial upside is clear, it is critical to weigh the risks. Refinancing federal student loans into a private loan means forfeiting federal protections. This is a permanent decision.

Loss of Federal Benefits include:

- Income-Driven Repayment (IDR) Plans: Federal loans offer plans that cap payments based on income; private loans do not.

- Public Service Loan Forgiveness (PSLF): If you work for a government or non-profit entity, you lose the ability to have your balance forgiven after 120 qualifying payments.

- Deferment and Forbearance: Federal loans offer robust, legislated protections during times of economic hardship, which are far more flexible than those offered by private lenders.

Before proceeding, every borrower must conduct a "gap analysis" to determine if their need for a lower interest rate outweighs their potential need for federal safety nets.

Official Guidance and Eligibility Requirements

Most lenders evaluating non-graduate applications look for a "strong financial profile." To maximize your chances of approval, lenders generally scrutinize:

- Credit Score: A history of responsible credit management.

- Debt-to-Income Ratio (DTI): Ensuring that your total monthly debt payments are low relative to your gross monthly income.

- Employment History: Consistent income verification.

- Payment History: A clear record of on-time payments on existing student loans is often a mandatory threshold.

If your profile falls short, the most effective strategy is the inclusion of a creditworthy cosigner. A cosigner acts as a guarantor, providing the lender with added security. It is highly recommended to seek a lender that offers a "cosigner release" policy, which allows the cosigner to be removed from the loan agreement once you have demonstrated independent repayment reliability for a set number of years.

Strategic Alternatives: What If Refinancing Isn’t Possible?

If you do not meet the criteria for private refinancing, or if you decide that retaining federal protections is too important, there are still avenues for relief:

- Income-Driven Repayment (IDR): For federal borrowers, plans like IBR or the new Repayment Assistance Plan (RAP) can lower monthly payments to a percentage of your discretionary income.

- Hardship Deferment: Many federal loans allow for temporary pauses in payment due to unemployment or economic hardship.

- Professional Consultation: For complex debt situations, booking a professional student loan consultation can provide a personalized roadmap, ensuring that you are not missing out on forgiveness programs or state-specific assistance.

Conclusion: A Path Forward

Refinancing without a degree is not an admission of failure, but a strategic financial maneuver. By moving from high-interest debt to a more manageable structure, you can reclaim control over your financial future. Whether you decide to refinance today, focus on building your credit for a future application, or leverage federal programs, the most important step is to act with a clear understanding of your long-term goals.

As the economy continues to shift, the definition of "success" in higher education is becoming broader. Your student loans should not be a permanent anchor. By auditing your current debt, comparing lender requirements, and carefully weighing the loss of federal protections, you can find a strategy that allows you to move forward with confidence.

For those unsure of their next steps, utilizing online diagnostic tools—such as 11-question financial quizzes or specialized calculators—can provide the clarity needed to determine whether your specific portfolio is best suited for PSLF, IDR, or the private refinancing market.