By Financial News Desk

The traditional narrative of the American Dream—the idea that hard work and "grit" alone lead to financial independence—is undergoing a profound transformation. According to a comprehensive new survey released by Lexington Law, the path to building wealth in the United States is increasingly bifurcated, defined less by individual effort and more by generational timing and family resources.

The study, which surveyed 1,000 American adults across all major demographics, highlights a growing "wealth-building gap." While younger generations express a surprising level of optimism, they are doing so against a backdrop of record-breaking housing prices, stagnant wages, and a system many believe is "rigged" against them. Perhaps most strikingly, the data reveals that the "self-made" success story of high earners is often bolstered by significant, yet frequently unacknowledged, parental financial assistance.

Main Facts: The New Reality of American Wealth

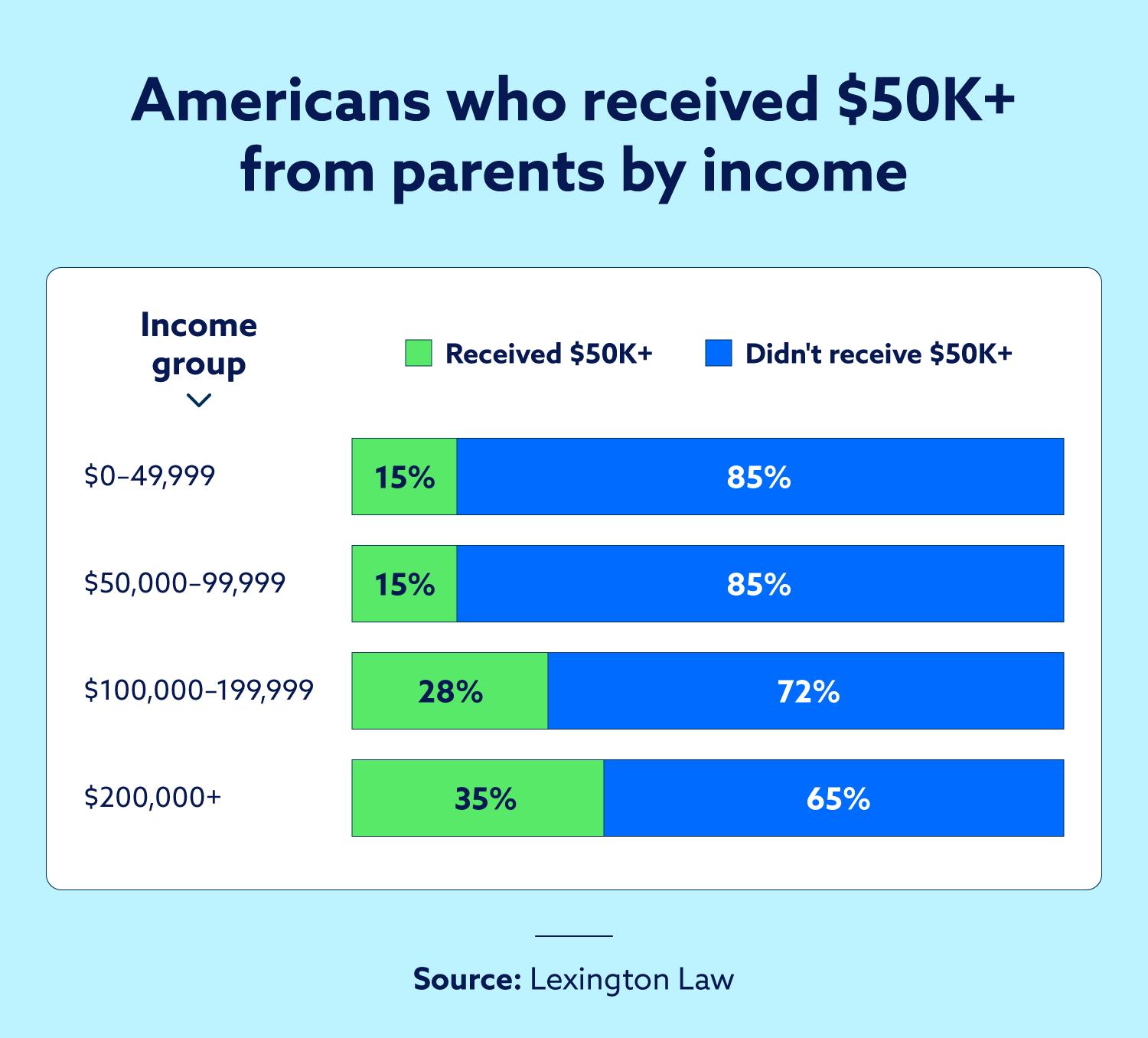

The Lexington Law survey offers a sobering look at the mechanics of modern prosperity. The most prominent finding challenges the cultural trope of the self-made millionaire: individuals earning $125,000 or more annually are 2.5 times more likely to have received a financial "head start" of $50,000 or more from their parents compared to lower-income earners.

Key findings from the report include:

- The Inheritance Advantage: 36 percent of high earners received at least $50,000 in parental support, while 53 percent of the general population received $10,000 or less, if anything at all.

- The Generational Paradox: Despite acknowledging that the economic system is rigged in favor of older generations (72 percent), an overwhelming 87 percent of Gen Z respondents believe they will be more successful than their parents.

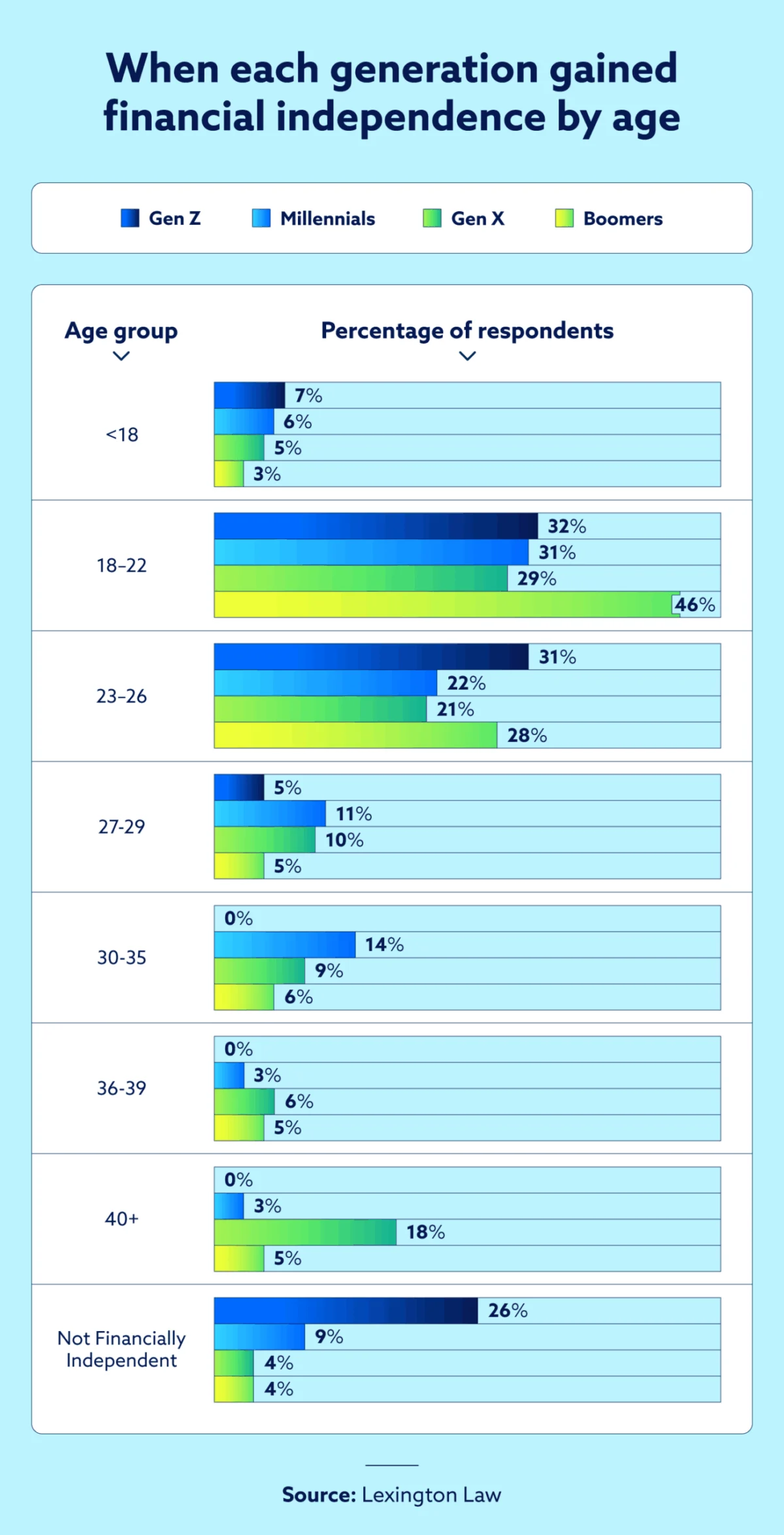

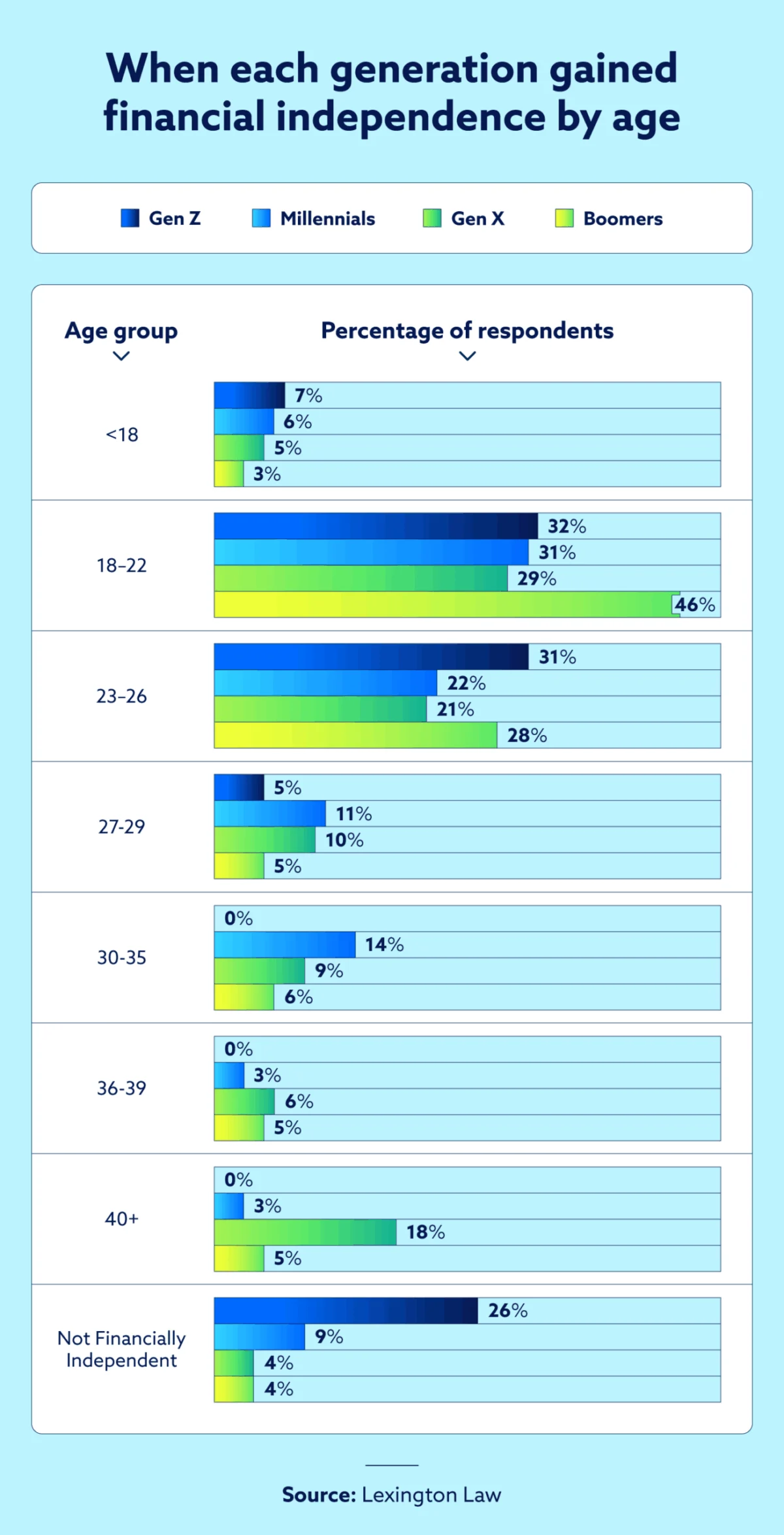

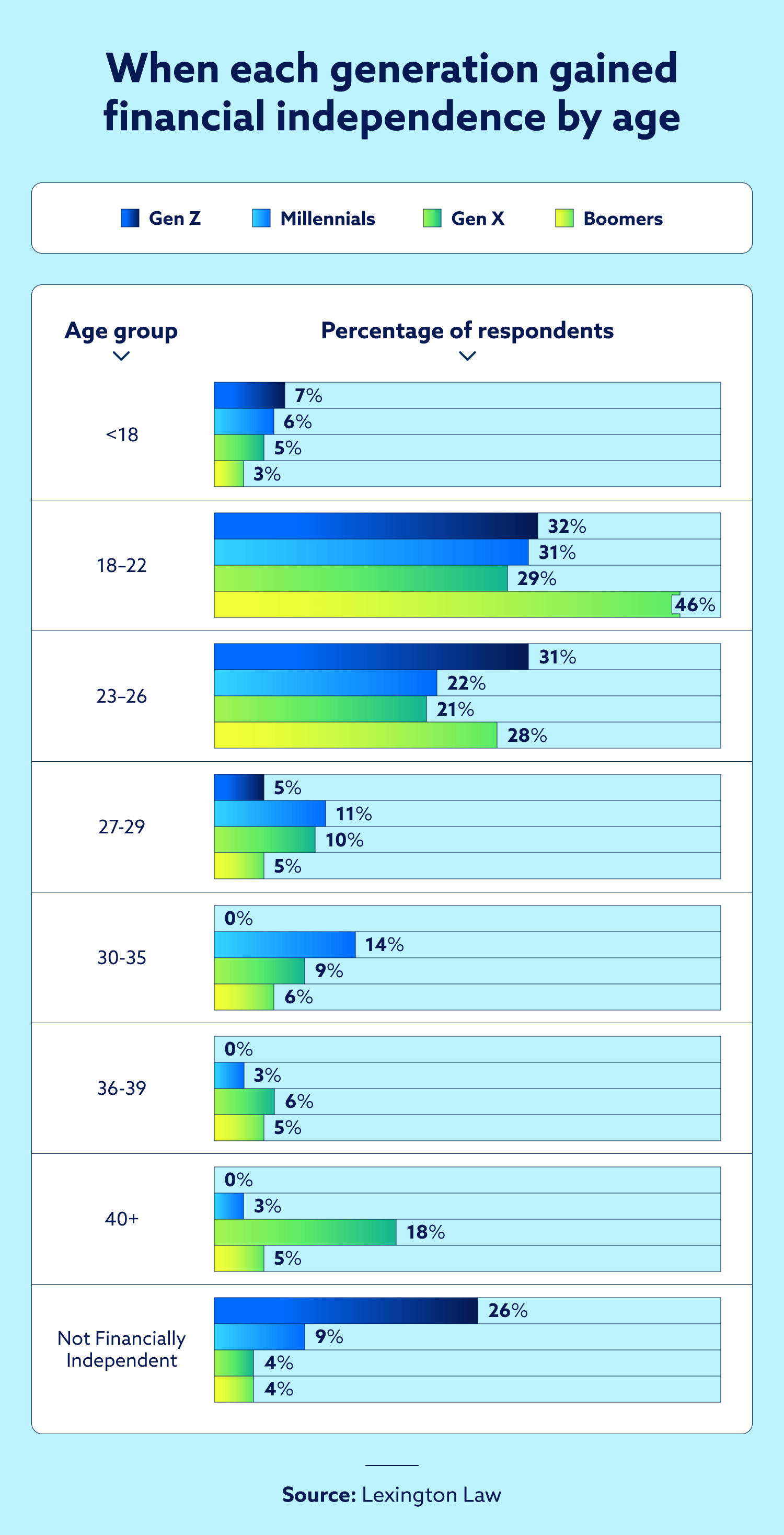

- The Independence Delay: Financial autonomy is arriving later with each passing decade. While nearly half of Baby Boomers were independent by age 22, Gen Z and Millennials are increasingly reliant on the "Bank of Mom and Dad" well into their late 20s and 30s.

- The Gen X Crisis: Generation X represents the highest earners (54 percent make over $100,000) but also the most pessimistic, with nearly half reporting a bleak outlook on their financial future.

- The Cost-of-Living Barrier: 73 percent of all respondents cited the rising cost of living as the primary obstacle to wealth accumulation, followed closely by housing costs at 65 percent.

Chronology: From Post-War Prosperity to the Modern Squeeze

To understand the current generation gap, one must look at the economic trajectory of the last several decades. The survey participants’ views are deeply colored by the era in which they entered the workforce.

The Boomer Benchmark (1946–1964)

Baby Boomers entered a post-World War II economy characterized by rapid industrial growth and relatively low costs of education and housing. The survey confirms that 48 percent of Boomers reached financial independence by age 22. This early start allowed for decades of compounding interest in the stock market and the accumulation of home equity during periods of significant appreciation.

The Gen X Transition (1965–1980)

Gen X navigated the transition into the digital age and the shift from pensions to 401(k)s. While they currently sit in their peak earning years, they were also the generation most likely to be hit by the 2008 financial crisis mid-career. The survey suggests they are now the "sandwich generation," receiving parental support (23 percent received over $50,000) while simultaneously supporting their own adult children.

The Millennial and Gen Z Struggle (1981–Present)

The last four years have seen a particularly sharp shift. According to the U.S. Bureau of Labor Statistics, the cost of living has surged by more than 20 percent since 2021. For younger workers, this inflation has coincided with a record-breaking housing market that has made the traditional first step of wealth building—homeownership—increasingly unattainable. Consequently, financial independence for these groups is often delayed until age 30 or later.

Supporting Data: Analyzing the Barriers to Success

The survey provides a granular look at the specific economic pressures preventing Americans from saving. While the "rising cost of living" is a catch-all term, the data breaks down the obstacles by generational priority.

The High Cost of Existing

For 73 percent of Americans, the daily expenses of gas, groceries, and utilities are the primary "wealth killers." This is no longer a concern exclusive to the working class; even those in the middle and upper-middle-income brackets report that discretionary income is being swallowed by basic necessities.

The Housing Hurdle

Housing costs were cited by 65 percent of respondents as a major barrier. With the Federal Reserve’s interest rate hikes aimed at curbing inflation, mortgage rates have remained high, creating a "lock-in" effect for current homeowners and a "lock-out" effect for first-time buyers.

The Wage-Growth Gap

Nearly half of the respondents (49 percent) identified stagnant wages as a core issue. While nominal wages have risen, they have largely failed to keep pace with the real-world inflation of "big ticket" items like healthcare and education.

Healthcare Concerns

The data shows a specific generational pain point for Baby Boomers: 62 percent cited healthcare costs as their biggest financial challenge. This highlights that even for the generation that had the best wealth-building opportunities, the rising cost of elder care threatens to deplete the assets they spent a lifetime accumulating.

Official Responses and Expert Perspectives

While the Lexington Law survey provides the raw data, federal agencies and economic experts have echoed these sentiments in recent reports.

The U.S. Department of the Treasury has noted that the "well-being of young adults" is now more closely tied to family resources than in previous generations. In a recent analysis, the Treasury highlighted that the transition to adulthood is taking longer, with significant implications for long-term wealth inequality.

The U.S. Federal Reserve has pointed to the 2008 recession as a "scarring event" that fundamentally altered the financial trajectory of Millennials. The Fed’s data on the "Economic Well-Being of U.S. Households" aligns with the Lexington Law survey, showing that rising housing costs and student loan debt are the primary drivers of delayed independence.

Lexington Law’s Editorial Disclosure emphasizes that while the "system" may present obstacles, individual agency still plays a role—specifically through credit health. "Building wealth isn’t just about what you can earn," the report notes. "It’s about factors you can control, like building credit, which becomes increasingly important for reaching financial goals." Experts argue that a clean credit report is the "utility" of the financial world, allowing individuals to access lower interest rates that can save them hundreds of thousands of dollars over a lifetime.

Implications: The Future of the American Middle Class

The findings of this survey have profound implications for the future of the American economy and social mobility.

1. The End of the "Self-Made" Meritocracy?

If high earners are 2.5 times more likely to have received substantial parental help, the concept of meritocracy in the U.S. comes into question. This suggests that wealth is becoming "hereditary" in a way that hasn’t been seen in decades. Those without family safety nets are forced to take on more debt, further delaying their ability to invest and grow wealth.

2. The Gen Z Optimism Gap

The fact that 87 percent of Gen Z believe they will be successful, despite 72 percent believing the system is rigged, suggests a new type of "defiant optimism." This generation may be looking toward non-traditional wealth-building avenues—such as the gig economy, digital assets, or entrepreneurship—rather than the corporate-ladder-and-home-equity model used by their parents.

3. The Delayed Economy

As financial independence is pushed into the 30s and 40s, the broader economy may see a "delay effect." This includes delayed home purchases, delayed marriage and family formation, and a potential crisis in retirement savings. If workers do not begin saving until their late 30s, they lose a decade of compound interest that is nearly impossible to recover.

4. The Critical Role of Financial Literacy and Credit

In an economy where the "margin for error" is shrinking, financial literacy becomes a survival skill. The survey suggests that for those who do not have a $50,000 parental "cushion," maintaining a high credit score is the only way to level the playing field. Credit serves as the primary tool for social mobility, enabling those without inherited capital to borrow at rates that make wealth-building possible.

Conclusion

The Lexington Law survey serves as a wake-up call for policymakers and individuals alike. The "generation gap" in wealth building is not merely a matter of different spending habits or "avocado toast" clichés; it is a structural reality driven by inflation, housing shortages, and a fundamental shift in how financial independence is achieved.

As the path to prosperity becomes increasingly reliant on family resources, the challenge for the next decade will be finding ways to reopen the doors of opportunity for those who are starting from scratch. Whether through policy reform or individual financial empowerment, the goal remains the same: ensuring that the American Dream is a reality for all generations, not just those who were born at the right time or into the right family.

Methodology Note:

The survey was conducted by SurveyMonkey Audience for Lexington Law Firm between June 20, 2025, and June 22, 2025. It included 1,000 U.S. residents over the age of 18. The margin of error is +/- 2 percent with a 95 percent confidence level.