Introduction: The New Landscape of American Prosperity

Building wealth in the United States has historically been viewed through the lens of individual meritocracy—the "pull yourself up by your bootstraps" ethos. However, a comprehensive new study involving 1,000 American adults reveals a starkly different reality. The path to financial freedom is increasingly dictated not just by career choice or work ethic, but by generational timing and the "Bank of Mom and Dad."

As the cost of living surges—up more than 20 percent over the last four years according to the U.S. Bureau of Labor Statistics—the traditional milestones of adulthood are shifting. From record-breaking housing prices to the persistent weight of student debt, the financial journey for younger generations has become a marathon with a moving finish line. This report explores the findings of a recent Lexington Law survey, detailing how the transfer of generational wealth, shifting independence timelines, and systemic economic pressures are creating a fractured financial landscape for Gen Z, Millennials, Gen X, and Baby Boomers alike.

Main Facts: The Myth of the Self-Made High Earner

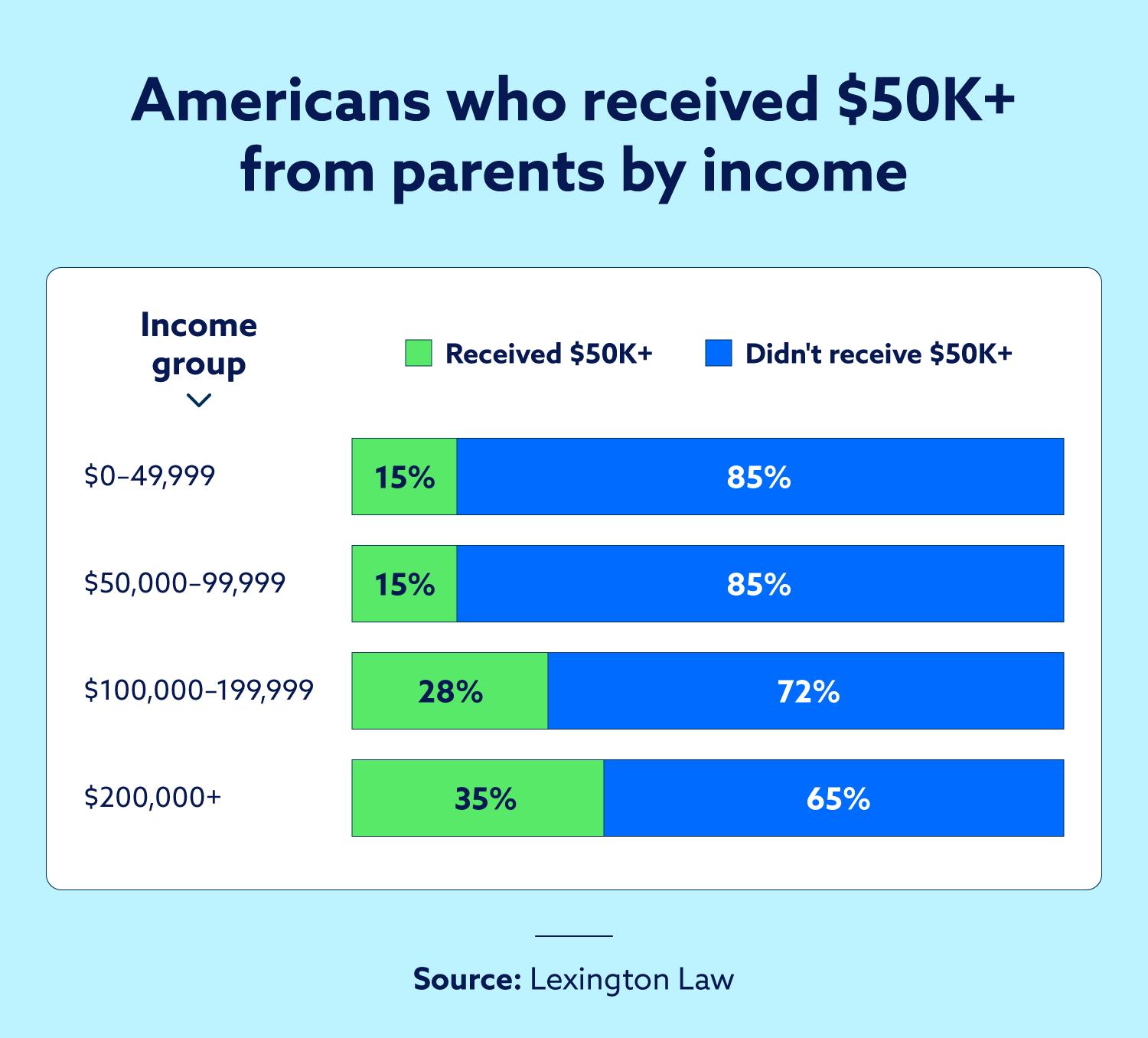

The most striking revelation from the survey data challenges the narrative of the "self-made" wealthy individual. The study found a direct correlation between high annual earnings and significant parental financial assistance. Individuals earning $125,000 or more per year are 2.5 times more likely to have received a substantial financial "injection" of at least $50,000 from their parents compared to lower-income earners.

Specifically, 36 percent of high earners reported receiving this level of support, whereas only 14 percent of those in lower income brackets could say the same. This suggests that early-career capital—often used for home down payments, debt elimination, or seed money for businesses—acts as a massive accelerant for long-term wealth accumulation.

While Gen X reported the highest levels of parental support overall—with nearly one in four receiving over $50,000—the majority of the American population remains outside this safety net. Over half of all respondents (53 percent) received $10,000 or less from their families, highlighting a growing divide between those with "inherited stability" and those forced to navigate a high-inflation economy in isolation.

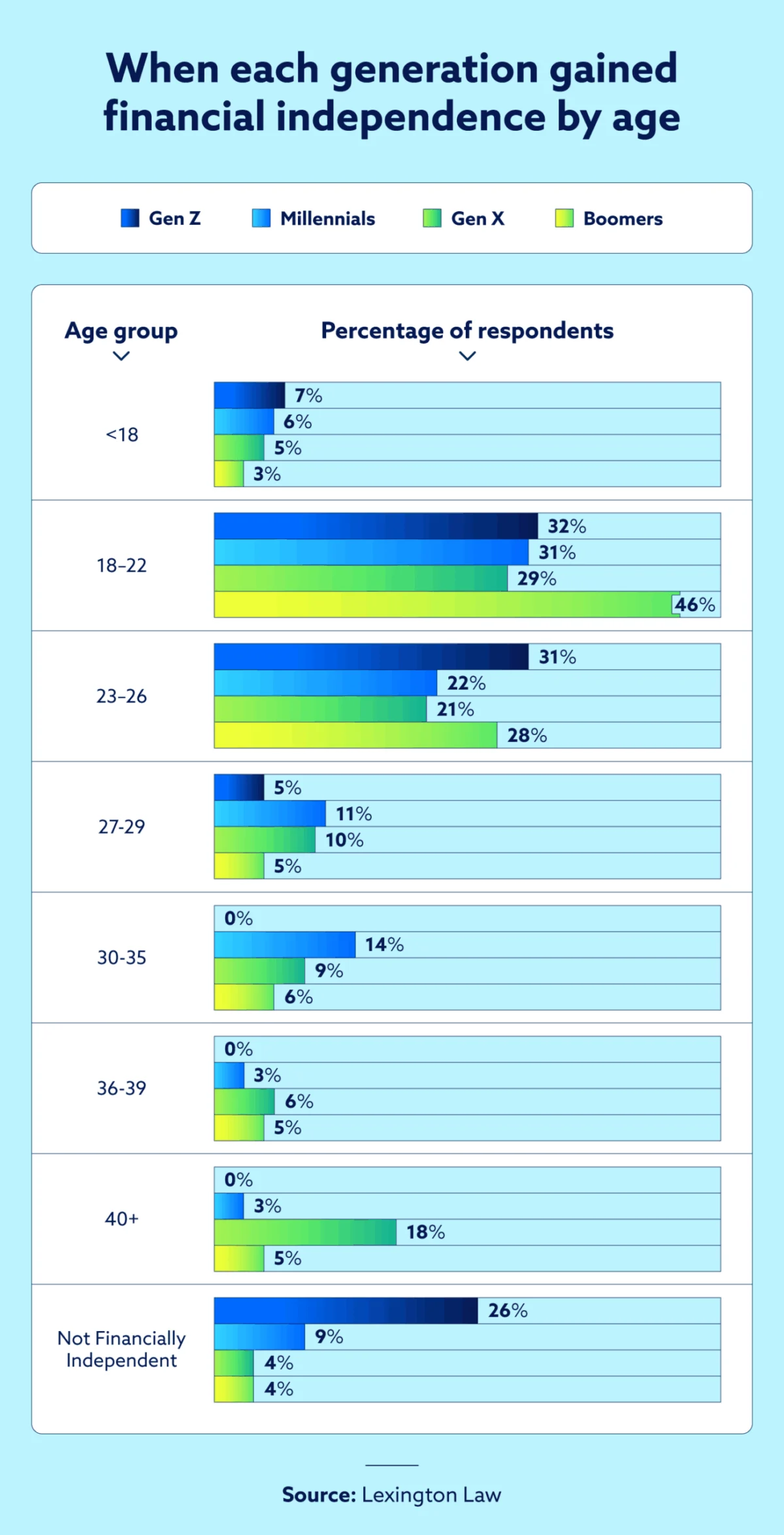

Chronology: The Shifting Timeline of Financial Independence

The data illustrates a clear chronological drift in when Americans achieve financial autonomy. The age at which a person "stands on their own two feet" has moved steadily upward over the last four decades.

- The Baby Boomer Era (Post-War to 1980s): For the Boomer generation, financial independence was achieved early. Nearly half (48 percent) reported being financially independent by the age of 22. This era was characterized by a lower cost of living relative to wages and a more accessible housing market.

- The Gen X Transition (1990s to early 2000s): While many Gen Xers achieved early success, the timeline began to stretch. Interestingly, 36 percent of Gen Xers surveyed did not reach full independence until after age 30, a precursor to the "delayed adulthood" seen in later cohorts.

- The Millennial and Gen Z Reality (2010s to Present): The shift is most pronounced among the youngest workers. Only 36 percent of Gen Z reached independence between the ages of 23 and 29. Furthermore, 26 percent of Gen Zers remain financially reliant on their parents well into their late 20s.

Perhaps most surprising is that high income does not necessarily equate to early independence in the modern economy. The survey found that 26 percent of individuals earning between $125,000 and $150,000 did not become independent until age 40 or older. This suggests that even high-paying professional roles are often insufficient to offset the high entry costs of modern American life without extended familial support.

Supporting Data: Optimism vs. A "Rigged" System

The survey uncovered a fascinating psychological paradox within Gen Z. Despite facing the most significant economic headwinds in recent memory, they remain the most optimistic generation regarding their personal futures.

- Gen Z Optimism: An overwhelming 87 percent of Gen Z respondents believe they will be as successful as, or more successful than, their parents. This confidence persists despite the fact that 72 percent of these same respondents believe the current economic system is "rigged" in favor of older generations.

- The Income-Outlook Gap: Interestingly, mindset does not always track with bank balances. Those earning under $25,000 annually reported a more positive financial outlook (49 percent optimistic) than those earning $125,000 or more (only 31 percent optimistic).

- The Gen X Pessimism: Despite being the highest-earning cohort—with 54 percent reporting incomes over $100,000—Gen X is the most pessimistic generation. Nearly half (49 percent) hold a bleak view of their financial future. This is likely due to the "Sandwich Generation" effect, where Gen Xers find themselves simultaneously supporting adult children and aging parents while trying to fund their own looming retirements.

Official Responses: Contextualizing the Economic Roadblocks

To understand why these generational gaps exist, one must look at the broader economic indicators cited by federal agencies. The survey results align closely with data from the U.S. Federal Reserve and the Department of the Treasury.

The U.S. Bureau of Labor Statistics notes that the Consumer Price Index (CPI) has surged, making basic necessities like groceries and energy a larger percentage of household budgets. According to the U.S. Federal Reserve’s reports on the economic well-being of households, the long-term effects of the 2008 recession, coupled with the post-pandemic inflationary spike, have created a "permanent plateau" of high costs.

The Treasury Department has also noted that the rising cost of higher education has fundamentally altered the wealth-building trajectory of young adults. With student loan debt hovering at record levels, the "starting line" for Millennials and Gen Z is effectively behind zero, whereas many Boomers started their careers with little to no debt and immediate access to equity-building assets like real estate.

Implications: The Structural Obstacles to Wealth Building

When asked to identify the primary barrier to wealth, the responses across all generations were remarkably unified. It is not "frivolous spending" that is hindering the American public, but systemic price increases.

- Cost of Living (73%): The top concern across the board. The erosion of purchasing power means that even those with raises feel they are "treading water."

- Housing Costs (65%): For younger generations, the dream of homeownership is increasingly viewed as a luxury. The survey suggests that without parental help for a down payment, many are locked into a permanent "renter class," unable to build the home equity that served as the primary wealth vehicle for their parents.

- Stagnant Wages (49%): Despite low unemployment numbers, nearly half of Americans feel their compensation has not kept pace with the 20 percent increase in living costs seen since 2021.

- Healthcare Costs (62% for Boomers): For the oldest generation, wealth is being drained not by lifestyle, but by the escalating costs of medical care, highlighting a different kind of financial vulnerability.

The Role of Credit in the New Economy

As systemic hurdles make traditional wealth-building more difficult, the importance of leverage—specifically credit—has intensified. In an environment where liquid cash is often tied up in high rent and daily expenses, a clean credit report becomes the only viable tool for accessing lower interest rates and financing opportunities that can lead to asset ownership.

For the 26 percent of young adults still relying on family support, the transition to independence will likely depend on their ability to establish a robust credit profile. As the survey suggests, if you cannot inherit a head start, you must optimize every financial tool at your disposal to bridge the gap.

Conclusion: A Call for Realistic Financial Planning

The Lexington Law survey paints a picture of an America at a financial crossroads. The "Great Generational Wealth Delusion" is being replaced by a sober realization: the economic math that worked for the Boomers no longer applies to Gen Z.

While parental support remains a significant predictor of high-income success, the majority of Americans must find a way to navigate an expensive economy through disciplined budgeting, strategic credit management, and a realistic understanding of the delayed timeline for independence. As we move further into the 2020s, the definition of the "American Dream" may need to shift from a sprint toward early retirement to a long-term strategy of survival and incremental growth in a high-cost world.

Methodology Note:

This study was conducted by SurveyMonkey Audience for Lexington Law Firm between June 20 and June 22, 2025. It includes responses from 1,000 U.S. residents aged 18 and older. The margin of error is +/- 2 percent at a 95 percent confidence level.