In an increasingly digitized global economy, a consumer’s credit score has evolved beyond a mere number; it is now a fundamental pillar of financial identity. As we navigate the fiscal environment of 2026, the traditional benchmarks of creditworthiness—the FICO® and VantageScore® systems—remain the industry standards, ranging from 300 to 850. However, the methodology for achieving these scores has become more sophisticated, integrating alternative data and real-time reporting.

A high credit score is the primary key to unlocking lower interest rates, favorable insurance premiums, and premium borrowing options. For those starting with a "thin file" or those seeking to rehabilitate a damaged reputation, the path to improvement requires a blend of disciplined traditional habits and the utilization of modern financial technology.

Main Facts: 15 Core Strategies for Rapid Credit Enhancement

Building credit in 2026 is no longer a passive process. It requires an active, multi-pronged approach. Financial experts identify 15 primary strategies that offer the most significant impact on a consumer’s profile.

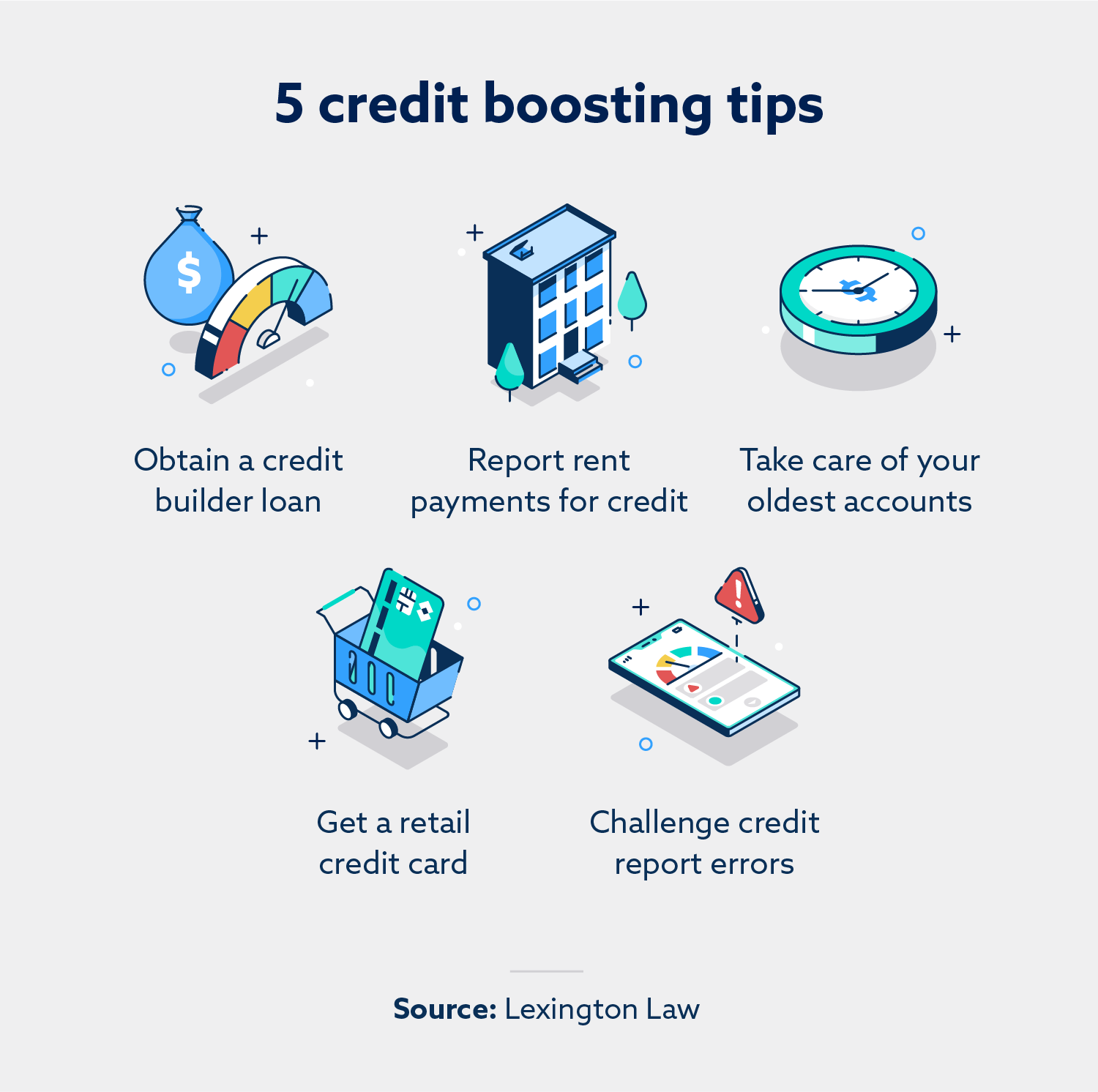

1. Credit Builder Loans

Unlike traditional loans where you receive funds upfront, credit builder loans act as a "reverse" installment plan. The lender holds the loan amount in a secured account while the borrower makes monthly payments. These payments are reported to the three major bureaus (Equifax, Experian, and TransUnion), establishing a record of reliability. Once the term is complete, the borrower receives the accumulated funds.

2. Rent Reporting Integration

Historically, rent—often a consumer’s largest monthly expense—was ignored by credit bureaus. In 2026, rent-reporting services have become mainstream. By opting into these services, tenants can have their history of on-time housing payments factored into their scores, which is particularly beneficial for those without an extensive history of debt.

3. Preservation of Account Age

Length of credit history accounts for approximately 15% of a FICO® score. Closing an old, unused credit card can inadvertently shorten the average age of accounts and reduce the total available credit, leading to a score drop. Financial advisors recommend keeping the oldest accounts open, even if they are rarely used, to demonstrate long-term stability.

4. Strategic Retail Credit Use

Retail credit cards often have lower barriers to entry than major bank cards. While they frequently carry higher interest rates, they serve as an effective tool for building credit if used for small, planned purchases that are paid in full immediately.

5. Systematic Error Challenging

The Consumer Financial Protection Bureau (CFPB) continues to report that a significant percentage of credit reports contain inaccuracies. These range from misreported late payments to accounts resulting from identity theft. Utilizing professional services or self-filing disputes to remove these errors is one of the fastest ways to see a score increase.

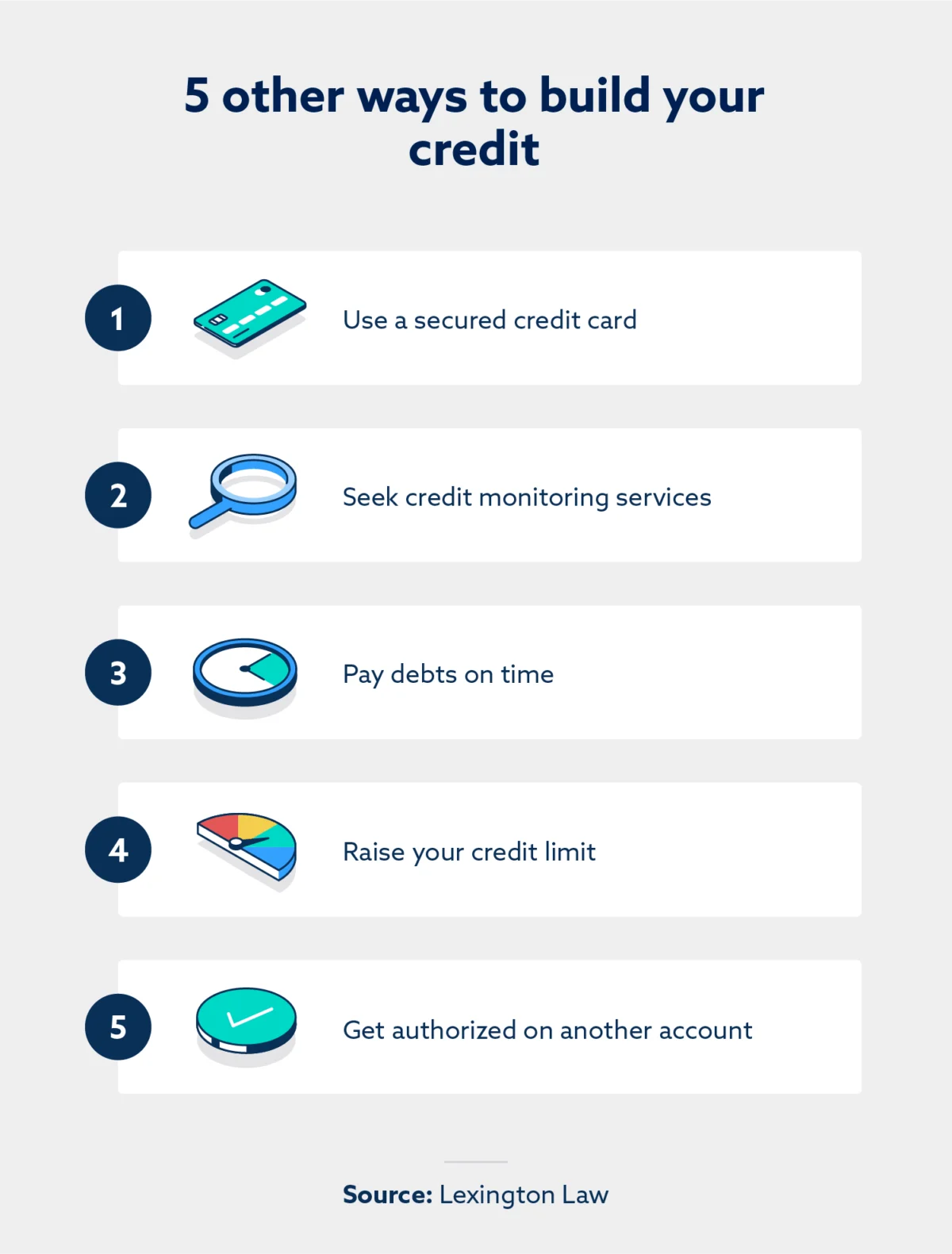

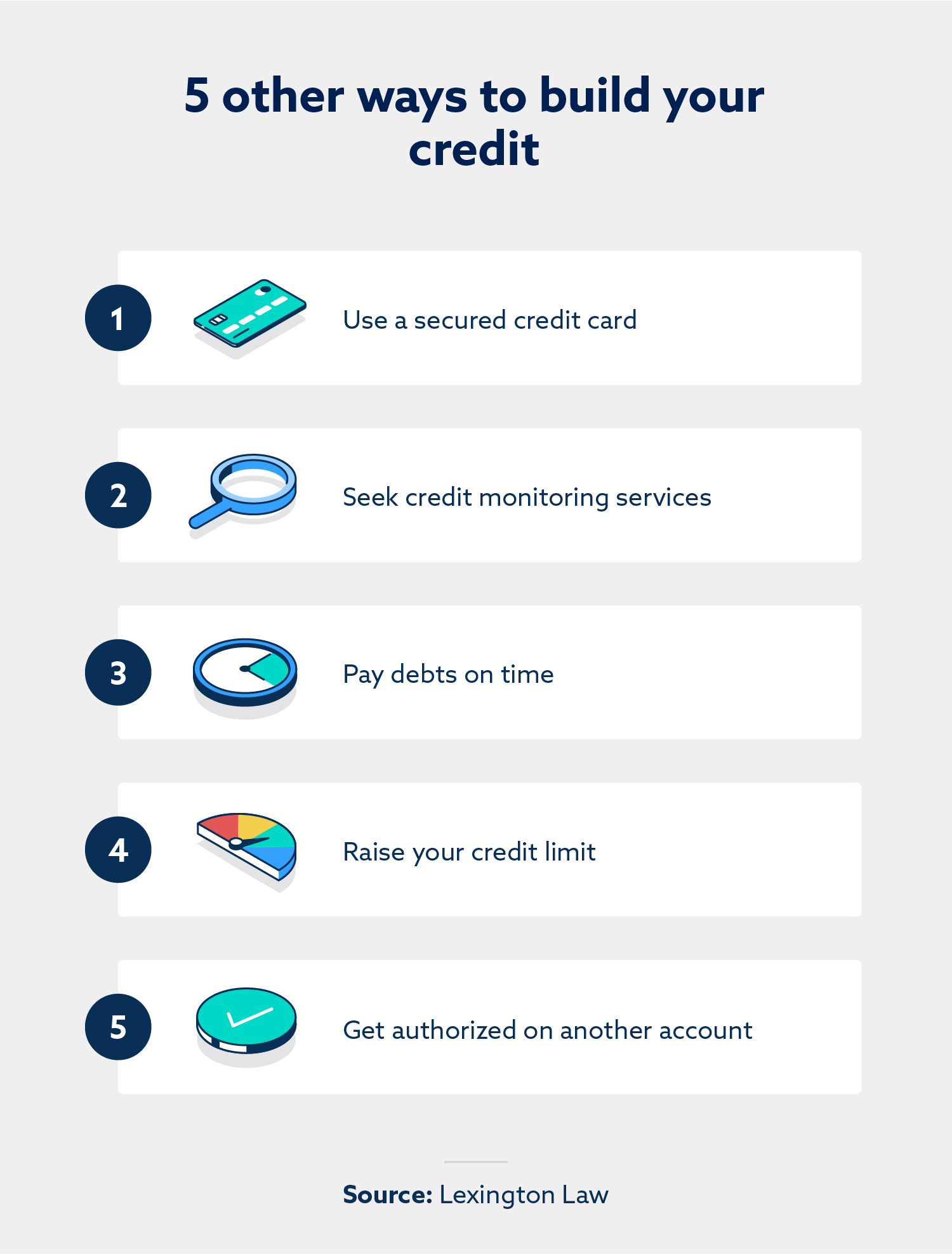

6. Secured Credit Card Utilization

For individuals with poor or no credit, secured cards remain a cornerstone. By providing a cash deposit as collateral, the borrower mitigates the lender’s risk. Responsible use of these cards typically leads to an "upgrade" to an unsecured card within 6 to 12 months.

7. Continuous Credit Monitoring

Active monitoring is the first line of defense against identity theft and reporting errors. Modern services provide real-time alerts for new inquiries or balance changes, allowing consumers to react instantly to fluctuations.

8. The Primacy of Timely Payments

Payment history remains the most critical factor, influencing 35% of FICO® scores and 40% of VantageScores. In the 2026 market, even a single 30-day delinquency can cause a score to plummet by up to 100 points for high-scorers.

9. Credit Limit Expansion

Increasing a credit limit without increasing spending is a highly effective way to lower the "credit utilization ratio." Keeping this ratio below 30%—and ideally below 10%—is a hallmark of "prime" borrowers.

10. Authorized User Status (Credit Piggybacking)

By being added as an authorized user to a well-maintained account of a family member or partner, a consumer can "inherit" that account’s positive history. However, this is a double-edged sword; if the primary cardholder misses a payment, the authorized user’s score may also suffer.

11. Student-Specific Credit Products

Designed for those in higher education, student cards offer a pathway to prove creditworthiness with less stringent income requirements, provided the applicant has proof of enrollment.

12. Rapid Rescoring for Mortgages

When applying for a home loan, hours matter. Rapid rescoring is a service provided by mortgage lenders that can update a credit report in 3 to 5 business days rather than the standard 30 to 45 days, capturing recent debt payoffs or error corrections just in time for a loan lock.

13. Professional Financial Advisory

In the complex 2026 economy, personalized advice from certified financial planners can help consumers navigate the nuances of debt-to-income ratios and strategic debt "avalanches" or "snowballs."

14. AI-Driven Credit Building Apps

A new generation of apps analyzes spending patterns and offers micro-loans or "virtual" lines of credit that report to bureaus, helping users build credit through their existing daily transactions.

15. Specialized Credit Builder Cards

Different from secured cards, these cards often link to a user’s bank account and limit spending to the available balance, effectively functioning like a debit card while reporting to credit bureaus as a revolving line of credit.

Chronology: The Lifecycle of Credit Reporting

Understanding the timeline of credit reporting is essential for managing expectations. Credit building is a marathon, not a sprint, though certain milestones can be reached quickly.

- Days 1–5: Initial actions such as requesting a credit limit increase or applying for a secured card take place. Hard inquiries appear on the report almost instantly.

- Days 30–45: Most lenders report account balances and payment statuses to the bureaus once a month. This is the standard window for a score to reflect a paid-off balance.

- Months 3–6: For a consumer with no history, this is the typical timeframe required for enough data to accumulate to generate an initial FICO® score.

- Year 1: Many secured cards are eligible for graduation to unsecured status. The "new credit" penalty from initial inquiries begins to fade.

- Years 7–10: This is the duration that most negative information (late payments, foreclosures, bankruptcies) remains on a report before federal law requires its removal.

Supporting Data: The Anatomy of a Score

To understand why these 15 strategies work, one must look at the statistical weight assigned to various financial behaviors.

| Factor | FICO® Weight | VantageScore® Impact |

|---|---|---|

| Payment History | 35% | Extremely Influential |

| Amounts Owed (Utilization) | 30% | Highly Influential |

| Length of Credit History | 15% | Moderately Influential |

| Credit Mix | 10% | Highly Influential |

| New Credit Inquiries | 10% | Less Influential |

Utilization Impact Case Study:

Consider two consumers, both with $1,000 in debt.

- Consumer A has a total credit limit of $2,000 (50% utilization).

- Consumer B has a total credit limit of $10,000 (10% utilization).

Despite having the same debt, Consumer B will likely have a score 40–60 points higher due to the lower utilization ratio.

Official Responses and Regulatory Context

The regulatory environment in 2026 has become increasingly protective of the consumer. The Fair Credit Reporting Act (FCRA) remains the bedrock of consumer rights, ensuring that individuals have the right to an accurate and private credit report.

CFPB Insights:

The Consumer Financial Protection Bureau has recently emphasized the importance of "Alternative Data." In a recent statement, regulators noted: "The inclusion of utility payments and rental data is a vital step in bridging the gap for the 26 million ‘credit invisible’ Americans who have historically been excluded from traditional banking systems."

The Industry Perspective:

Major lenders, including JP Morgan Chase and Bank of America, have responded to these trends by launching their own "low-barrier" credit products. Spokespersons for the American Bankers Association (ABA) suggest that while technology simplifies the process, the "golden rule" of credit—never borrowing more than one can repay—remains the most effective strategy in any era.

Implications: The Long-Term Value of Credit Health

The implications of maintaining a high credit score in 2026 extend far beyond the ability to buy a car or a house.

- The Cost of Capital: Over a lifetime, a person with an "Excellent" credit score (800+) is estimated to save over $250,000 in interest payments compared to someone with a "Fair" score (620).

- Employment and Housing: In many jurisdictions, employers and landlords use credit checks as a proxy for responsibility. A poor score can be a barrier to high-security jobs or desirable urban housing.

- The Digital Divide: As financial services become more automated, those with poor credit scores may find themselves "algo-locked" out of essential digital services, including certain fintech platforms and insurance products.

Conclusion

Building credit fast in 2026 requires a sophisticated understanding of how data is collected and reported. By combining foundational habits—such as 100% on-time payments—with modern tools like rent reporting and rapid rescoring, consumers can navigate the complexities of the financial system to secure their economic future. As the landscape continues to shift toward real-time data, the most successful consumers will be those who remain vigilant, informed, and proactive in managing their digital financial reputations.