: A Comprehensive Guide for Borrowers")

In an era defined by fluctuating interest rates and tightening lending standards, the relationship between a consumer and their credit score has become one of the most critical "partnerships" in adult life. Often viewed as a mere three-digit number, a credit profile is, in reality, a comprehensive narrative of financial trust, reliability, and future potential. As the calendar turns to February—a month traditionally synonymous with romance and the celebration of relationships—financial experts are urging consumers to pivot their focus toward "loving" their credit.

The following report explores the intricate dynamics of credit management, the historical evolution of consumer rights, and 14 actionable strategies to fortify one’s financial standing in a volatile economy.

Main Facts: The Intersection of Finance and Personal Well-being

Credit health is no longer a peripheral concern reserved for those seeking a mortgage. It impacts insurance premiums, employment opportunities, and even the ability to secure basic utilities without a deposit. According to recent consumer sentiment data, financial stress remains a leading cause of friction in interpersonal relationships. By prioritizing credit health, individuals are not merely managing a score; they are investing in their own peace of mind and the stability of their households.

The core of credit health rests on transparency and proactive management. Whether an individual is navigating the complexities of a shared financial life with a partner or maintaining a solo path, the principles of credit maintenance remain constant. The goal is to move from a defensive posture—reacting to financial crises—to an offensive strategy where credit serves as a tool for wealth generation.

Chronology: The Evolution of Credit and Consumer Protection

To understand the current state of credit management, one must look at the legislative and technological milestones that shaped the industry:

- 1970: The Fair Credit Reporting Act (FCRA): This landmark legislation established the right of consumers to see their own credit files and, crucially, the right to dispute inaccurate information. It shifted the power balance, ensuring that credit bureaus—TransUnion, Equifax, and Experian—were held to standards of accuracy and privacy.

- 1989: The Birth of the FICO Score: The introduction of a standardized scoring model by the Fair Isaac Corporation (FICO) revolutionized lending. It moved the industry away from subjective human judgment to a data-driven algorithm, though it also created a high-stakes environment where small errors could have outsized consequences.

- 2003: The FACT Act: This amendment to the FCRA allowed consumers to obtain one free credit report annually from each of the three major bureaus, fostering a new era of consumer self-monitoring.

- 2020–Present: The Post-Pandemic Shift: The global pandemic saw unprecedented shifts in credit reporting, including temporary pauses on student loan reporting and a surge in "Buy Now, Pay Later" (BNPL) services, which are only now beginning to integrate fully into traditional credit reporting.

Supporting Data and In-Depth Analysis: 14 Pillars of Credit Health

Achieving a "healthy relationship" with credit requires a multi-faceted approach. Below is an analysis of the 14 essential strategies for credit optimization:

1. The Audit: Quarterly Credit Reviews

Honesty is the bedrock of any relationship. Consumers should review their reports from all three bureaus at least quarterly. Data from the Federal Trade Commission (FTC) suggests that a significant percentage of credit reports contain errors. Identifying "unfair negative items"—such as accounts that don’t belong to you or outdated late payments—is the first step toward restoration.

2. The "Money Date": Strategic Budgeting

Budgeting should not be viewed as a restrictive chore but as a weekly or monthly "check-in." By reviewing checking, savings, and investment accounts regularly, consumers can align their daily spending with their long-term aspirations.

3. Payment History: The 35% Rule

Under the FICO model, payment history accounts for 35% of a total score. Even a single 30-day delinquency can cause a score to plummet by 50 to 100 points. Utilizing autopay and calendar alerts is a low-effort, high-reward strategy for maintaining this pillar.

4. Utilization Ratios: Managing the Balance

Credit utilization—the amount of revolving credit you use compared to your limits—accounts for 30% of your score. Experts generally recommend keeping this ratio below 30%, though "power users" often aim for under 10%. Paying balances down mid-cycle, before the statement date, can artificially lower reported utilization.

5. Preservation of Age: The Value of Longevity

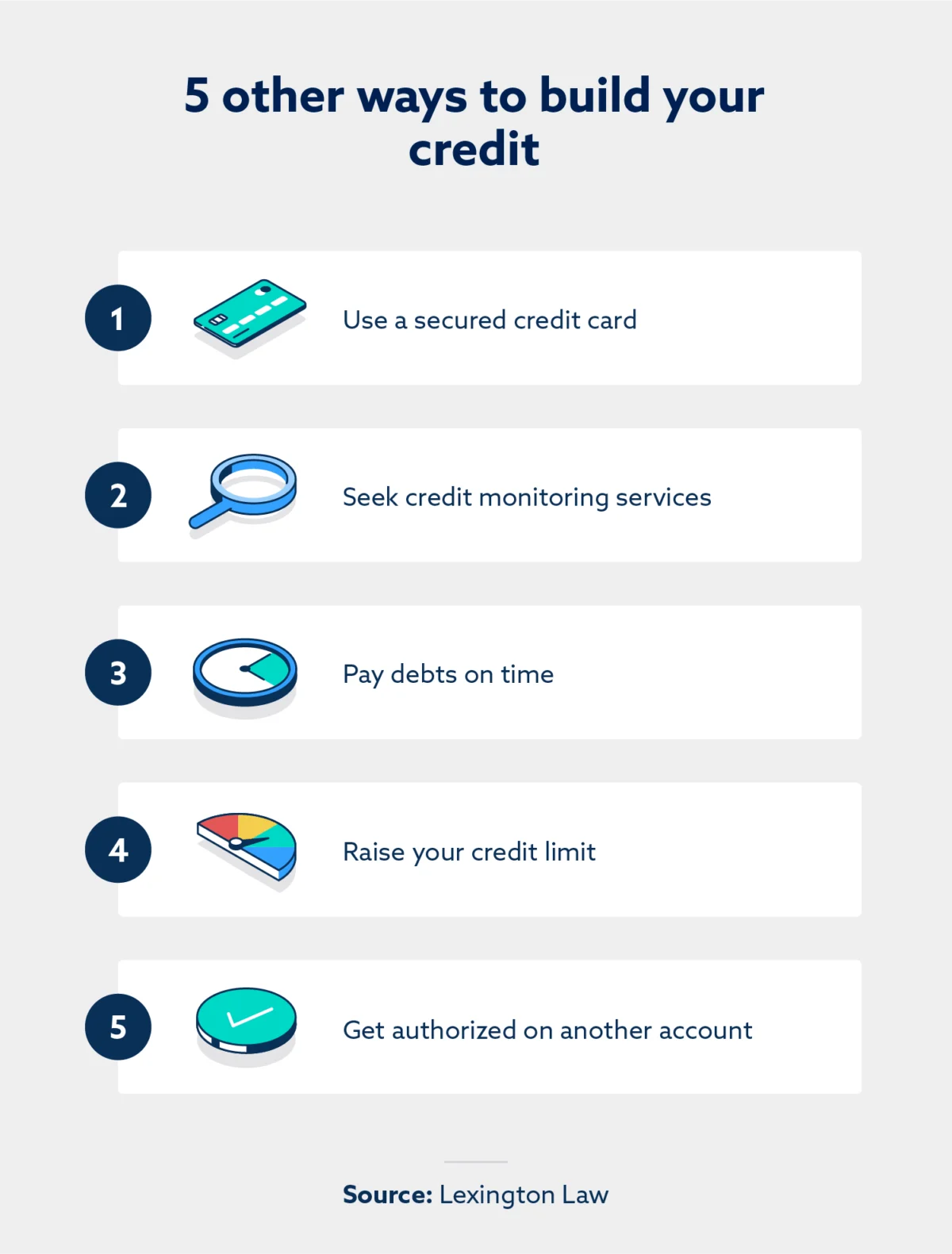

The length of credit history contributes 15% to a score. Closing an old, unused account can inadvertently shorten your average credit age and reduce your total available credit, negatively impacting your score. Unless an old card carries a high annual fee, it is often best to keep it open.

6. Behavioral Economics: Eliminating Temptation

Impulse spending is the enemy of credit health. Unsubscribing from retail marketing emails and removing "one-click" checkout options creates a "friction barrier" that encourages more mindful consumption.

7. The Liquidity Buffer: Emergency Funds

Financial reliance on credit cards often stems from a lack of liquid savings. Establishing even a modest emergency fund—starting with as little as $20 a month—can prevent an unexpected car repair from turning into high-interest debt.

8. Psychological Momentum: Celebrating Wins

Behavioral finance suggests that acknowledging small victories, such as paying off a minor balance or resisting an impulse buy, builds the psychological resilience needed for long-term financial discipline.

9. Radical Transparency in Partnerships

Financial "infidelity"—hiding debt or spending from a partner—is a primary driver of relationship breakdown. Open discussions about credit goals and existing liabilities are essential for couples planning a shared future.

10. The Risks of Co-signing

Joint accounts and co-signing tie two individuals’ financial reputations together. If one party defaults, both credit scores suffer equally. Consumers must establish clear "exit plans" and payment responsibilities before signing joint contracts.

11. Diversification: The Credit Mix

Lenders want to see that a consumer can handle different types of debt, such as revolving (credit cards) and installment (auto loans or mortgages). A healthy "mix" accounts for 10% of the score.

12. Advocacy Over Fear

Many consumers avoid their credit reports out of anxiety. However, the law provides protections against inaccurate or unfair reporting. Shifting from a mindset of fear to one of consumer advocacy is vital for those with "bruised" credit.

13. Low-Cost Experiences

Lifestyle creep can lead to credit strain. Prioritizing meaningful experiences—such as home-cooked meals or outdoor activities—over expensive commercial entertainment helps keep credit card balances manageable.

14. Professional Intervention

When credit reports are riddled with complex inaccuracies or the burden of debt becomes unmanageable, seeking professional help from reputable credit repair organizations or financial counselors is a legitimate and often necessary step.

Official Responses and Expert Perspectives

Regulatory bodies like the Consumer Financial Protection Bureau (CFPB) emphasize that credit reporting must be fair and accurate. In recent statements, the CFPB has increased scrutiny on how medical debt and "junk fees" impact credit scores, signaling a shift toward more consumer-friendly reporting standards.

Credit experts at firms like Lexington Law argue that the credit system is often "broken" for the average consumer, with automated systems frequently flagging legitimate activity as suspicious or failing to remove disputed items in a timely manner. Their stance is that "credit love" involves active defense—using the law to ensure that the story told by your credit report is both accurate and fair.

Implications: The Long-Term Forecast

The implications of a healthy credit profile extend far beyond the immediate ability to borrow. In a macro-economic sense, a population with high financial literacy and strong credit health leads to a more stable housing market and lower default rates.

On an individual level, the "compounding effect" of good credit is staggering. A consumer with a "Very Good" score (740+) may save hundreds of thousands of dollars in interest over the life of a 30-year mortgage compared to a consumer with a "Fair" score (580-669). This delta represents the difference between a retirement of ease and one of struggle.

As we move further into a digital-first economy, where "alternative data" (like rent and utility payments) is increasingly being used to calculate creditworthiness, the definition of credit will continue to expand. Those who take the time to "love" and nurture their credit today are not just fixing a number; they are securing their place in the future economy.

Final Thoughts

Credit is more than a metric of debt; it is a metric of opportunity. By treating credit management with the same care and attention one might give to a valued personal relationship, consumers can unlock a level of financial freedom that allows them to focus on what truly matters. Small, consistent actions—checking a report, paying on time, and communicating openly—are the building blocks of a lasting financial legacy.