Across the European continent, the Value Added Tax (VAT) serves as a primary pillar of government revenue. However, beneath the surface of these standardized tax regimes lies a complex patchwork of registration thresholds that fundamentally alter the landscape for small and medium-sized enterprises (SMEs). As countries attempt to balance administrative simplicity with the need for tax compliance, they have created a divergent reality where a business’s legal status—and its growth potential—is often dictated by a singular revenue limit.

The Landscape of European VAT Thresholds

When examining the 32 major European economies, a clear divide emerges regarding how nations treat micro-enterprises. At one end of the spectrum, countries like Switzerland offer a generous shield for small business owners, boasting the highest absolute VAT exemption threshold in Europe at CHF 100,000 (€106,724). This policy is designed to minimize the compliance burden for sole traders and micro-firms, allowing them to operate without the complex accounting requirements necessitated by VAT registration.

The United Kingdom and France follow closely in this ranking of nominal thresholds, with limits set at £90,000 (€105,043) and €87,000, respectively. These thresholds serve as a "safe harbor," shielding the smallest players from the administrative costs of tracking, collecting, and remitting tax on every transaction.

Conversely, some nations have opted for a "zero-tolerance" approach to tax administration. Spain and Turkey stand out as the only major European economies that do not provide an exemption threshold. In these jurisdictions, every business, regardless of size or annual turnover, is mandated to enroll in the VAT system. This policy ensures a broader tax base and total fiscal neutrality across the market, though it arguably imposes a disproportionate administrative burden on the smallest market entrants.

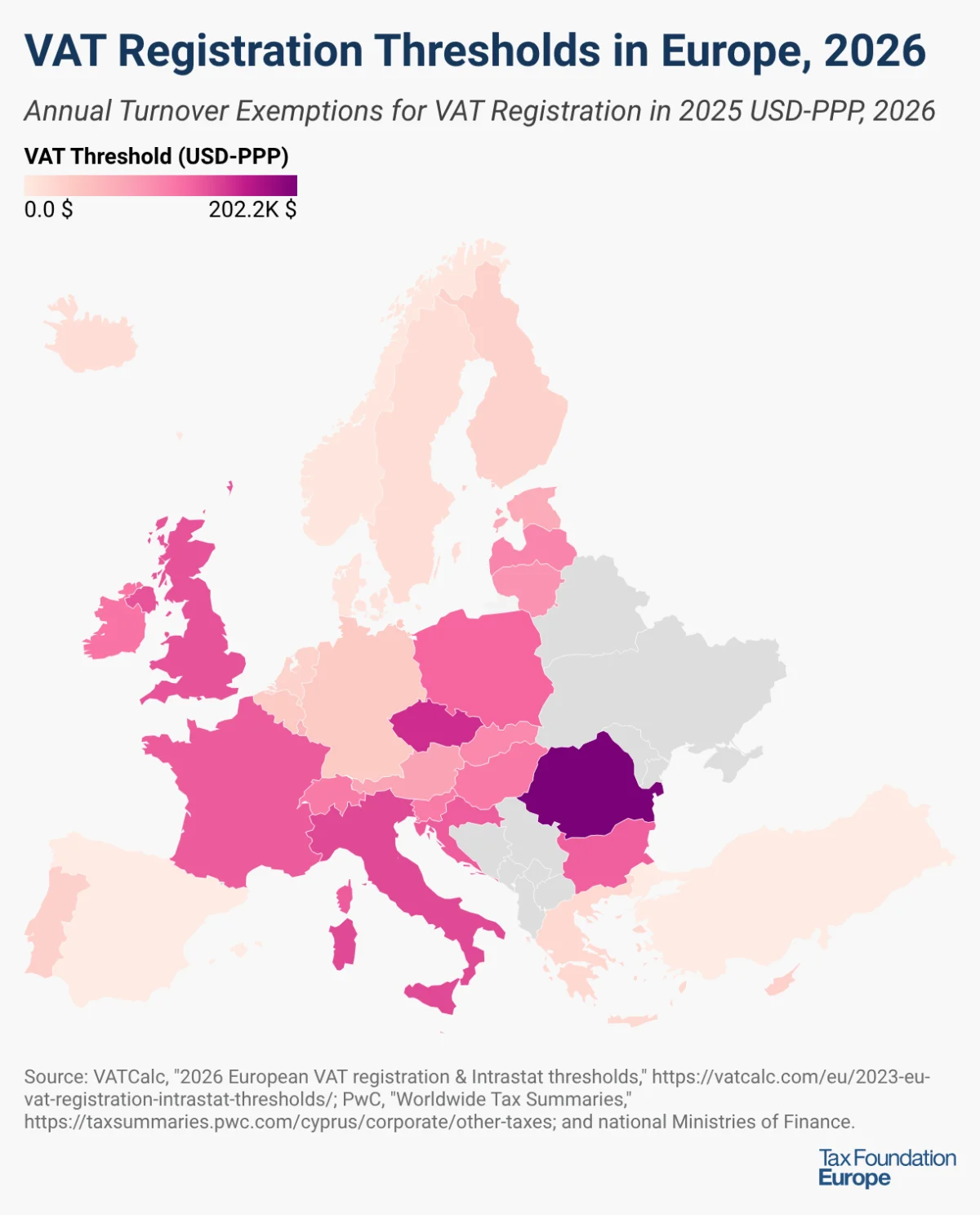

The Purchasing Power Parity (PPP) Perspective

Nominal figures, however, can be deceptive. A threshold that provides significant relief in a high-cost economy like Switzerland may have an entirely different economic impact in a country with lower price levels. When analysts adjust for Purchasing Power Parity (PPP), the map of European VAT policy shifts dramatically.

Romania currently leads the continent in terms of real-term exemption, with a threshold of RON 395,000 ($202,206) when adjusted for local purchasing power. The Czech Republic and Italy also occupy the top tier of this adjusted ranking, with thresholds of CZK 2,000,000 ($155,039) and €85,000 ($140,246), respectively. These figures suggest that in Central and Eastern Europe, policymakers are increasingly viewing high VAT thresholds as a vital tool for fostering entrepreneurship and local economic development, even if the absolute Euro values appear lower than those in Western Europe.

Chronology of Recent Legislative Shifts

The landscape of VAT thresholds is far from static. In recent years, a wave of legislative adjustments has swept across Europe, reflecting a trend toward raising thresholds to account for inflation and to support small business competitiveness.

- September 2025: Romania took a significant step by increasing its threshold from RON 300,000 to RON 395,000, signaling a commitment to reducing the compliance load for its rapidly growing SME sector.

- January 2026: Hungary initiated a phased increase of its threshold, moving from HUF 18 million to 20 million (€45,250 to €50,280). This roadmap includes a further scheduled increase to HUF 22 million (€55,310) by 2027.

- January 2026: Poland implemented a notable hike, raising its threshold from PLN 200,000 to 240,000 (€47,170 to €56,610), aimed at easing the tax administration burden for domestic entrepreneurs.

- April 2026: The Belgian parliament signaled a shift in policy by approving an increase in the VAT exemption threshold from €25,000 to €30,000. While the legislation is currently pending final entry into force, the intent to provide relief to micro-businesses is clear.

These sequential changes highlight a broader European consensus: as price levels and operational costs rise, the static thresholds of the past have become outdated, necessitating legislative intervention to prevent the "tax drag" that can stifle small businesses.

The Economic Implications: Efficiency vs. Distortion

While the political narrative surrounding these increases often centers on "supporting small businesses," economists warn of significant unintended consequences. VAT registration thresholds operate as a double-edged sword. On one hand, they undoubtedly reduce compliance costs for the smallest firms. On the other, they introduce profound market distortions.

The "Tax Cliff" and the Bunching Effect

The most critical issue with high thresholds is the creation of a "notch," or a tax cliff. Because VAT is a tax on value-added, a firm that earns one euro over the threshold suddenly becomes liable for tax on its entire turnover rather than just the marginal amount exceeding the limit. This creates a powerful, artificial incentive for firms to stay small.

Empirical evidence consistently confirms that firms will manipulate their behavior to remain beneath the threshold. This includes underreporting turnover or actively scaling back production. In the Czech Republic, this phenomenon is particularly visible. Economic data shows a sharp "bunching" of firms just below the VAT cutoff point. As the government has moved the threshold upward, this concentration of firms has migrated upward in tandem, proving that business behavior is being dictated by tax avoidance rather than market demand.

Competitive Distortions

Beyond individual firm behavior, high thresholds can lead to a "misallocation of resources." When tax advantages favor micro-enterprises, it can prevent the emergence of mid-sized firms that have the potential to scale. By artificially protecting smaller, less productive firms, these thresholds can crowd out more efficient, larger competitors who are forced to charge VAT, thereby creating an uneven playing field.

Official Responses and Policy Outlook

Policymakers face an increasingly difficult dilemma. The pressure to simplify the tax code for small businesses is immense, as is the political capital associated with "supporting the little guy." However, the fiscal cost of these exemptions—measured in lost VAT revenue—is non-trivial.

The consensus among tax experts at organizations like the Tax Foundation and the IMF is shifting toward a more cautious view. While acknowledging that compliance costs are a genuine burden, experts argue that the distortions created by high thresholds often outweigh the benefits. The primary recommendation from current fiscal research is for governments to consider lowering or even eliminating these thresholds entirely.

If thresholds must exist, experts suggest implementing "phase-out" mechanisms—where the tax burden increases gradually as a company grows—rather than the current "all-or-nothing" cliff. By smoothing the transition, governments could eliminate the incentive for firms to suppress their own growth.

Conclusion: The Future of VAT Compliance

As Europe moves toward a more integrated digital economy, the archaic nature of VAT thresholds becomes increasingly apparent. In an era of real-time digital reporting and automated accounting software, the administrative "burden" of VAT is shrinking. Consequently, the justification for high, distortive thresholds is weakening.

For the modern European policymaker, the challenge lies in decoupling tax policy from business-size manipulation. Whether through the complete elimination of thresholds, as seen in Spain and Turkey, or the adoption of smoother, graduated tax liabilities, the goal must be a neutral system. A tax code that encourages growth and rewards productivity—rather than one that incentivizes firms to remain perpetually small—is essential for the long-term health of the European economy. Until these cliffs are addressed, the "bunching" of firms will remain a testament to the fact that tax policy does not just fund the state; it fundamentally designs the marketplace.