Introduction

For decades, the "American Dream" was anchored in the ethos of the self-made individual—the idea that through grit, hard work, and determination, any citizen could ascend the economic ladder. However, a comprehensive new study suggests that the ladder’s rungs are growing further apart, and for many, the only way to reach the top is with a significant boost from the generation that came before.

A recent survey of 1,000 American adults conducted by Lexington Law Firm has pulled back the curtain on the mechanics of wealth building in the 21st century. The findings reveal a stark reality: financial success is increasingly tethered to "intergenerational transfers"—cash infusions from parents—rather than mere salary growth. As the cost of living outpaces wage increases by nearly 20 percent over the last four years, the path to financial autonomy is being fundamentally rewritten, creating a widening chasm between those with family safety nets and those without.

Main Facts: The End of the Self-Made Era?

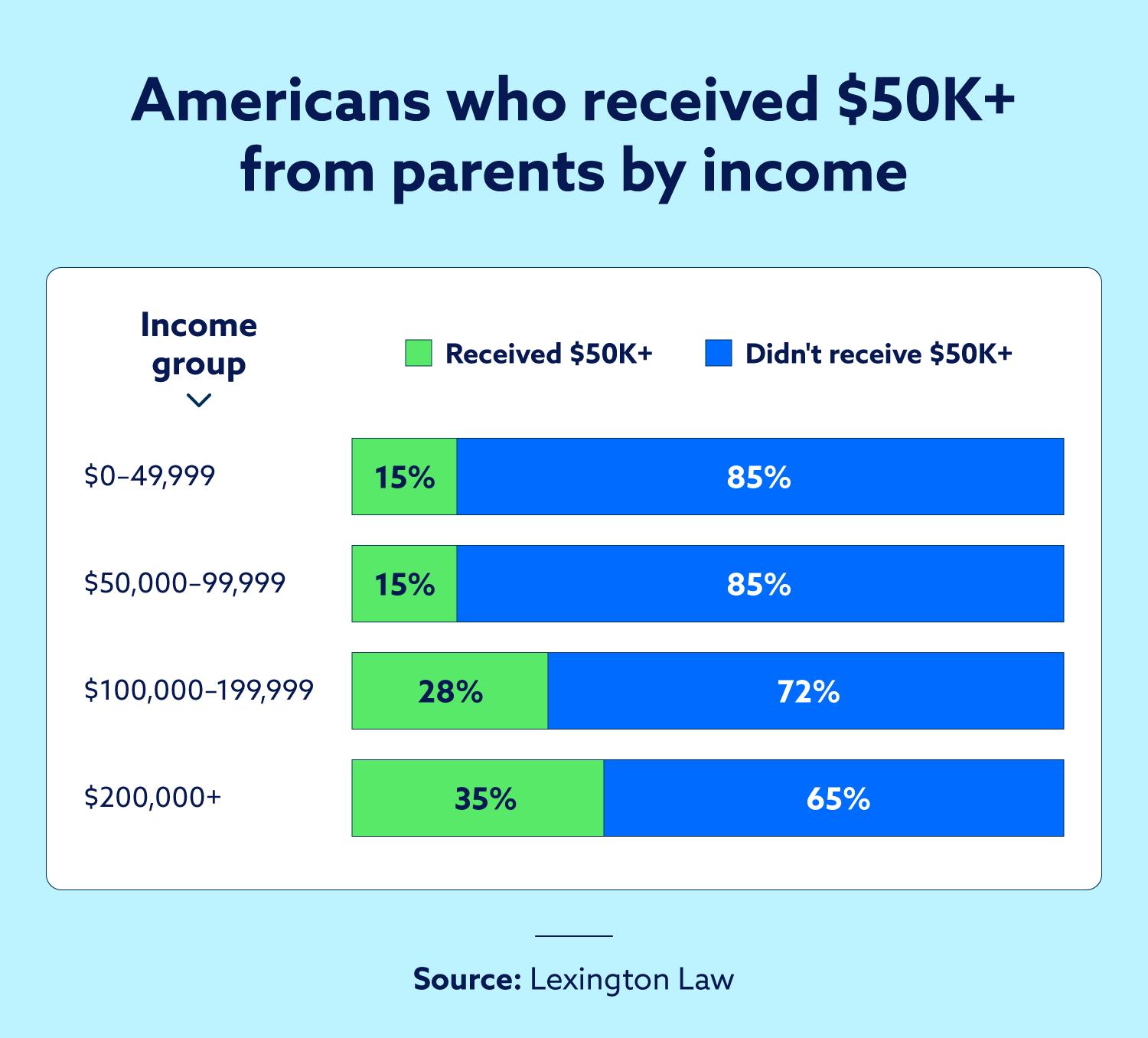

The most striking revelation from the data is the correlation between high-income status and parental assistance. While the archetype of the high-earner often involves stories of "bootstrapping," the survey data tells a different story. Individuals earning $125,000 or more per year are 2.5 times more likely to have received significant financial help—defined as $50,000 or more—from their parents. Specifically, 36 percent of high earners reported this level of support, compared to just 14 percent of those in lower-income brackets.

This "head start" provides more than just immediate liquidity; it offers a structural advantage that compounds over time. Whether used for a down payment on a home, the elimination of student loan debt, or seed money for a business, these five-figure transfers allow recipients to bypass the high-interest debt traps that frequently stall the progress of their peers.

The survey also highlighted a surprising psychological paradox among the youngest cohort. Despite acknowledging a "rigged" economic system, Gen Z remains remarkably optimistic. An overwhelming 87 percent of Gen Z respondents believe they will be as successful as, or more successful than, their parents. This optimism persists even though 72 percent of the same group believe the current economic system is unfairly weighted in favor of older generations. This suggest that for the youngest workers, success is no longer viewed as a product of the system, but rather a result of navigating around its flaws—often with family help.

Chronology: The Economic Evolution of Independence

To understand why the "Bank of Mom and Dad" has become a vital pillar of the American economy, one must look at the chronological shift in how wealth has been accumulated over the last sixty years.

The Post-War Golden Age (Baby Boomers):

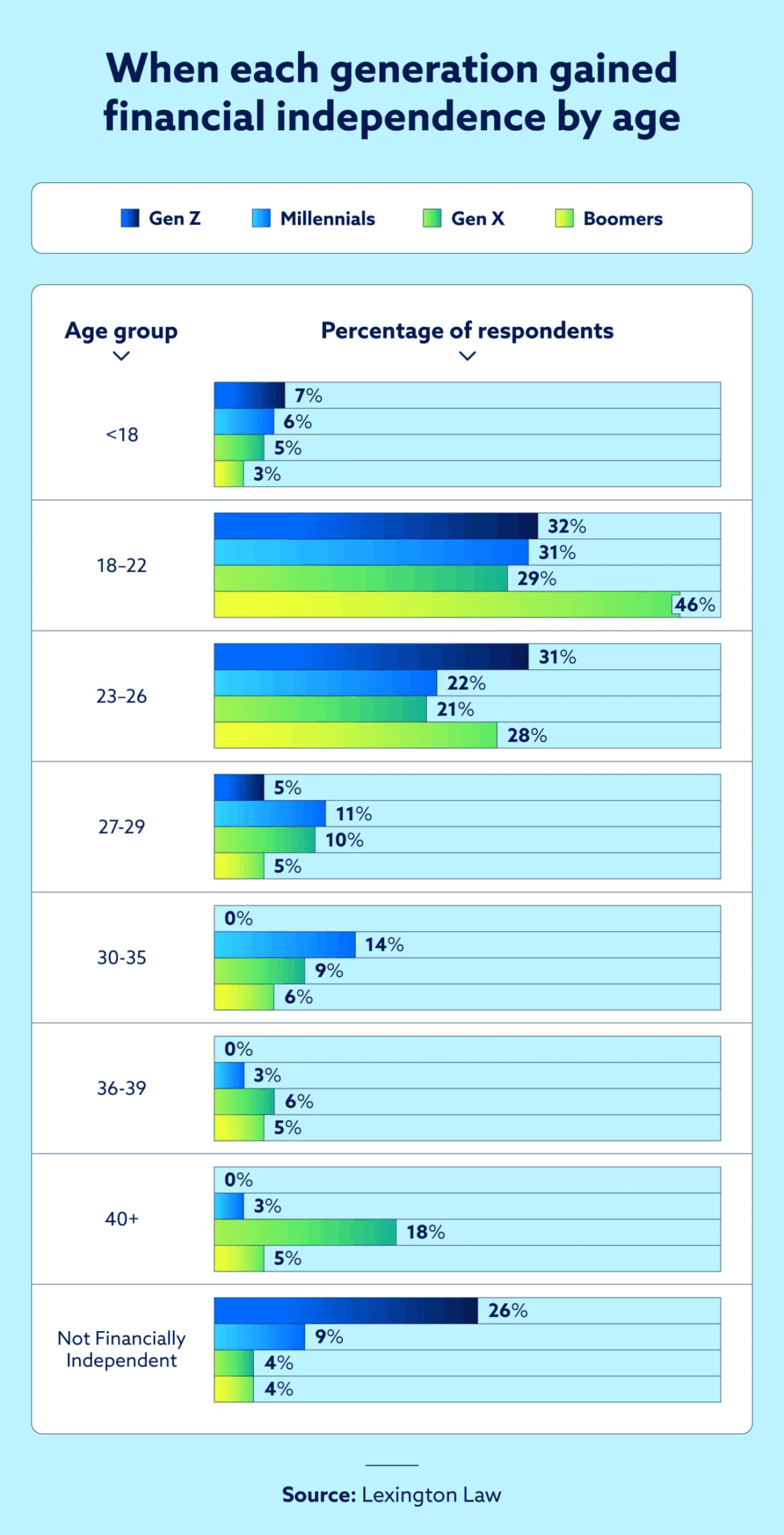

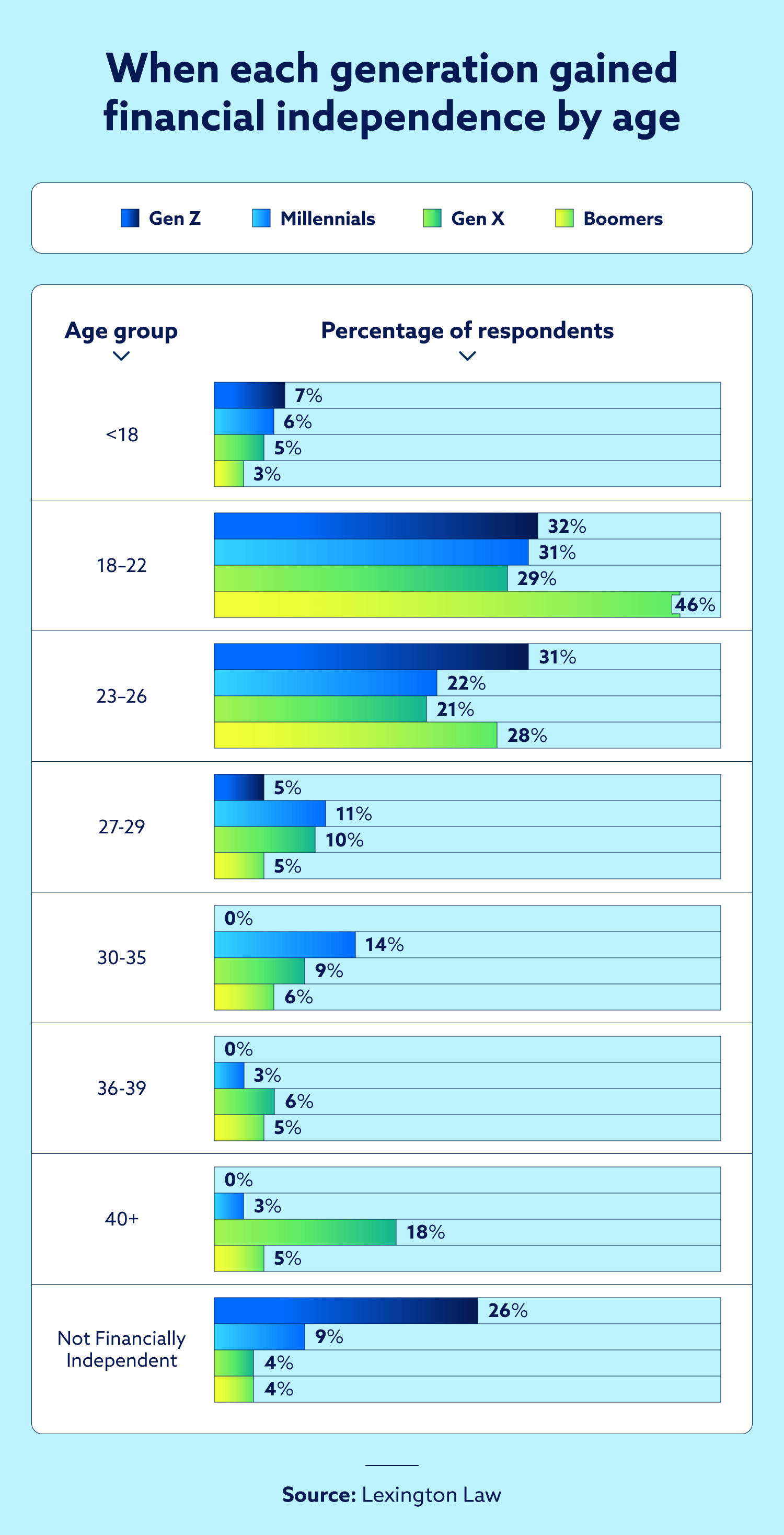

Following World War II, the American economy experienced unprecedented expansion. For the Baby Boomer generation, the path to independence was swift. The survey confirms this, showing that nearly 48 percent of Boomers achieved full financial independence by the age of 22. During this era, a single-income household could often afford a home, a car, and a college education with minimal debt, thanks to robust federal investments and a lower cost of living relative to wages.

The Transition Years (Gen X):

As Gen X entered the workforce in the 1980s and 90s, the economic landscape began to shift toward financialization. While Gen X currently reports the highest earnings—with 54 percent making over $100,000—they also represent the first generation to feel the "squeeze." They were the primary recipients of parental support during their middle-age years, with 23 percent receiving over $50,000, yet they maintain the bleakest outlook. This suggests that for Gen X, wealth is often tied up in the "sandwich generation" struggle: supporting both aging parents and adult children.

The Great Recession and the Inflationary Surge (Millennials and Gen Z):

The 2008 financial crisis served as a pivot point, permanently altering the trajectory of Millennial wealth. By the time Gen Z reached adulthood, the cost of living had surged. According to the U.S. Bureau of Labor Statistics, the last four years alone have seen a 20 percent spike in essential costs. Consequently, the age of independence has been pushed back significantly. Only 36 percent of Gen Z reached independence between the ages of 23 and 29, and more than a quarter still rely on parental support well into their late 20s.

Supporting Data: The Anatomy of Financial Obstacles

The Lexington Law survey provides a granular look at the specific hurdles preventing Americans from building a "wealth fortress." When asked to identify the primary roadblocks to financial security, the responses were remarkably consistent across generational lines, though the intensity of certain concerns varied.

- The Cost of Living Crisis: 73 percent of all respondents cited the rising cost of everyday goods—from groceries to gasoline—as the number one obstacle to saving.

- The Housing Barrier: 65 percent identified housing costs as a major deterrent. With home prices reaching record highs and mortgage rates remaining elevated, the traditional "starter home" has become a luxury asset.

- Stagnant Wages: Despite low unemployment rates, 49 percent of respondents feel their wages have not kept pace with inflation, effectively resulting in a loss of purchasing power year-over-year.

- The Healthcare Burden: For Baby Boomers, the primary concern shifts from housing to healthcare. 62 percent of Boomers named medical costs as their greatest financial threat, highlighting the fragility of wealth in the face of aging.

The data also reveals a shift in the "independence timeline." The survey found that 26 percent of those earning between $125,000 and $149,000 did not achieve financial independence until age 40 or older. This suggests that even high-paying professional roles are no longer a guarantee of early autonomy; rather, they are often used to play "catch-up" for decades of accumulated debt.

Official Responses and Expert Perspectives

The findings of the Lexington Law survey align with recent reports from major federal institutions, which have expressed growing concern over the "wealth gap."

The U.S. Federal Reserve has noted in its recent publications on the economic well-being of households that the long-term effects of the 2008 recession, combined with the post-pandemic housing shortage, have created a "lock-in effect." This prevents younger workers from building equity, which was the primary vehicle for Boomer wealth.

The U.S. Department of the Treasury has also weighed in, noting that the "well-being of young adults" is increasingly dependent on family resources. Economists at the Treasury suggest that this creates a cycle of "inherited meritocracy," where the ability to take risks—such as starting a business or moving to a high-opportunity city—is reserved for those with familial financial backing.

Financial analysts at Lexington Law emphasize that while these macro-economic factors are daunting, they underscore the importance of individual credit health. "Building wealth isn’t just about what you earn; it’s about the cost of the money you borrow," the report notes. In an environment where parental support is the great divider, those without it must rely on a clean credit report to access lower interest rates, which can save hundreds of thousands of dollars over a lifetime.

Implications: The Future of Social Mobility

The implications of this survey are profound for the future of the American social contract. If the primary predictor of high-income status is a $50,000 gift from a parent, the concept of social mobility becomes increasingly fragile.

1. The Stratification of the Middle Class:

We are seeing the emergence of two distinct "middle classes." One is fueled by inherited assets and parental safety nets, allowing for homeownership and aggressive retirement investing. The other is a "working professional" class that, despite high salaries, remains in a perpetual state of "renting" their lifestyle due to debt and the lack of a family buffer.

2. The Redefinition of Success for Gen Z:

Gen Z’s optimism in the face of a "rigged" system suggests a shift in mindset. Younger Americans may be moving away from the idea of "beating the system" and toward a strategy of "hacking" it—prioritizing gig work, digital nomadism, and living with parents longer to bypass the traditional expenses that drained previous generations.

3. Policy Pressure:

The data puts immense pressure on policymakers to address the "big three" costs: housing, healthcare, and education. As long as these costs remain untethered to wage growth, the "generational gap" will continue to widen, making parental support a requirement rather than a bonus.

4. The Critical Role of Financial Literacy and Credit:

For those who do not have the luxury of a $50,000 parental transfer, the margin for error is razor-thin. The survey highlights that in a high-cost economy, financial tools like credit repair and strategic budgeting are no longer optional "extras"—they are essential survival skills.

Conclusion

The Lexington Law survey serves as a sobering reminder that the American economic engine is changing. While the spirit of optimism remains alive in the younger generations, the structural reality is that wealth is becoming a family affair. As financial independence arrives later and the cost of living continues its upward trajectory, the ability to build a stable financial future will depend on a combination of systemic reform, individual credit management, and—for the lucky few—the "Bank of Mom and Dad." For the rest, the climb has never been steeper.