PNC Financial Services Group, the Pittsburgh-based super-regional banking giant with $603 billion in assets, has officially launched its next-generation mobile banking application. This rollout represents more than a mere cosmetic update; it is a fundamental reimagining of the digital banking experience, powered by a pioneering "agentic" artificial intelligence development process and a strategic mandate to transform the smartphone into the bank’s "most important branch."

As the financial services industry grapples with the dual pressures of rising consumer expectations and the rapid evolution of generative AI, PNC’s new app seeks to strike a delicate balance: providing a feature-rich, high-utility environment that remains intuitive and uncluttered. By leveraging data-driven insights and a highly customizable interface, PNC aims to deepen its relationship with its 8 million active mobile users while setting a new standard for how traditional institutions compete with agile neobanks.

Main Facts: The Evolution of the "Most Important Branch"

The new PNC mobile app is the culmination of a multi-year digital transformation strategy. At its core, the project was designed to solve a perennial problem in financial technology: "feature creep." As banks add more services—from investment accounts to insurance and sophisticated payment rails—mobile interfaces often become "heavy," bogged down by labyrinthine menus and confusing navigation.

Alex Overstrom, PNC’s Head of Retail Banking, emphasized that the primary objective was to maximize capability without overwhelming the user. The bank’s solution is a "light" architecture that allows clients to design their own experience. Key features of the new rollout include:

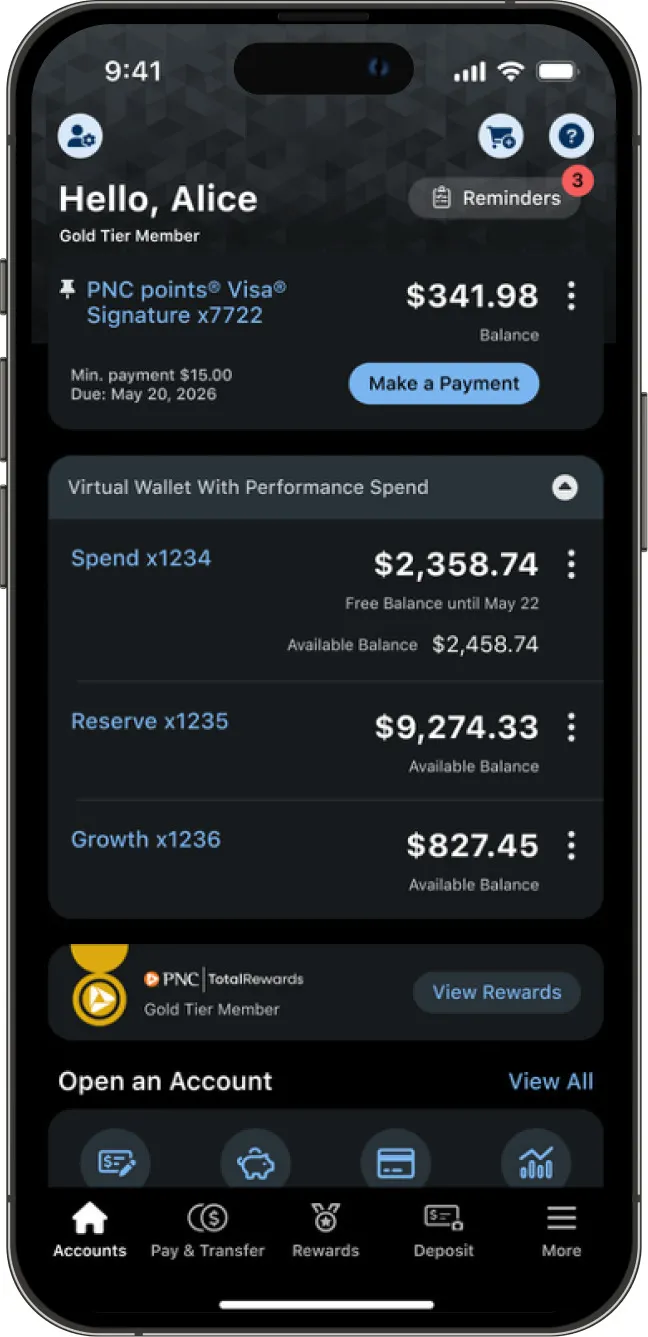

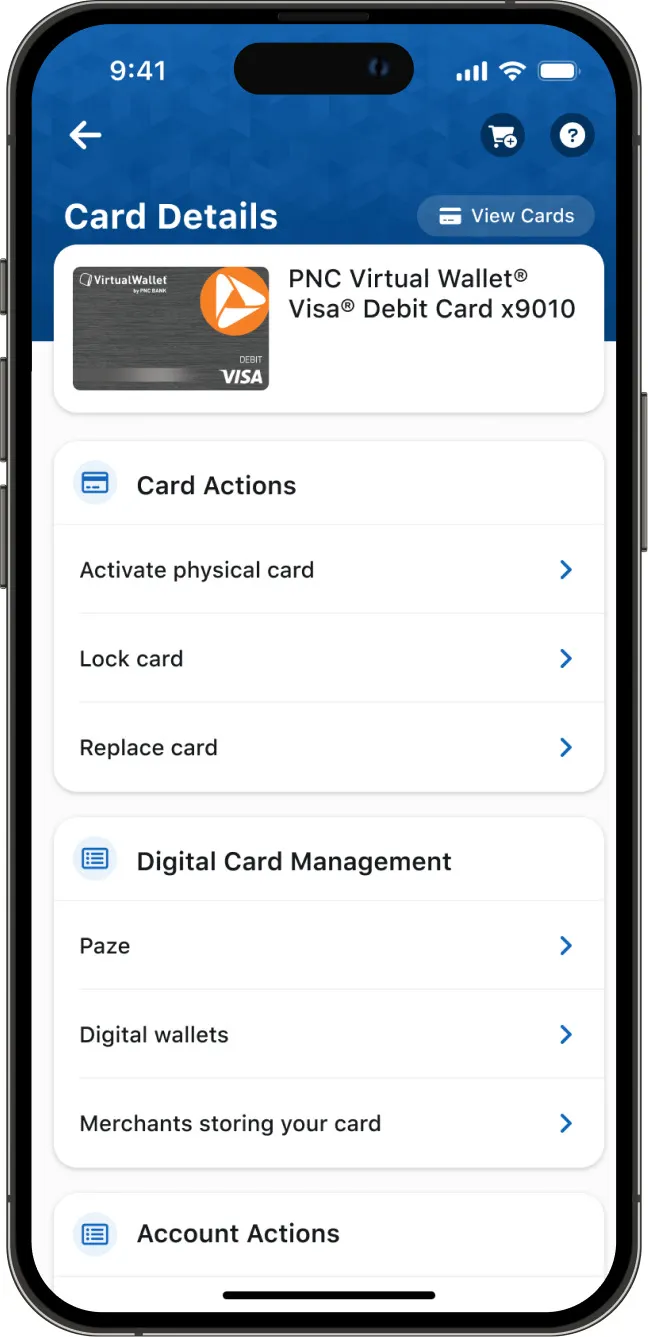

- User-Centric Customization: A revamped navigation framework that allows customers to prioritize the tools they use most, reducing the need to navigate through multiple menu layers.

- Data-Driven Insights: The integration of predictive analytics that offer customers personalized financial advice and alerts based on their specific spending behaviors and transaction history.

- "Dark Mode" Implementation: Responding to the single most-requested feature from its user base, PNC has integrated a native dark mode to improve accessibility and visual comfort.

- Frictionless Product Integration: The app now allows for the seamless opening of investment accounts and credit cards, a move intended to "catch up" to competitors and capture more of the customer’s total financial life within a single ecosystem.

- Agentic AI Origins: Perhaps most significantly from a technical standpoint, the app was built using 115 autonomous AI agents, marking a significant shift in how the bank handles software development and testing.

The rollout is currently underway in phases. Initial access has been granted to recently converted FirstBank customers and clients in select markets, with full availability for all retail and small business customers expected by the end of the summer.

Chronology: A Multi-Year Digital Transformation

The path to this launch was not a sudden sprint but a calculated, multi-stage marathon. To understand the significance of the new app, one must look at the timeline of PNC’s technological overhaul:

2022–2023: Modernizing the Foundation

Before the consumer-facing app could be reimagined, PNC had to address its legacy "back-end" systems. Throughout 2022 and 2023, the bank focused on modernizing its data centers and core digital infrastructure. This effort was critical to ensuring that the front-end experience would be backed by the reliability and speed required for a national footprint.

Late 2023: The New Online Banking Platform

Following the back-end modernization, PNC released a revamped online banking platform. This served as a testing ground for the new navigation philosophy and allowed the bank to introduce incremental capabilities at a faster cadence. It established the design language that would eventually migrate to the mobile environment.

January 2024: Strategic Investment Announcements

During the bank’s fourth-quarter earnings call in January, CEO Bill Demchak signaled the bank’s aggressive tech posture, announcing a $3.5 billion annual technology budget. He indicated that this spend would increase by approximately 10% in 2024, with a significant portion of that growth dedicated specifically to artificial intelligence.

July 2024: The Phased Mobile Launch

PNC officially announced the rollout of the new mobile app on Tuesday. By starting with FirstBank customers—who were already undergoing a transition—PNC was able to monitor the app’s performance in a controlled environment before expanding to its broader 8-million-user base.

Supporting Data: The Tech Spend and the "Agentic" Shift

PNC’s commitment to this digital evolution is backed by substantial financial and operational data. The bank’s $3.5 billion annual technology budget places it among the top spenders in the regional and super-regional banking space.

The AI Agent Ecosystem

The development of the app utilized a cutting-edge methodology known as "agentic AI." PNC deployed 115 AI agents to autonomously manage various stages of the software development life cycle (SDLC).

- Functionality: These agents handled tasks ranging from initial coding to rigorous stress testing and bug detection.

- Human-in-the-Loop: While the agents performed the heavy lifting, Overstrom noted that human developers reviewed every output, ensuring that the AI’s speed was balanced by human oversight for security and accuracy.

- Efficiency Gains: This upfront investment in an AI ecosystem has allowed the bank to transition to a continuous delivery model, where new features can be added in weeks rather than months.

Growth Metrics

The demand for these digital tools is evident in PNC’s performance metrics. In the first quarter of the year, PNC saw an 8% year-over-year jump in active mobile users. With 8 million customers currently utilizing the mobile platform, the bank views the app not just as a convenience, but as a primary engine for customer retention and cross-selling.

Official Responses: Insights from PNC Leadership

The leadership at PNC has been vocal about the philosophy driving these changes. Alex Overstrom has been clear that the app is intended to eliminate the "friction" that often drives customers into physical branches for simple tasks.

"What I’m trying to avoid is seven layers of menus to get to something," Overstrom said in a recent interview. "The challenge we gave to the team is, how do we add a whole bunch more into the app… without making it overwhelming for our customers?" He described the app as a "living" platform, noting that the goal is for customers to be able to do anything in the app that they could do with a human agent or at a physical branch.

From a high-level strategic perspective, CEO Bill Demchak has linked these technological advancements to the bank’s broader national expansion. He noted that AI is responsible for roughly 20% of the increase in the bank’s tech budget this year, highlighting it as a core pillar of PNC’s competitive strategy.

CFO Rob Reilly has also emphasized the necessity of these investments for a bank with a national footprint. During an investor conference in February, Reilly pointed out that a "national footprint requires" a refreshed and reliable data center network to support continuous operations. This infrastructure is what allows the mobile app to function as a "24/7 branch" across different time zones and demographics.

Implications: The Future of "Frictionless" Banking

The launch of PNC’s new app has several long-term implications for the bank and the wider financial sector:

1. The Marginalization of the Physical Branch

By aiming for a "100% parity" between the app and the branch, PNC is acknowledging a shift in consumer behavior where the physical branch becomes a venue for complex advisory services rather than transactional banking. If the app can successfully handle 90% of customer needs with "one or two clicks," the operational cost of retail banking could shift dramatically.

2. AI as a Competitive Moat

PNC’s use of 115 AI agents for development marks a turning point for legacy institutions. If super-regionals can use AI to match the development speed of fintech startups, they can leverage their massive balance sheets and existing customer trust to regain an edge. The ability to add "incremental features" quickly means PNC can react to market trends in real-time.

3. The Arrival of the Digital Assistant

Later this year, PNC plans to roll out its own digital assistant. While Overstrom has been careful not to label it a "chatbot," the implication is a move toward "conversational banking." This assistant will likely use the same data-driven insights currently being integrated into the app to provide proactive financial coaching.

4. Hyper-Personalization as Retention

In an era where "switching costs" between banks are lowering due to open banking initiatives, personalization is the new "sticky" feature. By allowing users to design their own interface and providing them with insights based on their specific behaviors, PNC is attempting to create an emotional and functional "lock-in" that a generic banking app cannot provide.

Conclusion

PNC’s new mobile app is a bold statement of intent. It reflects a bank that is no longer content with simply "having an app," but one that views its digital interface as the primary battlefield for customer loyalty. Through the innovative use of agentic AI and a relentless focus on reducing user friction, PNC is positioning itself to lead the next era of digital-first, super-regional banking. As the phased rollout continues through the summer, the industry will be watching closely to see if this "light" yet powerful approach can indeed deliver the "most important branch" directly into the pockets of millions.