July 16, 2026 — In a move that consumer advocates are calling a "predatory pivot," Opportunity Financial (OppFi), a prominent fintech lender known for offering high-cost installment loans, has petitioned the Trump Administration for approval to acquire BNC Bank. If successful, the acquisition would transform the institution into "OppFi Bank," effectively granting the lender a national banking charter.

For critics, this is not merely a corporate merger; it is a strategic maneuver designed to circumvent state-level interest rate caps. By federalizing its operations, OppFi could potentially bypass usury laws in 45 states that currently restrict the triple-digit Annual Percentage Rates (APR) that have become the firm’s hallmark. As the deadline for public comment approaches, a coalition of advocates is sounding the alarm, warning that the federal government stands at a crossroads: either uphold consumer protections or greenlight a "rent-a-bank" scheme that could institutionalize predatory lending nationwide.

The Mechanics of the Bid: A Regulatory Loophole?

At the heart of the controversy is the concept of "preemption." Under current banking regulations, national banks—entities chartered and regulated by federal agencies like the Office of the Comptroller of the Currency (OCC)—often enjoy a degree of exemption from state-level interest rate restrictions.

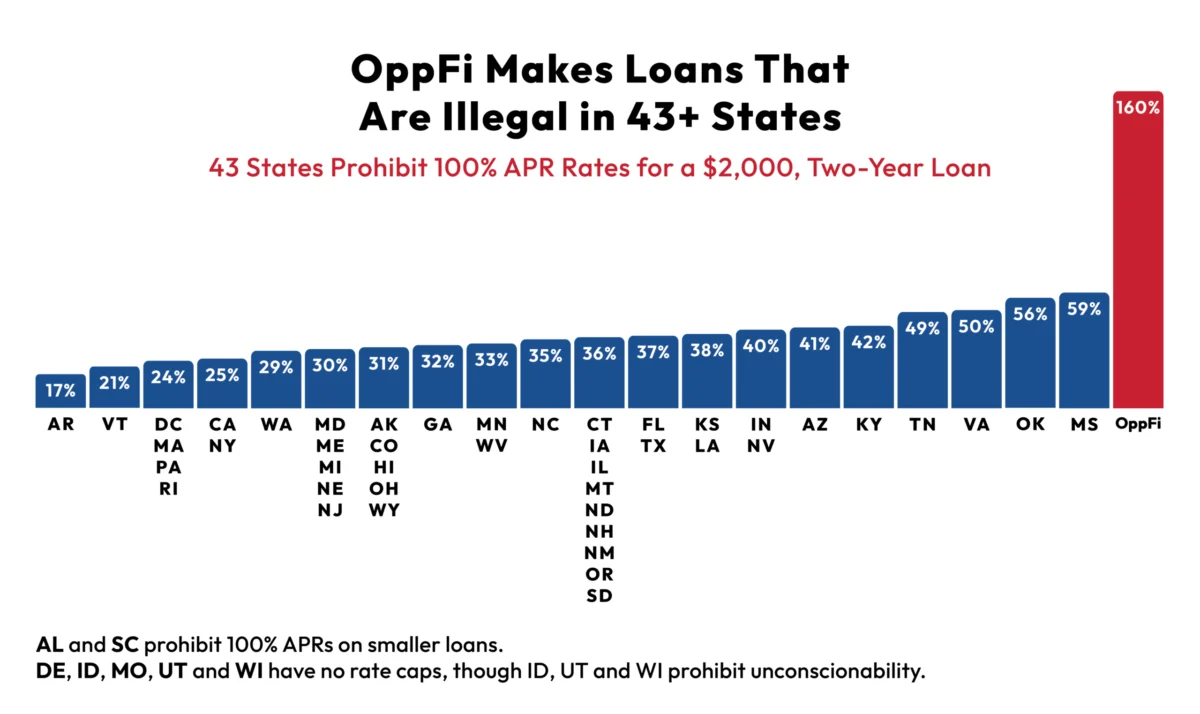

OppFi’s business model currently relies on charging interest rates that frequently exceed 160% APR. In the 45 states where such rates are deemed usurious and prohibited, OppFi currently faces significant operational headwinds. By acquiring BNC Bank, OppFi would gain the regulatory shield of a national charter. This would allow the company to export its high-interest rate products into states that have specifically voted to ban such predatory lending practices, effectively nullifying the legislative will of millions of citizens and their elected representatives.

Chronology of a High-Stakes Acquisition

The bid for BNC Bank is part of a broader, concerning trend within the fintech lending sector.

- Mid-2020s: As state legislatures tightened regulations on "payday-style" installment loans, fintech lenders began seeking more permanent regulatory solutions to maintain their profit margins.

- The Enova Precedent: Earlier this year, Enova—the parent company of CashNetUSA, NetCredit, and OnDeck—initiated a similar bid to acquire Grasshopper Bank. This move signaled a shift in industry strategy: moving away from traditional fintech lending partnerships toward full-scale bank ownership.

- July 2026: OppFi formally submitted its application to the federal banking regulators—the Federal Reserve, the OCC, and the FDIC—seeking approval for the BNC Bank acquisition.

- July 16, 2026: The public comment period is officially underway, with deadlines staggered through mid-August. Advocates are mobilizing, framing this as a defining moment for the American banking system.

Supporting Data: The Reality of Triple-Digit APRs

The financial impact of 160% APR loans on vulnerable populations cannot be overstated. According to data from the National Consumer Law Center (NCLC), loans with these interest rates create a structural "debt trap" from which many borrowers find it impossible to escape.

A $1,000 loan at 160% APR, if not repaid immediately, can balloon into a multi-thousand-dollar liability within months. These products are often marketed to individuals with limited access to traditional credit, effectively preying on those who are already struggling to cover fundamental living expenses such as rent, groceries, and utilities.

Furthermore, the industry’s push into "earned wage payday loans" suggests an intent to expand these products into every corner of the American market. If the acquisition is approved, OppFi intends to utilize the bank charter to launch these products across all 50 states, formalizing a system where the most expensive credit is marketed to the least financially secure consumers.

The Implications for the Banking Industry

The potential approval of this acquisition carries profound implications for the integrity of the U.S. banking system. Traditionally, national banks have been viewed as stewards of financial stability, tasked with fostering economic health and providing accessible credit.

Eroding the "National Bank" Brand

Critics argue that allowing a lender with a 160% APR business model to carry the title of a "National Bank" fundamentally degrades the reputation of the industry. It risks conflating traditional banking—which involves deposit-taking, mortgage lending, and business services—with predatory, high-risk, high-cost lending.

The Regulatory Race to the Bottom

If the federal government approves the OppFi and Enova bids, it may trigger a "race to the bottom." Other lenders currently constrained by state laws may feel emboldened to seek their own bank charters, leading to a landscape where predatory lending becomes the standard, rather than the exception, in the American retail credit market.

Official Responses and the Public Mandate

As of mid-July 2026, the regulatory agencies remain in the midst of the review process. The FDIC, OCC, and Federal Reserve are obligated to weigh the "convenience and needs" of the community, as well as the safety and soundness of the institutions involved.

Consumer advocates contend that the "needs" of the community are not met by high-interest debt traps that ruin credit ratings. Instead, they argue that these acquisitions are contrary to the public interest and undermine the regulatory framework designed to protect consumers from financial exploitation.

How to Make Your Voice Heard

The window for public input is narrow, and regulators are required to review the comments submitted. The advocacy community is urging the public to provide specific examples of financial harm caused by predatory lending, emphasizing that these comments carry significant weight in the final decision-making process.

- FDIC: Comments are due by July 29.

- OCC: Comments are due by August 5.

- Federal Reserve: Comments are due by August 13.

Conclusion: A Turning Point for Consumer Rights

The struggle over OppFi’s acquisition of BNC Bank is a litmus test for the current administration’s commitment to consumer protection. For many, the question is simple: Should the federal government provide the legal infrastructure for companies that profit from the financial distress of the working class?

The precedent set by the approval—or rejection—of this bid will likely dictate the landscape of personal finance for the next decade. If the regulators say "no," it will reinforce the power of states to protect their residents from predatory interest rates. If they say "yes," it will signal that the federal government is willing to prioritize the expansion of fintech lenders over the financial health of the American consumer.

As the summer of 2026 continues, the eyes of the financial world are fixed on Washington. The message from consumer advocates is clear: The banking charter is a privilege, not a right, and it should not be granted to institutions that build their business model on the erosion of financial stability. It is now up to the public to ensure that regulators hear this message before the deadline for intervention passes.