In the modern global economy, research and development (R&D) serves as the lifeblood of competitive advantage. As nations vie for technological supremacy, governments have increasingly turned to the tax code as a primary lever to stimulate private sector innovation. However, a deep dive into the latest data reveals a fragmented landscape where the generosity of R&D tax relief varies wildly—from minimal support in some jurisdictions to aggressive, subsidy-heavy regimes in others.

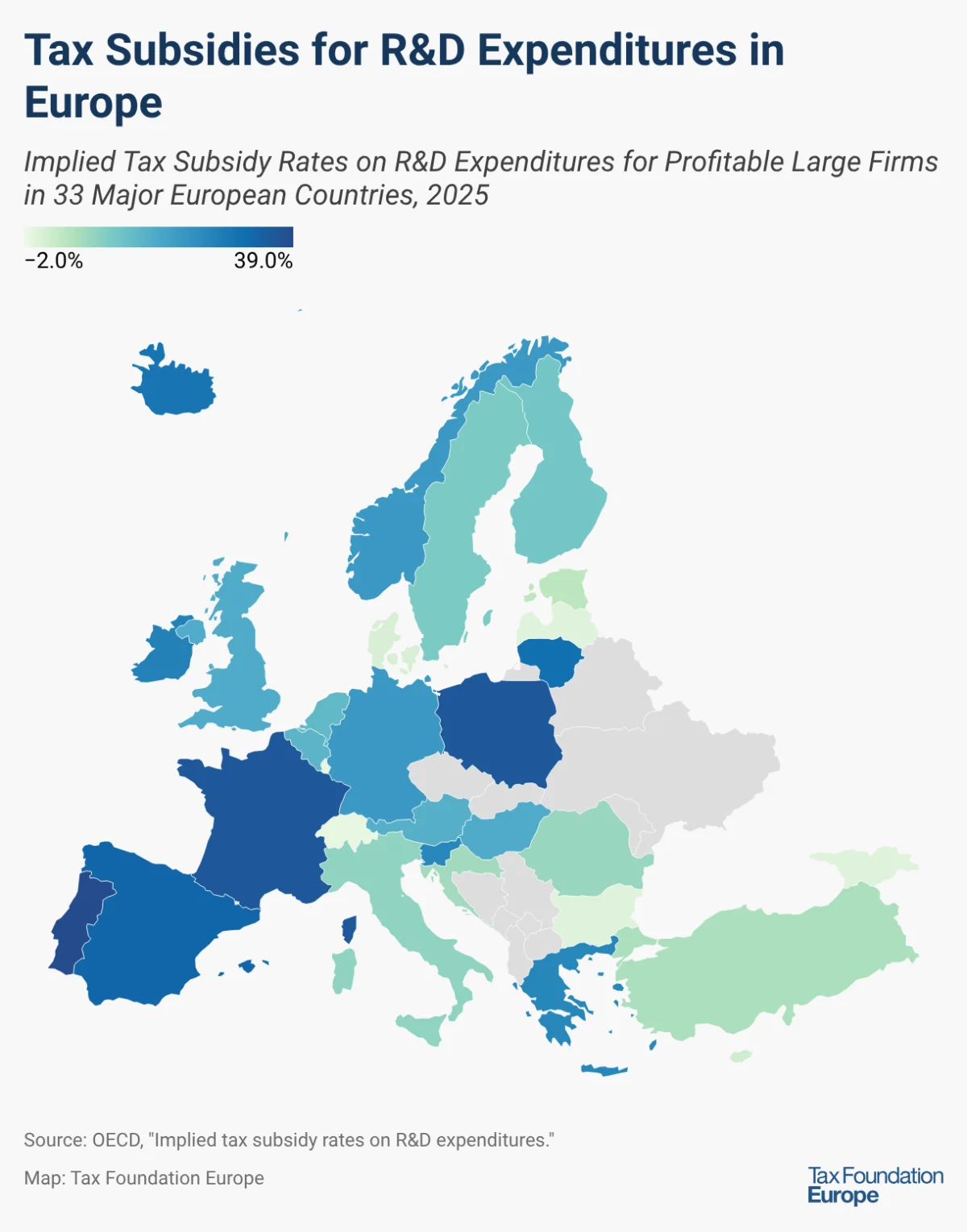

As of 2025, the average implied subsidy rate for large, profitable firms across 33 major European economies sits at 16 percent. Yet, this headline figure masks a vast spectrum of policy choices that carry significant implications for fiscal health, administrative complexity, and the genuine promotion of innovation.

The Global Disparity: Who Leads the Subsidy Race?

The variation in implied tax subsidy rates—a metric representing the reduction in the cost of R&D investment due to tax relief—is stark. Among nations offering notable support, Portugal currently stands as the most generous, boasting an implied subsidy rate of 39 percent. France and Poland trail closely behind, each offering a 36 percent subsidy rate.

At the other end of the spectrum, some countries offer only nominal relief. Denmark, for instance, provides a 1 percent subsidy rate, while Cyprus and Estonia hover at 2 and 4 percent, respectively. Furthermore, a group of nations—including Bulgaria, Georgia, Latvia, Luxembourg, Malta, and Switzerland—maintain tax regimes that show no significant expenditure-based R&D tax relief, signaling a preference for neutral tax structures over targeted incentives.

The global context is equally revealing. While Europe averages a 16 percent subsidy, the United States currently offers a 7 percent rate to large, profitable firms. China, meanwhile, has positioned itself as an aggressive player on the global stage, providing an implied subsidy rate of 32 percent, nearly double the European average.

A Chronology of Policy Shifts (2024–2025)

The past year has been characterized by significant legislative movement as nations calibrate their incentives to remain competitive.

- Lithuania: Starting in 2025, Lithuania increased its corporate tax rates, which inadvertently boosted the value of its existing R&D tax deductions. This policy shift lifted the implied subsidy rate for large, profitable firms from 31 percent to 34 percent.

- The Slovak Republic: Similar to Lithuania, the Slovak Republic’s adjustment to its corporate tax framework resulted in a jump in the implied subsidy rate from 28 percent to 33 percent.

- The Netherlands: Unlike the passive increases seen elsewhere, the Dutch government took explicit action by raising tax credit rates for in-scope R&D, moving the implied subsidy rate from 31 percent in 2024 to 35 percent in 2025.

- The United States: After a period of policy uncertainty, the U.S. moved to restore its pre-2022 expensing regime. By eliminating temporary amortization requirements and combining this with existing R&D tax credits, the U.S. more than doubled its implied subsidy rate for large, profitable firms, moving from 3 percent to 7 percent.

Supporting Data: SME vs. Large Firm Dynamics

A critical nuance in R&D policy is the treatment of Small and Medium-sized Enterprises (SMEs) versus large, profitable corporations. Most nations utilize a "one-size-fits-all" approach, offering the same expenditure-based relief regardless of company size. However, there are notable exceptions where governments have sought to foster entrepreneurial ecosystems through preferential treatment.

Germany, Iceland, and the Netherlands have implemented more generous structures for SMEs than for large firms. France also provides enhanced support for SMEs, particularly those in loss-making positions. Conversely, Croatia stands as a rare outlier, offering slightly higher relief to large firms than to SMEs.

The data further highlights the challenges faced by loss-making firms. Because R&D often requires massive upfront capital before profitability is achieved, tax credits that cannot be utilized immediately—or that lack refundability and carryover provisions—become less effective. Consequently, the average implied subsidy rate for loss-making firms is consistently lower than that for profitable firms, creating a potential barrier for startups and innovation-heavy firms that have yet to turn a profit.

Official Perspectives and Economic Implications

The proliferation of R&D tax incentives is not without its critics. While proponents argue that these credits are essential to offset the high costs of innovation, policymakers are increasingly grappling with the "fiscal leakage" associated with these programs.

The Challenge of Targeted Innovation

The fundamental goal of R&D relief is to encourage investment that generates positive spillovers—knowledge, new products, and technologies that benefit the wider economy. However, identifying "genuine" innovation is notoriously difficult. As governments attempt to prevent abuse and ensure that tax dollars are not subsidizing routine business activities, they inevitably increase administrative and compliance costs. Firms must navigate complex reporting requirements, and tax authorities must devote significant resources to auditing and verifying qualified expenditures.

The Case for Neutral Tax Treatment

Many economists argue that the current obsession with R&D-specific tax preferences may be misplaced. Instead of creating convoluted, targeted incentives, policymakers could support innovation more effectively—and at a lower revenue cost—by refining the general tax code.

Key recommendations from policy experts include:

- Neutral Cost Recovery: Allowing firms to fully recover their capital costs in a timely manner.

- Loss Offsets: Implementing flexible regimes that allow firms to offset their operating losses against past or future profits.

By creating a tax environment that is neutral toward investment, governments could reduce the distortionary effects of picking "winners" through R&D credits, while simultaneously lowering the compliance burden on the private sector.

Conclusion: The Road Ahead

As the global competition for technological leadership intensifies, the landscape of R&D tax incentives will continue to evolve. While the data shows a clear trend toward higher subsidy rates in many jurisdictions, the efficacy of these programs remains a subject of intense debate.

For policymakers, the challenge is twofold: maintaining a competitive edge in an era of global capital mobility while ensuring that tax expenditures do not undermine the stability of the national budget. Moving forward, the most successful nations will likely be those that transition away from complex, fragmented R&D incentives and toward broad, neutral tax policies that foster a fertile ground for all forms of investment.

As we look toward the remainder of the decade, the shifting subsidy rates in the U.S., the Netherlands, and across Europe suggest that governments are far from reaching a consensus. Whether the future lies in direct, targeted subsidies or in the broader, neutral treatment of risky capital investment remains the defining question of modern corporate tax policy. For businesses, keeping a close eye on these changing legislative landscapes is no longer just a tax function—it is a strategic necessity.