: A Comprehensive Guide for Borrowers")

In the modern financial landscape, a credit score is more than just a three-digit number; it is a fundamental pillar of economic identity. It dictates the ability to secure housing, the interest rates on essential loans, and even, in some sectors, the viability of employment opportunities. However, for millions of Americans, "credit confidence"—the belief in one’s ability to manage and leverage credit effectively—has been shaken by a series of global and personal economic shocks.

From the lingering effects of the pandemic-era disruptions to the recent pressures of inflation and rising interest rates, the path to financial stability has become increasingly complex. Yet, as experts at Lexington Law and various consumer advocacy groups assert, a credit setback is a temporary state, not a permanent definition of financial worth. Rebuilding that confidence requires a strategic blend of legal rights, behavioral shifts, and disciplined patience.

The Main Facts: The Current State of Consumer Credit

The American credit landscape is currently defined by a paradox of high participation and high pressure. According to recent data from the Federal Reserve, total household debt has reached record highs, with credit card balances and auto loans seeing significant upticks. In this environment, even minor financial missteps can have outsized consequences.

The Prevalence of Reporting Errors

One of the most startling facts in the credit industry is the frequency of inaccuracies. A landmark study by the Federal Trade Commission (FTC) previously found that one in five consumers had an error on at least one of their credit reports. These errors range from "mixed files" (where two people with similar names have their data merged) to "zombie debt" (debts that have passed the statute of limitations but continue to appear). For the consumer, these inaccuracies represent an invisible barrier to rebuilding confidence.

The Psychological Toll of Credit Stress

Financial setbacks—whether caused by medical emergencies, divorce, or job loss—often carry a heavy emotional burden. The concept of "credit confidence" is as much about mental health as it is about math. When individuals feel "stuck" or embarrassed by their scores, they are less likely to engage with their finances, creating a cycle of avoidance that further degrades their credit standing.

Chronology of Recovery: A Step-by-Step Path to Rebuilding

Rebuilding credit is not a sprint; it is a deliberate, phased process. Understanding the timeline of recovery can help consumers manage expectations and maintain motivation.

Phase 1: The Diagnostic Audit

The first step in any recovery journey is a comprehensive assessment. Under the Fair Credit Reporting Act (FCRA), every consumer is entitled to a free credit report from each of the three major bureaus—Experian, Equifax, and TransUnion—every 12 months (though weekly reports have been made available via AnnualCreditReport.com in recent years).

During this phase, consumers must look for:

- Identity Errors: Incorrect names, addresses, or Social Security numbers.

- Account Inaccuracies: Closed accounts marked as open, or vice versa.

- Payment History Discrepancies: Late payments that were actually made on time.

- Unauthorized Inquiries: Hard pulls on credit that the consumer did not initiate.

Phase 2: The Dispute and Correction Cycle

Once errors are identified, the legal process of disputing begins. This involves notifying both the credit bureau and the "furnisher" (the creditor that reported the information). The bureaus generally have 30 to 45 days to investigate and respond. This stage is critical because removing a single significant error can result in a rapid score increase, providing the "small win" necessary to fuel long-term confidence.

Phase 3: The Behavioral Re-Anchoring

After the "cleanup" of the credit report, the focus shifts to daily habits. This phase involves two primary levers:

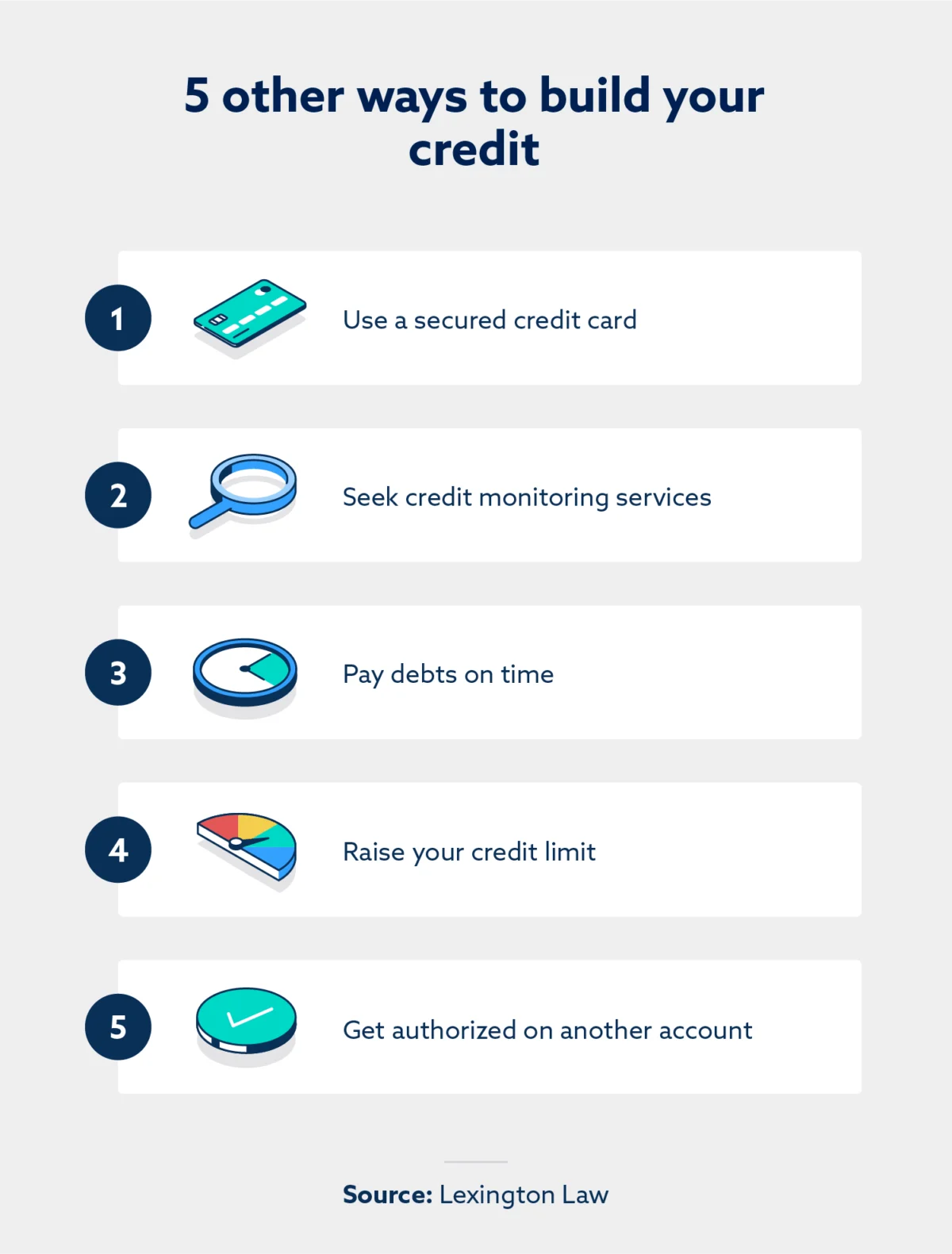

- Payment Consistency: Establishing an unbroken chain of on-time payments.

- Utilization Management: Reducing the "credit utilization ratio"—the amount of debt owed relative to the total credit limit—to below 30%, or ideally, below 10%.

Phase 4: The Seasoning Period

The final phase is the most difficult for many: waiting. Credit scoring models, such as FICO and VantageScore, reward the "age" of accounts and a sustained history of low-risk behavior. While most negative items fall off a report after seven years, their impact begins to diminish significantly after the two-year mark if they are outweighed by new, positive data.

Supporting Data: The Mechanics of the Score

To rebuild credit confidence, one must understand the weight of various factors within the credit scoring algorithms. Knowledge of these data points allows consumers to prioritize their efforts effectively.

The FICO Breakdown

- Payment History (35%): This is the single most influential factor. Even one 30-day late payment can cause a score to drop by 60 to 100 points, depending on the initial score.

- Amounts Owed (30%): This focuses on credit utilization. High balances on revolving credit (credit cards) suggest a high risk of default, even if payments are made on time.

- Length of Credit History (15%): Older accounts are better. Closing an old, unused card can actually hurt a score by shortening the average account age.

- Credit Mix (10%): Lenders like to see a variety of credit types, such as a mortgage, an auto loan, and a credit card.

- New Credit (10%): Opening too many accounts in a short period signals financial distress to lenders.

The Cost of Low Confidence

The data illustrates a stark reality: low credit scores are expensive. For example, on a $300,000 30-year fixed mortgage, a borrower with a score in the 620 range might pay thousands of dollars more per year in interest compared to a borrower with a score of 760. Over the life of the loan, the "cost of bad credit" can exceed $100,000. This data underscores why rebuilding credit is one of the highest-return investments an individual can make.

Official Responses and Legal Frameworks

The process of rebuilding credit is not merely a matter of personal responsibility; it is protected and governed by federal law. Understanding these "official" mechanisms provides consumers with the leverage they need to face large financial institutions.

The Fair Credit Reporting Act (FCRA)

The FCRA is the "Bill of Rights" for consumers regarding their data. It mandates that information in a credit file must be accurate, complete, and verifiable. If a credit bureau cannot verify a disputed item within the legal timeframe, they are required by law to remove it. This legal framework is what allows firms like Lexington Law to advocate for consumers, ensuring that the "truth" of a consumer’s financial history is what is actually being reported.

The Role of Professional Advocacy

While consumers can manage disputes on their own, many turn to professional credit repair organizations. These firms provide a layer of expertise in navigating the complex communication channels of the three major bureaus. Their role is to ensure that disputes are framed correctly under the law and that creditors are held accountable for the data they provide.

As noted by Lexington Law, the goal of professional support is not just to "fix" a score, but to educate the consumer on how to maintain that score. This involves deep dives into the Fair Credit Billing Act (FCBA) and the Fair Debt Collection Practices Act (FDCPA), which protect consumers from unfair billing and predatory collection tactics, respectively.

Implications: The Long-Term Impact of Restored Credit

The implications of rebuilding credit confidence extend far beyond the individual’s bank account. They ripple through the broader economy and the social fabric of communities.

Economic Mobility and Wealth Building

Credit is a primary tool for wealth creation in the United States. Access to low-interest capital allows individuals to purchase homes—the primary source of net worth for most Americans—and start small businesses. By rebuilding credit confidence, individuals move from a defensive financial posture (paying off old mistakes) to an offensive one (investing in the future).

Reducing the "Poverty Premium"

Individuals with low credit scores often fall victim to the "poverty premium"—paying more for basic services. This includes higher insurance premiums, utility deposits, and the need to use predatory "payday loans" due to a lack of traditional bank access. Restoring credit confidence effectively gives the consumer a "raise" by eliminating these unnecessary costs.

A Shift in Financial Mindset

Perhaps the most profound implication is the shift from shame to strategy. When a consumer realizes that credit is a system with rules that can be learned and mastered, the fear of financial setbacks diminishes. This psychological resilience is essential for navigating future economic downturns. It transforms the consumer from a passive participant in the economy into an empowered actor.

The Bottom Line

Rebuilding credit confidence is an act of reclaiming one’s future. It requires a confrontation with the past—reviewing the "black and white" of credit reports—and a commitment to a disciplined future. Whether through self-management or professional assistance, the journey is defined by progress rather than perfection.

As the economic landscape continues to evolve, the ability to manage, repair, and leverage credit will remain one of the most vital life skills of the 21st century. The message for those facing setbacks is clear: your financial story is not a static document; it is a narrative that you have the legal and practical power to rewrite.

Legal Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or credit advice. Use of this information does not create an attorney-client relationship. Credit repair results vary, and no specific outcome can be guaranteed. For specific legal or financial concerns, consumers should consult with a qualified professional.