For the first time in nearly two decades, the skyline of Pittsburgh’s financial district is bracing for a new tenant that represents a rare breed in the modern banking landscape: a de novo community bank. Brian Tabb, a former senior executive at BNY (formerly BNY Mellon), has officially filed applications with federal regulators to establish Sagehaven Bancorp.

The move marks a significant milestone for Pittsburgh, a city that serves as the headquarters for PNC Financial Services and a major hub for BNY, yet has seen its local community banking sector thin out through years of consolidation. Sagehaven’s entry into the market is not merely a business venture; it is a signal of shifting regulatory tides, a bet on the enduring value of localized relationship banking, and a testament to the technological evolution of the financial services industry.

I. Main Facts: The Blueprint for Sagehaven Bancorp

Sagehaven Bancorp is positioned to be a high-touch, technology-forward community bank headquartered in Pittsburgh’s central business district. On Tuesday, the organizing group submitted formal applications for a national bank charter to the Office of the Comptroller of the Currency (OCC) and for federal deposit insurance to the Federal Deposit Insurance Corporation (FDIC).

Target Market and Mission

The proposed institution is not seeking to compete with the retail banking giants for every checking account in the tri-state area. Instead, Sagehaven has a surgical focus:

- Small to Mid-Market Companies: Businesses that often find themselves "too small" for the white-glove service of global investment banks but "too complex" for the automated lending processes of large retail banks.

- High-Net-Worth Individuals: Providing bespoke wealth management and private banking services to the growing professional class in Pittsburgh’s "Eds and Meds" (Education and Healthcare) economy.

- The "Relationship" Gap: Filling the void left by larger institutions that have moved toward centralized, algorithm-driven decision-making.

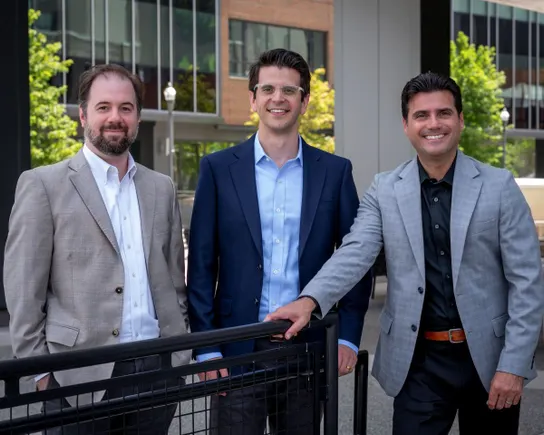

The Leadership Team

The success of a de novo bank—a bank that is newly chartered and not the result of an acquisition—rests almost entirely on the pedigree of its management. Sagehaven is led by a trio of seasoned professionals:

- Brian Tabb (Proposed CEO): Tabb spent four years at BNY, most recently as Senior Vice President of Corporate Treasury. His experience in managing the balance sheet of one of the world’s largest custodial banks provides the foundational expertise required to navigate the complex liquidity and capital requirements of a startup bank.

- Angelo Innamorato (Proposed COO): Bringing a wealth of operational experience from both BNY and Huntington National Bank, Innamorato is tasked with building the bank’s infrastructure from the ground up.

- Jared Leland (Proposed Chief Counsel): A former partner at the law firm Houston Harbaugh, Leland provides the legal and regulatory navigate necessary for an industry that is among the most heavily policed in the United States.

II. Chronology: From Corporate Treasury to Entrepreneurship

The journey toward Sagehaven Bancorp began in the halls of BNY, where Brian Tabb observed the rapid transformation of the banking sector. While the global giants focused on scale and digital ubiquity, Tabb identified a latent demand for a localized institution that could leverage modern technology without the "anchor" of legacy systems.

- March 2024: Brian Tabb departs his role as SVP of Corporate Treasury at BNY. This exit marked the beginning of the formal planning phase for Sagehaven. Tabb cited his time at BNY as "instrumental" in providing the skills necessary to envision a new bank, particularly under the leadership of BNY CEO Robin Vince, who has championed a culture of efficiency and artificial intelligence.

- Spring–Summer 2024: The organizing group is formed. Tabb recruits Innamorato and Leland, securing the operational and legal pillars of the project. During this period, the team finalized their business plan, focusing on a national charter rather than a state charter—a strategic decision based on Pittsburgh’s proximity to Ohio, West Virginia, and New York.

- Late 2024: The group engages in pre-filing discussions with the OCC and FDIC. This is a critical stage where regulators vet the initial proposal to ensure the organizers have sufficient capital and a viable "Path to Profitability."

- Tuesday (Current Week): The formal application is submitted to the OCC and FDIC.

- April 2027: The projected "Go-Live" date. The three-year window between filing and opening accounts for the rigorous regulatory review process, capital raising rounds, and the build-out of the bank’s technological core.

III. Supporting Data: The Regulatory and Economic Context

The filing for Sagehaven comes at a fascinating inflection point for the American banking industry. To understand the significance of this move, one must look at the data surrounding de novo activity and the specific economic landscape of Pittsburgh.

The De Novo Drought and Resurgence

Following the 2008 financial crisis, the creation of new banks slowed to a trickle. High regulatory costs and a low-interest-rate environment made it difficult for new entrants to achieve the "net interest margin" (the difference between interest earned on loans and interest paid on deposits) necessary to survive.

However, the tide is turning. Under Comptroller Jonathan Gould, the OCC has signaled a renewed openness to new charters.

- 2023 Statistics: The OCC received 18 applications for new bank charters in 2023, a number equal to the previous four years combined.

- 2024 Momentum: More than two dozen applications have been filed so far this year.

- The 120-Day Rule: A significant factor in Sagehaven’s timing is the regulators’ commitment to a 120-day window for making preliminary decisions on applications. This transparency allows organizers to plan their capital calls with greater precision.

The Pittsburgh Market

Pittsburgh is often called a "banking hub," but that title is somewhat misleading. While it houses the massive operations of PNC and BNY, the number of independent, locally-focused community banks has dwindled.

- Consolidation: Over the last 20 years, dozens of Western Pennsylvania community banks have been absorbed by regional or national players.

- The Gap: Small businesses (SMEs) in Pittsburgh represent a multi-billion dollar credit market. As larger banks automate their lending, the "soft information"—the local knowledge a banker has about a neighborhood or a business owner—is often lost. Sagehaven aims to reclaim this.

The National Charter Strategy

Tabb’s decision to pursue a national charter over a Pennsylvania state charter is a calculated geographic play. A national charter, regulated by the OCC, provides "preemption" benefits, making it easier to operate across state lines. Given that Pittsburgh is a centerpiece of the tri-state area, many of Sagehaven’s prospective clients have business interests that bleed into Ohio and West Virginia.

IV. Official Responses: Regulatory and Executive Perspectives

The filing has triggered a series of procedural and public responses from the involved parties.

The Organizers’ Stance

In an interview following the filing, Brian Tabb emphasized that Sagehaven is not a "niche" play. While many recent de novo applications have focused on specific sectors like cryptocurrency or fintech-adjacent services, Sagehaven is returning to the roots of the industry.

"We’re starting a community bank," Tabb stated. "We’re not necessarily really going into any of these niche products, like digital assets. But I think the timing of all of this is helpful because the regulators are sticking to a 120-day window."

Tabb also highlighted the personal nature of the project. Though not a Pittsburgh native, he has committed his family’s future to the city. "I really, truly want to immerse myself in this community and make an impact… particularly given that my daughters are going to be raised here."

Federal Regulators

The FDIC has officially confirmed the receipt of Sagehaven’s application for deposit insurance. While the OCC’s spokesperson did not immediately comment on the specific filing, the agency’s broader stance has been one of "cautious encouragement." The OCC is looking for "well-capitalized institutions with experienced management teams" to fill the gaps left by industry consolidation.

Technology as a Catalyst

A recurring theme in the organizers’ rhetoric is the "Mile 20" analogy. Tabb noted that starting a bank in 2025 allows them to bypass the "Mile 2" struggles of legacy banks—meaning they don’t have to spend millions of dollars maintaining 40-year-old mainframe systems. By starting with a cloud-native tech stack and integrated AI from day one, Sagehaven expects to operate with a significantly lower efficiency ratio than its older competitors.

V. Implications: What Sagehaven Means for the Future of Banking

The emergence of Sagehaven Bancorp carries several long-term implications for the financial sector and the Pittsburgh region.

1. The "Post-Legacy" Advantage

Sagehaven represents a new category of "Neo-Community Banks." Unlike "Neobanks" (which are often just tech companies with a banking partner), Sagehaven will be a fully chartered, regulated bank. However, by being born in the age of AI, it can offer the digital seamlessness of a fintech with the stability and regulatory oversight of a traditional bank. This could force existing regional banks in the area to accelerate their own digital transformations.

2. Economic Development in the Rust Belt

Pittsburgh’s transition from a manufacturing center to a tech and healthcare hub requires a sophisticated financial ecosystem. Small and mid-market companies in these sectors often require complex lending structures—such as asset-based lending for tech hardware or specialized credit lines for medical practices. A local bank with the authority of a national charter and the agility of a startup could become a primary engine for local business growth.

3. A Litmus Test for the OCC

The Sagehaven application will be a closely watched test case for the OCC’s efficiency. If the "120-day window" holds true and the bank moves toward its 2027 opening without significant regulatory friction, it may encourage other former "Big Bank" executives to leave their corporate roles and start their own local institutions. This could lead to a broader "de-concentration" of the American banking system, which many economists argue would improve financial stability.

4. The Human Element

Ultimately, Sagehaven is a bet on the idea that in an era of ChatGPT and automated teller machines, people still want to talk to a banker who knows their name and their business. By focusing on the Pittsburgh central business district, Sagehaven is positioning itself at the heart of the city’s identity.

As the application moves through the federal pipeline, the banking industry will be watching to see if Brian Tabb and his team can successfully bridge the gap between the storied history of Pittsburgh finance and the high-tech future of global banking. If successful, Sagehaven Bancorp won’t just be the first de novo bank in Pittsburgh in 20 years—it could be the blueprint for the next generation of American community banking.