For millions of Americans, the pursuit of a higher education is a path toward career advancement and increased lifetime earnings. However, the academic journey is rarely linear. Unexpected life events—ranging from financial hardship and family obligations to health challenges—often force students to pause or abandon their studies before receiving a diploma. According to data from the Education Data Initiative, approximately 39% of first-time, bachelor’s degree-seeking students fail to complete their programs within an eight-year window.

For these individuals, the financial burden of student loans remains a persistent reality. While the degree may be unfinished, the debt is not. Many borrowers in this position mistakenly believe they are trapped with their existing loan terms, unaware that refinancing remains a viable, albeit more challenging, option.

The Financial Landscape: Can You Refinance Without a Degree?

The short answer is yes. While the lending market is significantly more restrictive for non-graduates than for alumni, it is not closed. Refinancing involves replacing one or more existing student loans—either federal or private—with a new, single private loan. The objective is typically to secure a lower interest rate, reduce the monthly payment, or simplify the repayment process by consolidating multiple servicers into one.

However, the "degree requirement" is a common hurdle. Many traditional lenders mandate proof of graduation as a risk-mitigation strategy. They view degree completion as a proxy for long-term career stability and higher earning potential. When that marker is missing, lenders must pivot to alternative metrics, such as credit history, debt-to-income ratios, and employment stability.

Chronology of the Lending Shift

Historically, student loan refinancing was an exclusive club for high-earning graduates. As the student debt crisis intensified over the last decade, the market evolved.

- Pre-2015: Refinancing was almost exclusively reserved for graduates of four-year institutions.

- 2015–2020: As competition among private lenders increased, firms began looking for "underserved" markets. They realized that many non-graduates were still employed in high-paying fields (like trade industries or tech) and possessed strong credit.

- 2020–Present: In the wake of pandemic-era economic volatility, lenders have refined their underwriting algorithms. Today, the focus has shifted toward "repayment behavior." Lenders are now more likely to approve non-graduates who can demonstrate a consistent history of on-time payments, effectively proving their reliability despite the absence of a credential.

Supporting Data and Lender Options

For borrowers without a degree, the "big banks" may turn them away, but specialized private lenders have stepped in to fill the gap. Here are the primary entities currently offering options for non-graduates:

1. Earnest

Earnest is widely recognized for its flexible underwriting. They do not have a blanket "no degree" policy, provided the borrower meets specific criteria. Applicants generally need a strong credit profile and at least six years since their last enrollment. Furthermore, the original loans must have been issued for a Title IV-accredited institution.

2. Citizens Bank

Citizens represents the "traditional" banking approach. Unlike lenders that focus purely on credit, Citizens looks for a track record. Their primary requirement for non-graduates is proof of at least 12 consecutive, on-time monthly payments made after leaving school. This serves as a "probationary period" that validates the borrower’s intent and ability to pay.

3. Advantage Education Loan

This lender provides a pathway for those with lower balances or those who may need a cosigner. With loan amounts starting at $7,500, they offer terms between 10 and 20 years, making them a solid choice for those looking to stretch out payments to lower the monthly burden.

4. EDvestinU

Focusing on loans used for Title IV, degree-granting institutions, EDvestinU allows for significant flexibility. They offer refinancing for balances up to $200,000. Crucially, they are highly receptive to applications involving a creditworthy cosigner, which can significantly lower the interest rate for the primary borrower.

5. MEFA (Massachusetts Educational Financing Authority)

MEFA requires at least $10,000 in existing debt and a proven history of on-time payments. They are particularly strict about the "current" financial picture, often requiring applicants to be U.S. citizens or permanent residents with a stable, documented income.

6. RISLA (Rhode Island Student Loan Authority)

Despite the name, RISLA is available to borrowers nationwide. They are known for competitive fixed rates and offer loan amounts up to $250,000. Their willingness to work with non-graduates has made them a popular choice for borrowers looking to exit high-interest federal or private debt.

Official Perspectives and Risk Implications

Financial experts consistently urge caution when considering refinancing. The decision is not merely about the interest rate; it is about the "lost benefits."

The Federal Trade-Off

When you refinance federal student loans with a private lender, you effectively convert them into private debt. This results in the permanent loss of federal protections, including:

- Income-Driven Repayment (IDR) Plans: These plans cap your monthly payments based on your income.

- Public Service Loan Forgiveness (PSLF): If you work for a non-profit or government entity, your debt could be forgiven after 120 qualifying payments.

- Deferment and Forbearance: Federal loans offer broad protections during unemployment or economic hardship, which private lenders are not legally required to match.

The Mathematics of Refinancing

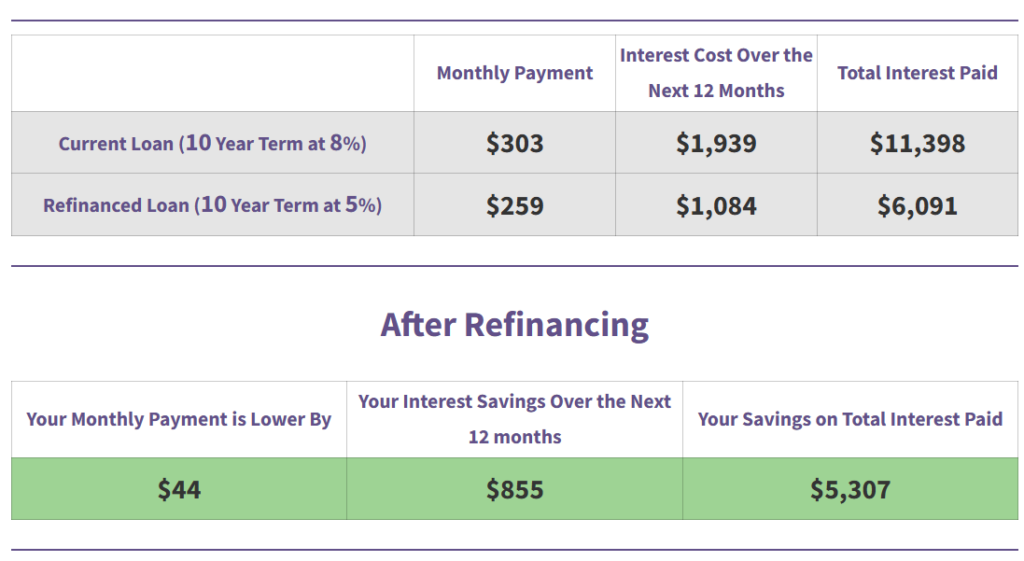

The primary argument for refinancing is simple arithmetic. If you hold a $25,000 loan at an 8% interest rate, you are paying significantly more in interest over time than you would at a 4.5% rate. As illustrated by the Student Loan Planner calculator, the difference in monthly payments can be substantial—often hundreds of dollars annually—which can be redirected toward savings, retirement, or paying down the principal faster.

Strategic Recommendations for Borrowers

If you are a non-graduate looking to improve your financial standing, follow this roadmap:

- Check Your Credit: Before applying, pull your credit report. If your score is below 650, you are unlikely to qualify for the best rates. Focus on paying down high-interest credit card debt first to boost your score.

- Document Your History: Prepare a spreadsheet showing your last 12–24 months of on-time payments. This is your strongest evidence of "repayment reliability."

- Consider a Cosigner: If your income is modest or your credit is thin, a parent or spouse with a strong credit history can serve as a catalyst for approval. Look for lenders that offer a "cosigner release" program, which allows the cosigner to be removed once you have hit a certain number of successful, on-time payments.

- Explore Alternatives: If your loans are federal, investigate IDR plans or the new Repayment Assistance Plan (RAP) before jumping to private refinancing. You may find that lowering your payment via federal programs is safer than moving the debt to a private lender.

- Calculate the Long-Term Impact: Use a dedicated refinance calculator to determine your "break-even" point. Ensure that the interest savings outweigh the loss of potential federal benefits.

Conclusion

The absence of a degree does not mean you have to be saddled with predatory interest rates or unsustainable debt. By understanding the specific requirements of lenders like Earnest, Citizens, and RISLA, and by meticulously preparing your financial profile, you can navigate the refinancing process effectively.

However, the path requires diligence. Always prioritize your long-term financial security by weighing the immediate relief of a lower monthly payment against the long-term security provided by federal protections. If the complexity of these options feels overwhelming, professional consultation—through services like Student Loan Planner—can provide a customized roadmap, ensuring that your path to debt management is as efficient and secure as possible.