The global banking sector is currently navigating its most significant inflection point since the introduction of online banking in the late 1990s. As legacy institutions grapple with the weight of technical debt and the rapid ascent of agile fintech competitors, the industry is witnessing a "Great Decoupling." Customers are no longer tethered to their local branches by proximity or tradition; instead, they are migrating toward platforms that offer the most seamless, personalized, and real-time experiences.

According to a comprehensive strategic guide released by Kyndryl, the world’s largest IT infrastructure services provider, the window for incremental change has closed. To remain competitive, banking leaders must move beyond tactical upgrades and embrace a foundational overhaul of their technological and cultural DNA. The following report synthesizes the core findings of Kyndryl’s research, offering a roadmap for the future of finance.

Main Facts: The Four Pillars of Modern Banking Strategy

The modernization of banking is no longer a matter of simply launching a mobile app. It requires a holistic rethink of how value is created and delivered. Kyndryl identifies four critical recommendations that serve as the pillars of a future-ready financial institution.

1. The Shift to Composability and Long-Term Transformation

Traditional banking systems were built as "monoliths"—large, interconnected software structures where changing one part often risked breaking the whole. Kyndryl argues for a shift toward composability. This architectural philosophy treats banking functions as modular "building blocks" (APIs and microservices) that can be swapped, upgraded, or scaled independently.

This approach is essential for "embedded finance," where banking services are integrated directly into non-financial platforms (such as a retail checkout or a real estate app). By focusing on open banking capabilities, institutions can transition from being mere "vaults" to becoming "orchestrators" of a wider financial ecosystem.

2. Holistic Data Observability

In the modern tech stack, "monitoring" is no longer sufficient. Banks must embrace observability. While monitoring tells you that something is wrong, observability tells you why by providing context across the entire infrastructure—from the hardware chips to the software stack.

The challenge lies in the complexity of hybrid environments. Most banks operate on a mix of on-premises mainframes and multiple public clouds. Kyndryl’s research highlights a massive gap here: while 92% of senior leaders recognize the need for a single dashboard to monitor these environments, 85% find it nearly impossible to implement due to data silos.

3. Cultural Governance and the Talent Pipeline

Technology is only half the battle. Kyndryl’s report emphasizes that the "human element" is often the primary bottleneck. Two-thirds of banking CEOs express concern that their IT systems are nearing the end of their life cycles, but the real crisis is the skills gap. Modernizing these systems requires expertise in Generative AI, cybersecurity, and cloud-native engineering—skills that are in high demand and short supply.

4. Hyper-Personalization and Real-Time Connectivity

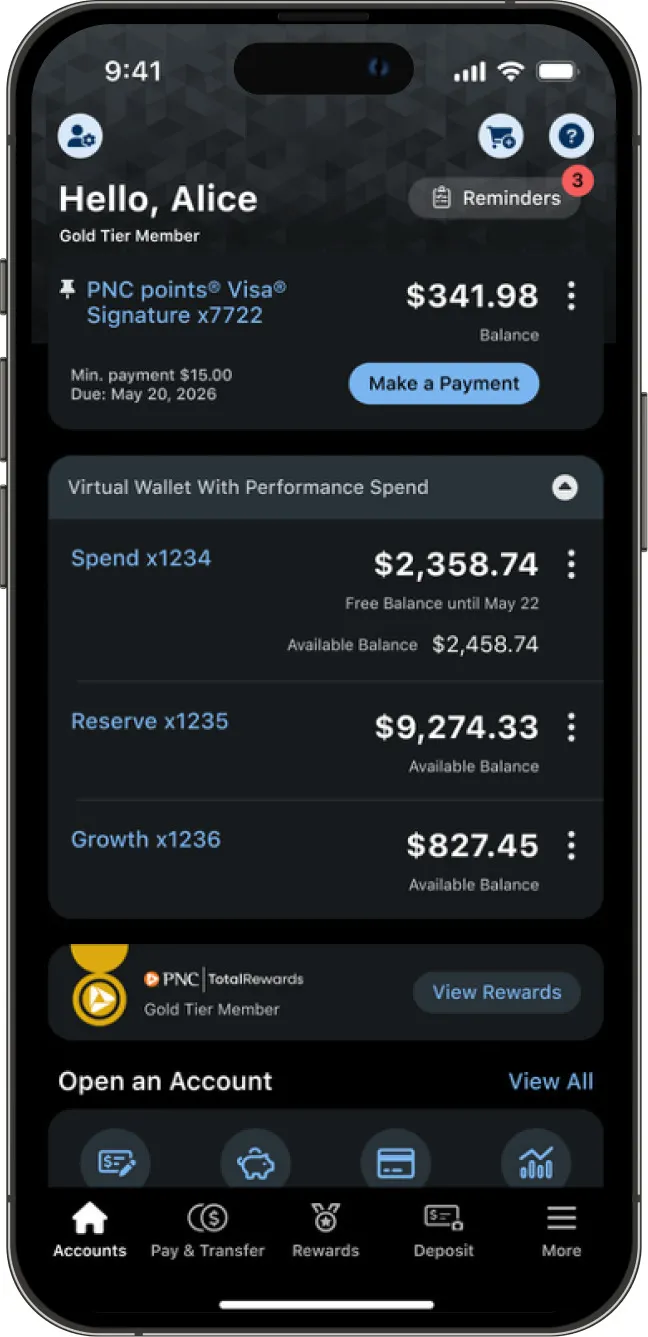

The expectation of the modern consumer—particularly Millennials and Gen Z—is a "Segment of One" experience. This means the bank anticipates needs rather than reacting to them. This is achieved through real-time data processing and AI-driven insights, moving away from interest-rate competition toward value-added, fee-based services.

Chronology: From "Fortress Banking" to "Agile Ecosystems"

To understand the urgency of Kyndryl’s recommendations, one must look at the timeline of the industry’s digital evolution:

- 2010–2015: The Mobile First Era. Banks focused on migrating web portal features to smartphone apps. Success was measured by the number of logins and the ability to perform basic transactions like mobile check deposits.

- 2016–2020: The Rise of the Neobanks. Digital-only players like Chime, Revolut, and Monzo began eating market share. They didn’t just offer an app; they offered a new user experience (UX) characterized by instant notifications, fee transparency, and aesthetic appeal.

- 2021–2023: The Hybrid Cloud and Data Explosion. Incumbent banks began moving massive workloads to the cloud. However, this created "fragmented visibility," where data became trapped in different environments, leading to outages and security vulnerabilities.

- 2024 and Beyond: The AI and Open Banking Frontier. The current era is defined by the integration of Generative AI and the regulatory push for Open Banking. Customers now expect their bank to act as a financial "copilot," providing proactive advice rather than just storing funds.

Supporting Data: The High Cost of Stagnation

The data supporting a radical shift in strategy is stark. Kyndryl points to several key metrics that indicate a brewing crisis for traditionalists:

- Customer Volatility: Research from RFI Global indicates that 1 in 4 U.S. households are currently considering switching their bank or investment provider. This represents a 10-year high in consumer "promiscuity" in the financial sector.

- The Generational Divide: A J.D. Power survey found that direct (digital-only) banks are significantly outperforming traditional regional and national banks in customer satisfaction. This gap is most pronounced among younger demographics who prioritize "support during challenging times" via digital channels over physical branch access.

- The Implementation Gap: While 92% of leaders want unified operational monitoring, the 85% failure or difficulty rate in achieving it suggests that banks are struggling with the "spaghetti code" of their legacy systems.

- CEO Anxiety: Nearly 66% of banking CEOs admit their IT systems are outdated, creating a direct link between aging hardware and increased cybersecurity risks.

Official Responses and Industry Case Studies

Kyndryl’s recommendations are not merely theoretical; they are reflected in the recent actions of major financial players.

The Case of Citi: AI as a Service Tool

Citi recently earned a Pega Innovation award for its "CitiService Agent Assist" solution. Initially launched as a Generative AI pilot, the tool provides customer service agents with real-time transcripts, procedural information, and automated call summaries. By empowering the human agent with AI, Citi has improved customer outcomes and reduced the time spent on administrative tasks. This aligns with Kyndryl’s Recommendation #2 regarding actionable insights through AI.

The Case of Portal: The AI Copilot

In 2024, the fintech infrastructure provider Portal won the "Best of AI in Finance" at the Cloud Awards. Their AI-powered investing copilot, RAFA, connects seamlessly with traditional custodians like Fidelity and Schwab. RAFA provides individual investors with continuous market analysis and personalized portfolio management—features previously reserved for high-net-worth individuals with private wealth managers. This illustrates the "open connectivity" mentioned in Kyndryl’s Recommendation #4.

Kyndryl’s Strategic Stance

"Every banking leader is unique," Kyndryl’s report states. "But there are several core principles leaders around the world should consider to stay competitive." The company emphasizes that while "cash is no longer king," context is. By understanding the context of a customer’s life through data, banks can move from being a commodity to being an essential partner.

Implications: The Future of the Banking Business Model

The shift toward the strategies outlined by Kyndryl will have profound implications for the industry’s bottom line and the broader economy.

1. Revenue Model Stability

Traditionally, banks have relied on the "Net Interest Margin"—the difference between the interest they pay on deposits and the interest they earn on loans. This model is volatile and subject to central bank fluctuations. Kyndryl notes that personalized, AI-driven solutions allow banks to move toward fee-based revenue models. These are more stable, predictable, and less dependent on the interest rate environment.

2. The Rise of Global Capability Centers (GCCs)

As banks struggle to find talent, the "outsourcing" model is evolving. Banks are now establishing Global Capability Centers. Unlike the call centers of the past, these are sophisticated engineering hubs located in talent-rich regions (such as India, Poland, or Mexico) designed to "future-proof" skill sets in AI and cybersecurity.

3. The End of "Customer Obedience"

For decades, banks could rely on "customer obedience"—the idea that a customer would stay with a bank because it was too difficult to move. With the advent of Open Banking and automated account switching, that era is over. CIO teams must now be "customer obsessed," focusing on the user experience (UX) as much as the financial products themselves.

4. Operational Resilience

By adopting observability and composability, banks can significantly reduce the risk of systemic failures. In an era where a 15-minute mobile app outage can become a national news story and a PR disaster, the ability to "spot issues and optimize performance" in real-time is a matter of institutional survival.

Conclusion

The Kyndryl Strategic Guide serves as a stark reminder that in the "new world of finance," agility is the only true currency. Banks that continue to view IT as a back-office cost center rather than a front-line growth engine will likely find themselves among the 25% of institutions that customers are looking to leave. Conversely, those that embrace the "chip-to-stack" observability, cultural transformation, and modular architecture will be well-positioned to lead the next era of global finance.