The residential real estate market in 2026 continues to navigate a complex landscape defined by persistent economic headwinds and geopolitical uncertainty. According to the latest BiggerPockets Pulse survey for the third quarter of 2026, the sentiment of the nation’s largest bloc of retail real estate investors is one of tempered resilience. While investors remain committed to growing their portfolios, a clear trend of declining confidence has emerged as the year has progressed.

Executive Summary: A Steady Downward Trend in Sentiment

The "Pulse Index," a proprietary metric used by BiggerPockets to gauge investor sentiment, provides a stark visualization of the current climate. In the first quarter of 2026, the Index stood at a robust 108 points. By the second quarter, it had retracted to 102, and as of Q3, it has settled at 96 points.

While a score of 96 still sits within the "neutral" territory, the consistent downward trajectory suggests that the optimism characterizing the early months of the year has been replaced by a "wait-and-see" pragmatism. This shift is primarily driven by the increasing difficulty of sourcing viable deals, the rising cost of capital, and the persistent erosion of cash flow due to inflating property-level expenses, such as insurance premiums and property tax hikes.

Chronology of Market Sentiment: From Q1 to Q3 2026

To understand the current state of the market, one must look at the progression of investor expectations over the last nine months.

The Q1 Outlook: Hopes for a Rebound

At the start of the year, investors were broadly optimistic. Many entered the market anticipating that the Federal Reserve would soon pivot, leading to lower interest rates and a subsequent boom in transaction volume. Mortgage rate expectations were anchored in the 5.5% to 5.99% range, and a significant portion of the investor base was positioning itself to capitalize on an expected rebound.

The Q2 Transition: The "About the Same" Plateau

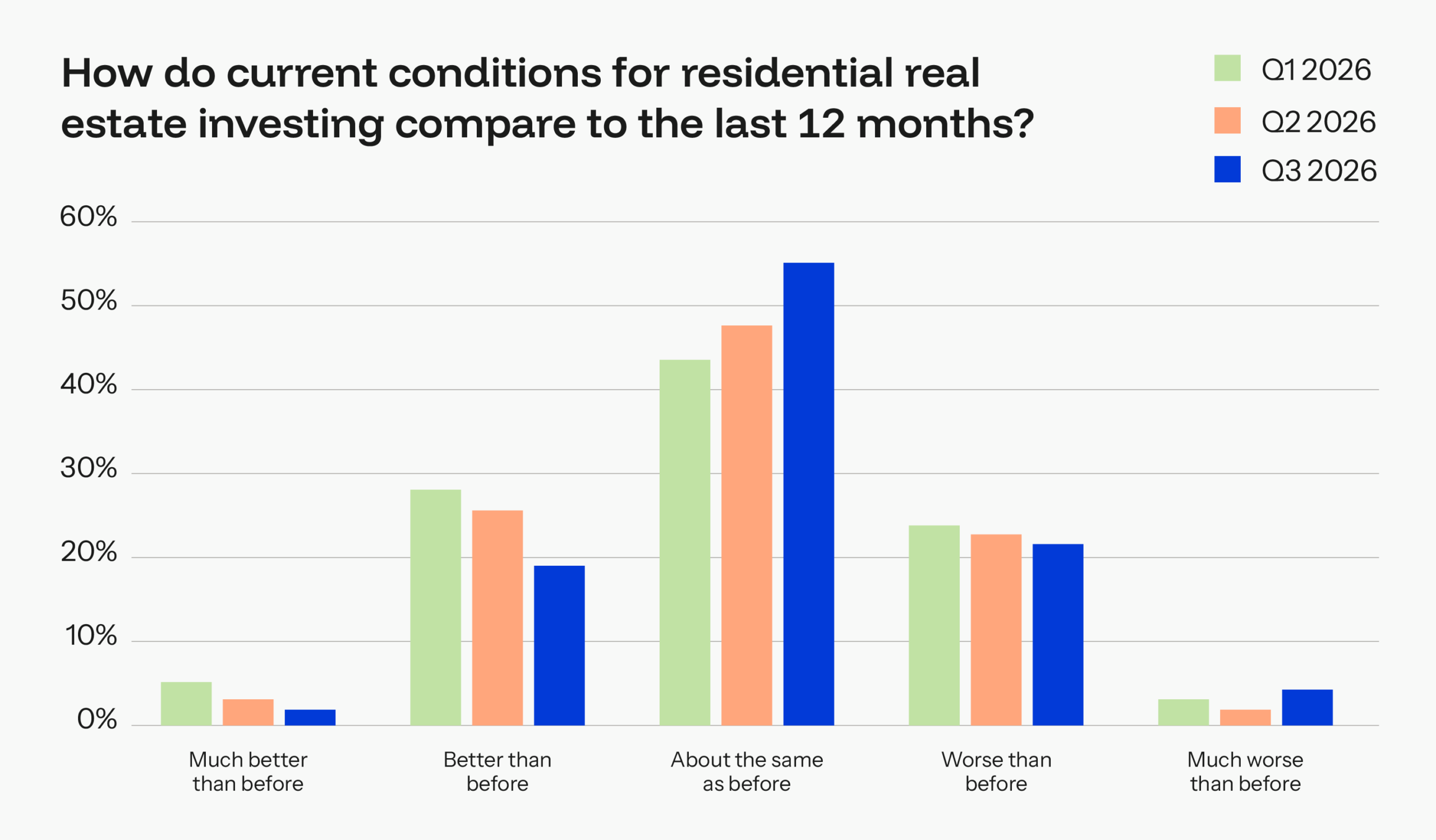

By the second quarter, the anticipated rate relief failed to materialize. The sentiment shifted as investors began to accept that the "high-for-longer" interest rate environment was the new baseline. During this period, the "about the same" sentiment gained ground, rising from 43.5% to 47.5%.

The Q3 Reality: Bracing for Stability

In the current quarter, the narrative has solidified into a "flattening of expectations." A full 55% of respondents now believe market conditions are identical to those of the previous 12 months. The anticipation of a significant improvement in conditions has plummeted to just 1.5%. Investors are no longer betting on a quick recovery; they are adjusting their business models to survive and thrive in a static, high-cost environment.

Supporting Data: Behavior and Strategic Shifts

Despite the cooling sentiment, the BiggerPockets community continues to exhibit high levels of activity. The data suggests that investors are not retreating; they are simply changing their tactics.

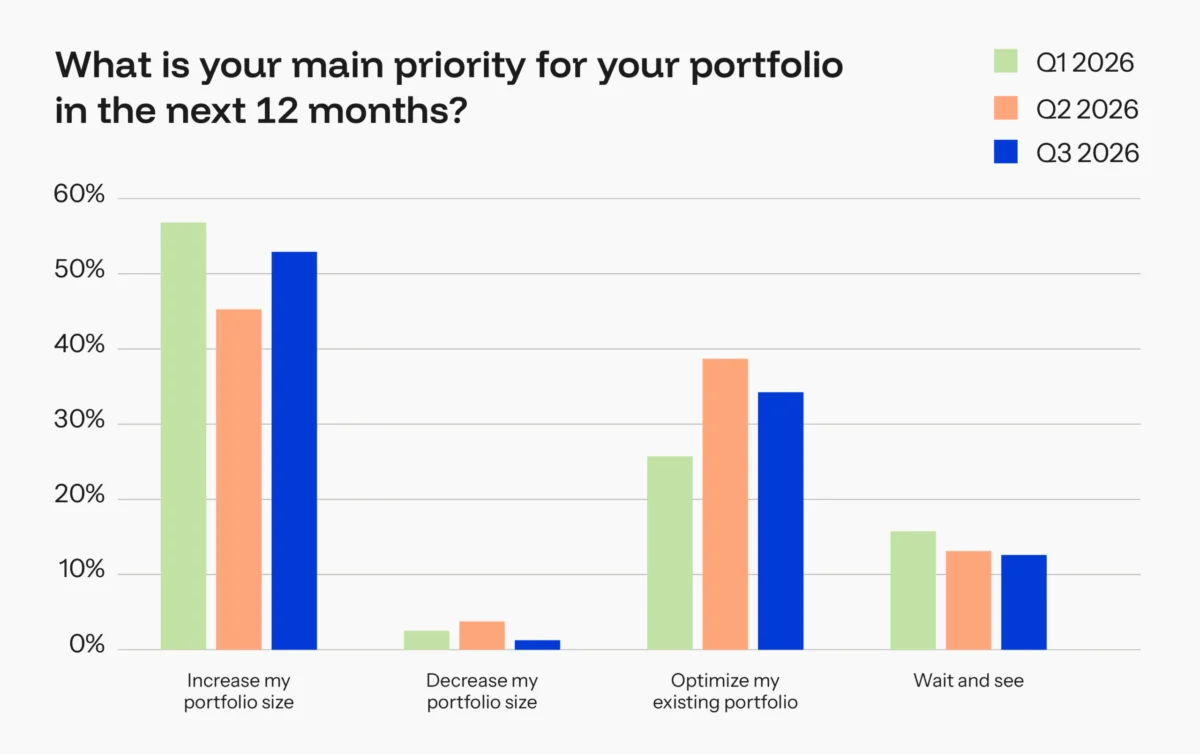

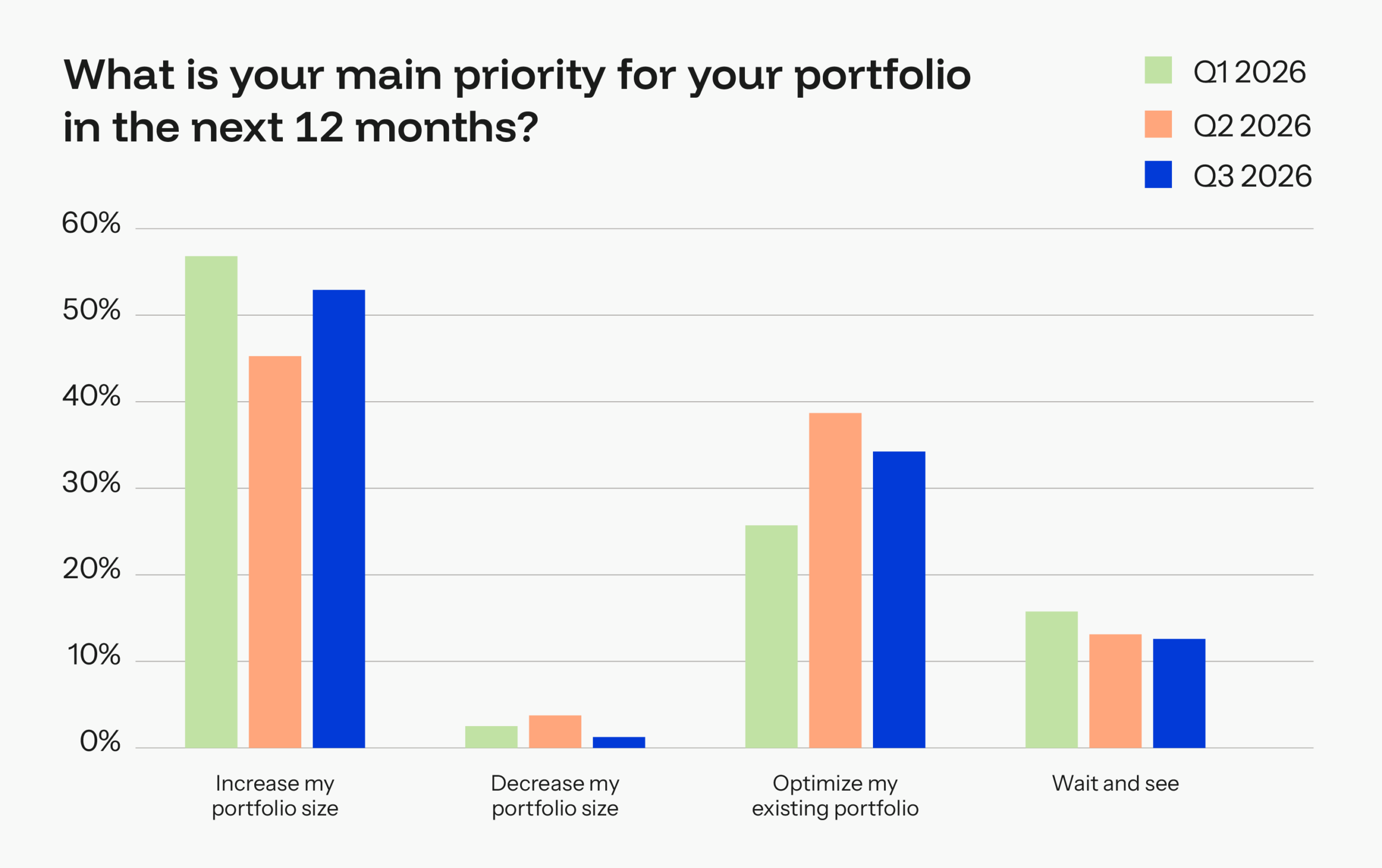

Portfolio Expansion vs. Optimization

Surprisingly, the desire for growth remains the dominant strategy. 53% of investors identified "increasing their portfolio size" as their primary goal for the next 12 months—a rebound from 45% in Q2. This indicates that while the market is difficult, the appetite for acquiring assets remains high among seasoned investors who have identified specific, localized opportunities.

Strategy Preferences: The Flight to Quality

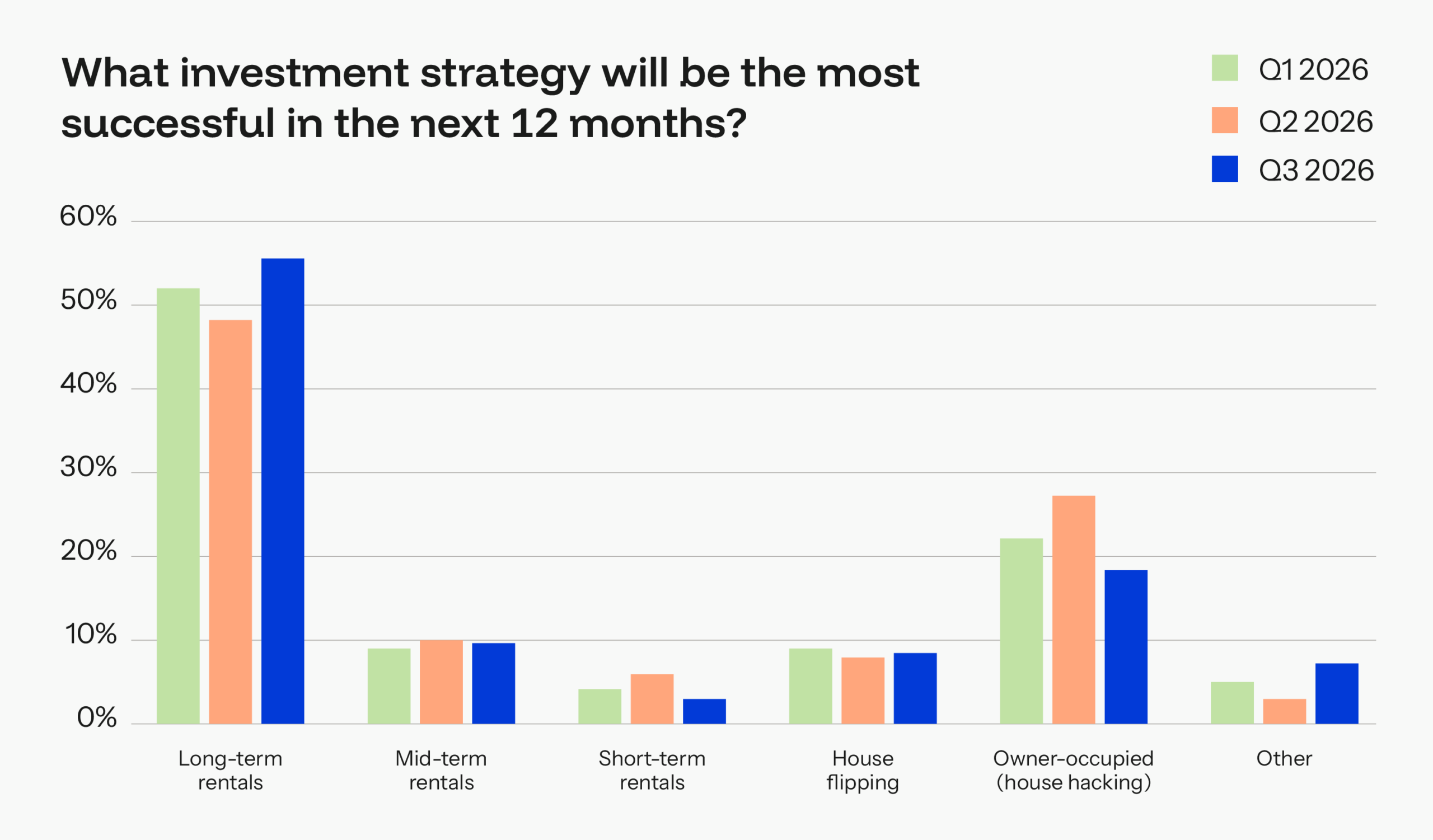

When faced with uncertainty, investors have retreated to the most tried-and-true model: the long-term rental. 55% of respondents believe that long-term rentals will be the most successful strategy over the next year.

The decline of interest in short-term rentals (dropping to 3%) highlights a pivot away from volatility and toward the stability of long-term lease structures. House hacking remains a strong secondary strategy, particularly for those looking to offset their own living expenses while building equity.

The Triple Threat: Primary Challenges Facing Investors

The survey identifies three major obstacles currently preventing deal closure:

- The Deal Drought: Nearly 30% of investors cite the "difficulty of finding good deals" as their primary challenge. This suggests that the bid-ask spread between sellers (who are holding out for peak prices) and buyers (who need to account for higher financing costs) remains wide.

- Rising Operational Expenses: 25% of respondents noted that insurance, taxes, and maintenance are eroding their margins. In many markets, the surge in property insurance costs—driven by climate-related risks—has effectively neutralized the cash flow gains from rising rents.

- Capital Constraints: Access to capital remains a significant friction point, with 25% of investors struggling to secure financing for new acquisitions.

Interestingly, while high mortgage rates were the dominant complaint in previous years, they have faded to 13% of investor concerns. This is not because rates have dropped, but because investors have effectively "priced them in" to their underwriting models.

Regional Focus: The Midwest Advantage

Geographically, the Midwest continues to dominate as the preferred investment destination, with 45% of investors naming it the region with the best conditions. This preference is rooted in the region’s relative affordability and better cap rates compared to the overheated markets of the Sun Belt or the coastal cities.

Implications for the Future: Inflation, Geopolitics, and AI

Looking ahead, the market is grappling with broader macro-economic factors that extend beyond the housing sector.

The Fed and the "Warsh" Factor

When asked about the potential leadership of Kevin Warsh at the Federal Reserve, the majority of investors (67%) remain neutral. This ambivalence suggests that investors are increasingly focused on localized deal metrics rather than attempting to time the Fed’s interest rate policy. It is a sign of market maturity—acknowledging that monetary policy is largely outside of their control.

Geopolitical Stability and Inflation

The war in Iran, which caused significant alarm in the second quarter, has been largely "priced in" by investors. A plurality (47%) now views the conflict as having a neutral impact on their real estate operations in the short term.

However, inflation continues to act as a drag. 43% of investors indicated that inflation makes them less likely to invest in the coming months. The persistent increase in the cost of goods and services is forcing a more conservative approach to capital allocation.

The AI Wildcard

Perhaps the most interesting data point concerns AI and job displacement. While 49.5% of investors expect a neutral impact, a growing number are beginning to view AI as a potential catalyst for housing demand. As the labor market shifts due to automation, the geographic needs of workers may change, potentially favoring smaller, more affordable markets—a trend that could provide a tailwind for the rental sector in the years to come.

Conclusion: The Professionalization of the Investor

The Q3 2026 BiggerPockets Pulse survey paints a picture of an investor base that is maturing rapidly. The era of easy growth, fueled by historically low interest rates and rapid appreciation, has ended. In its place is a professionalized, cautious, and highly selective market.

Investors are no longer waiting for a "return to normal." They are building businesses that can withstand 6% interest rates, elevated insurance premiums, and the ongoing challenges of inventory shortages. By leaning into long-term rental models and focusing on affordability in regions like the Midwest, the modern investor is proving that resilience is not just about surviving a difficult market—it is about finding the margins where others see only obstacles.

As we look toward the end of 2026, the data suggests that those who succeed will be the ones who focus on what they can control: strict underwriting, operational efficiency, and a long-term commitment to the fundamentals of housing.