")

In the modern global economy, a credit score is more than just a three-digit number; it is a financial passport. As we move through 2026, the landscape of consumer lending has shifted toward higher scrutiny and more sophisticated algorithmic modeling. Whether a consumer is looking to secure a mortgage, lease a vehicle, or simply obtain a credit card with a competitive interest rate, their FICO® and VantageScore® profiles—ranging from 300 to 850—remain the primary gatekeepers of economic mobility.

The following report provides a comprehensive analysis of the most effective strategies for building credit in the current market, the evolution of credit reporting, and the broader implications of credit health on personal and national economic stability.

I. Main Facts: The 15 Essential Strategies for 2026

Building credit in 2026 requires a multi-faceted approach that combines traditional debt management with new, technology-driven tools. Experts at firms like Lexington Law emphasize that while there is no "magic bullet" for an instant 800 score, the following 15 strategies are the most effective levers for improvement.

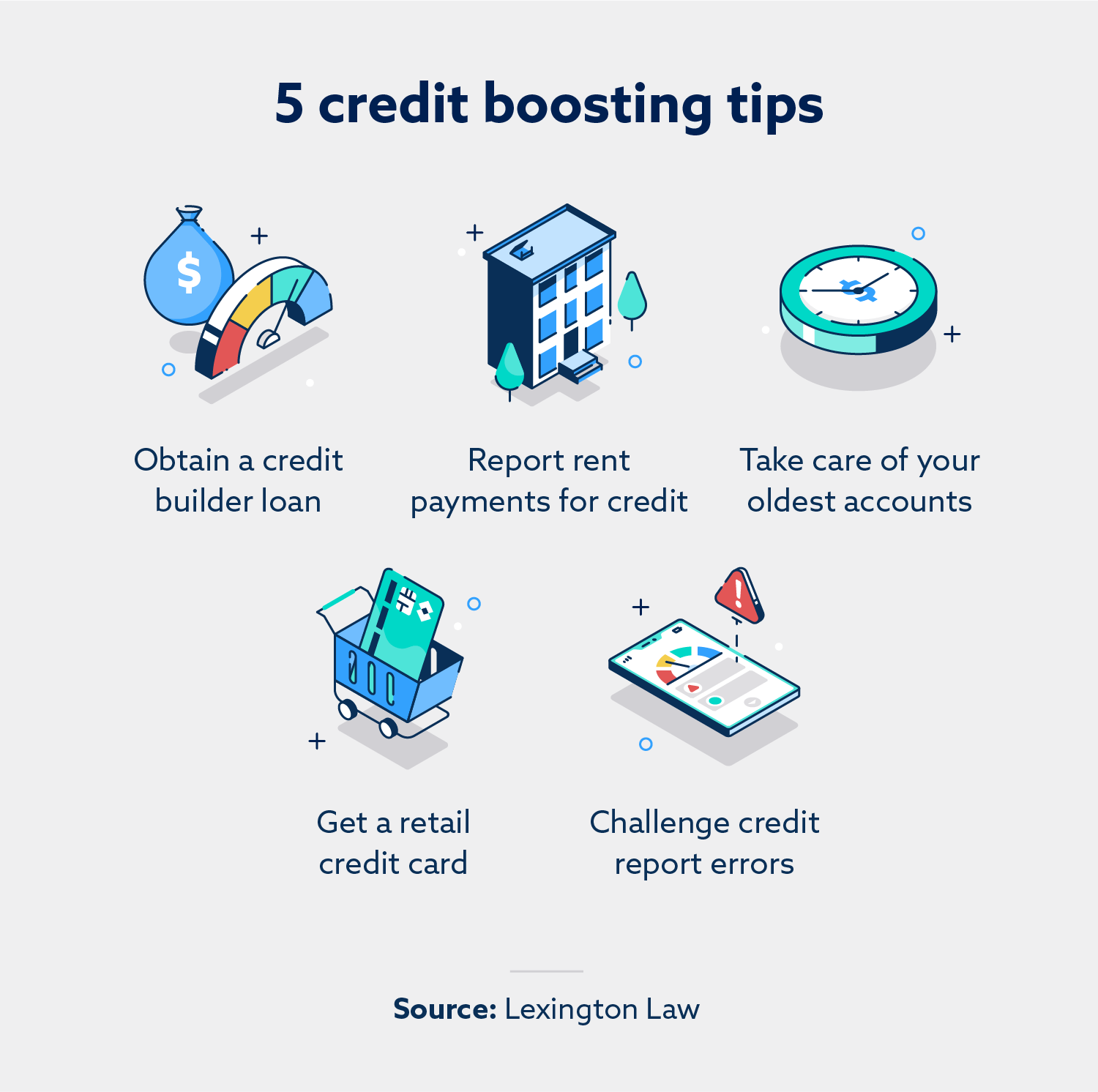

1. The Rise of Credit Builder Loans

Unlike traditional loans where you receive the cash upfront, credit builder loans hold the borrowed amount in a secured savings account while you make monthly payments. Once the loan is paid off, the funds are released to you. This "forced savings" mechanism is reported as a positive installment loan, significantly boosting the "Credit Mix" and "Payment History" categories of a score.

2. Institutionalizing Rent Payments

Historically, rent was the largest monthly expense that didn’t help a credit score. In 2026, rent-reporting services have become mainstream. By using third-party platforms to transmit data to Equifax®, Experian®, and TransUnion®, renters can build a "thin file" into a robust history without taking on new debt.

3. The Preservation of Account Longevity

Length of credit history accounts for approximately 15% of a FICO® score. Journalistic analysis of consumer trends shows that "churning" cards—closing old ones to open new ones for rewards—often backfires. Maintaining the oldest account, even if it is rarely used, preserves the average age of accounts (AAoA), a critical metric for stability.

4. Strategic Use of Retail Credit Cards

While often criticized for high interest rates, retail cards usually have lower barriers to entry. For consumers with "fair" credit, using a store card for essential purchases and paying it off immediately can demonstrate reliability to the bureaus.

5. Rigorous Error Challenging

The Consumer Financial Protection Bureau (CFPB) has noted that a significant percentage of credit reports contain errors. These can range from misspelled names to incorrectly reported late payments or "zombie" debts that should have aged off. Engaging professional services to challenge these inaccuracies remains a cornerstone of credit maintenance.

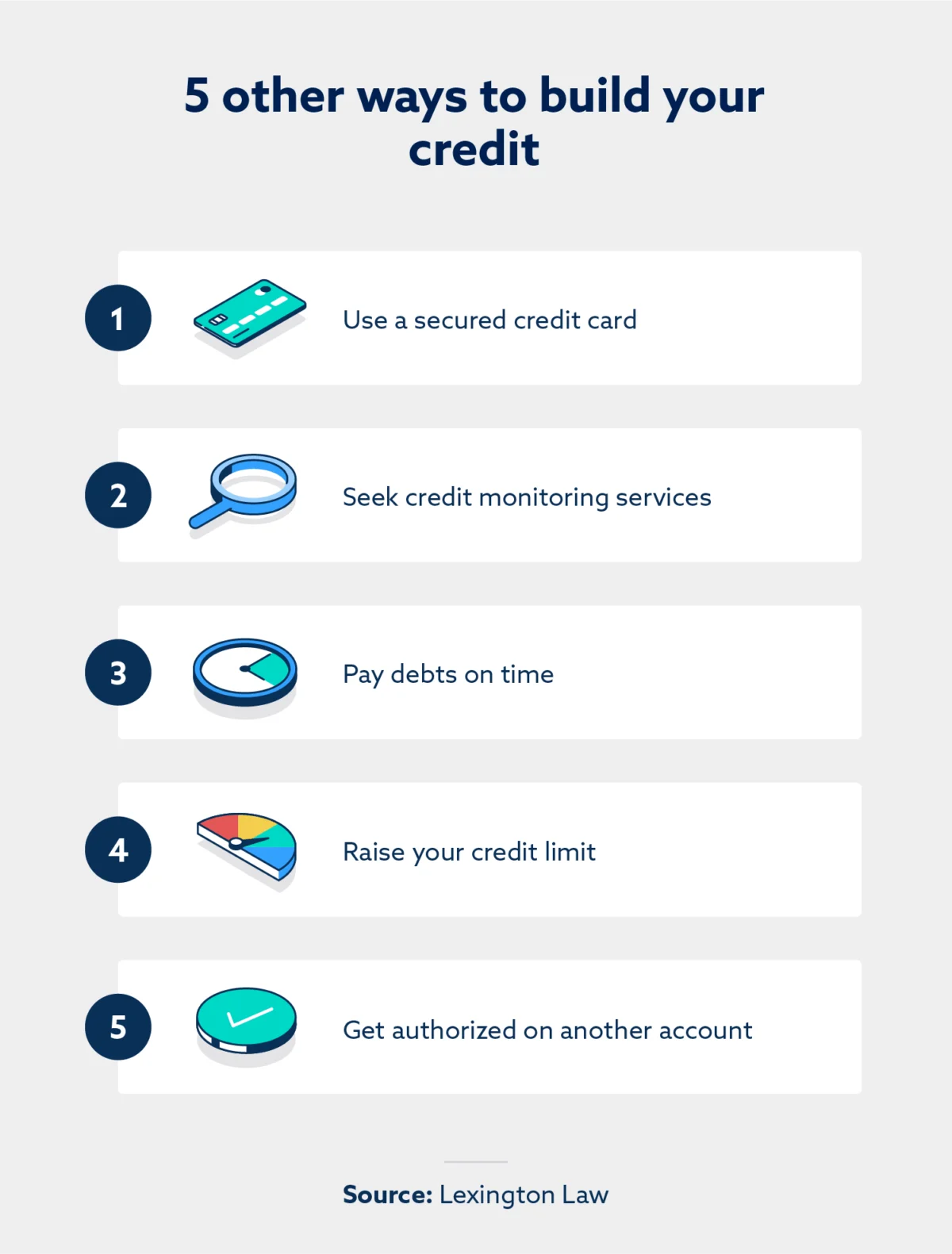

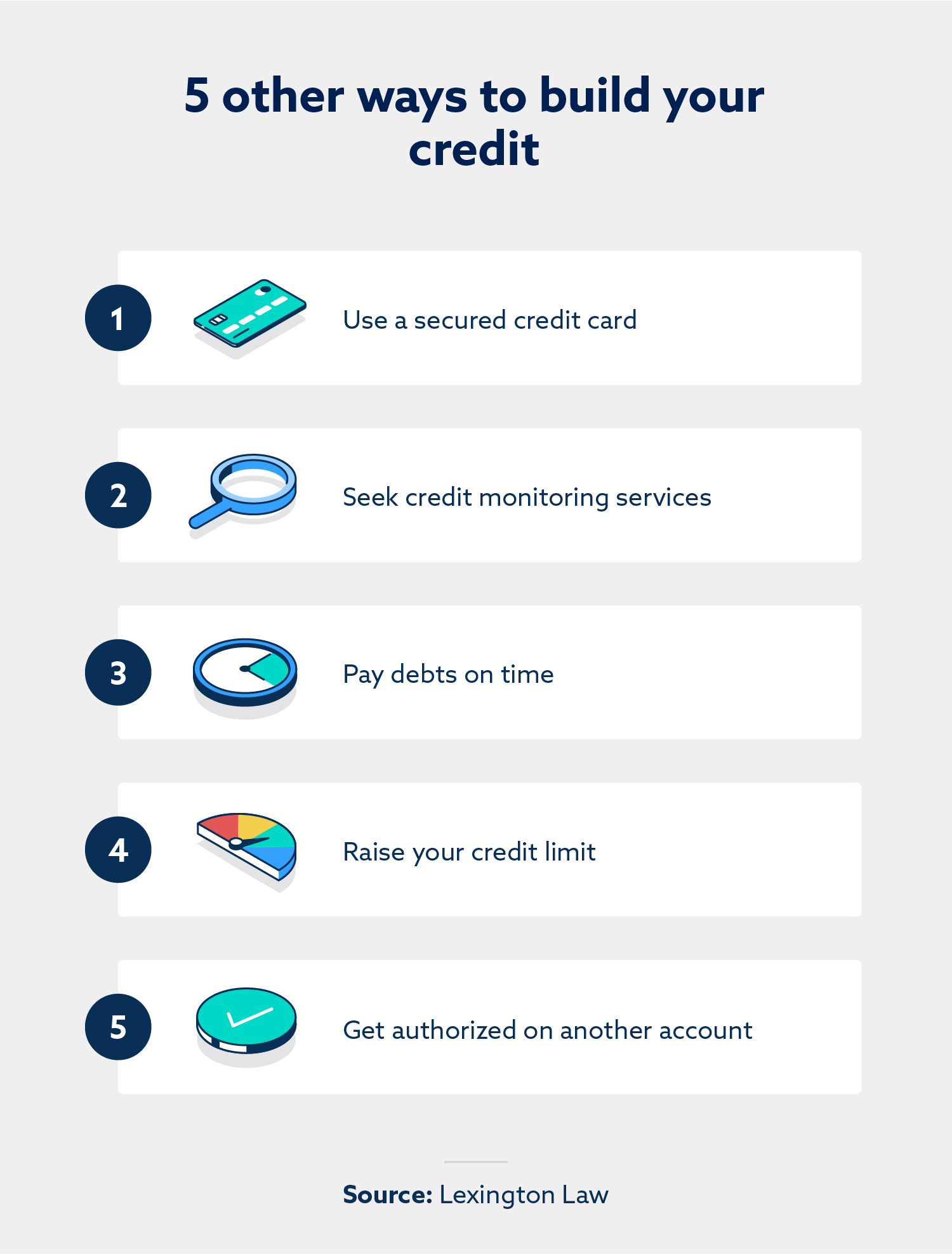

6. Secured Credit Cards as a Foundation

For those rebuilding after bankruptcy or starting from zero, secured cards—which require a cash deposit as collateral—provide a controlled environment to prove creditworthiness. In 2026, many of these cards offer "graduation" paths to unsecured lines within six months.

7. Advanced Credit Monitoring

Real-time monitoring has evolved from a luxury to a necessity. Modern services provide instant alerts for "hard inquiries" and changes in utilization, allowing consumers to react to potential identity theft or reporting errors within minutes.

8. The 35% Pillar: Timely Payments

No strategy outweighs the importance of payment history. It constitutes 35% of a FICO® score. In an era of automated banking, setting up "autopay" for the minimum amount due ensures that a single missed payment doesn’t cause a 50-to-100-point drop.

9. Managing the Credit Utilization Ratio

The second most important factor (30%) is utilization—the amount of credit used versus the total limit. Keeping this ratio below 30% is the standard advice, though top-tier "prime" borrowers often keep theirs below 10%. Requesting a limit increase without increasing spending is a "pro-tip" for instantly lowering this ratio.

10. Authorized User Status (Credit Piggybacking)

By being added as an authorized user to the account of a family member with a long, pristine history, a consumer can "inherit" that positive data. However, this is a double-edged sword; if the primary cardholder misses a payment, the authorized user’s score may also suffer.

11. Student-Specific Credit Products

Banks have tailored products for the Gen Z and Gen Alpha demographics. Student cards often lack annual fees and offer rewards for good grades, serving as an entry point for those with no prior history.

12. Rapid Rescoring for Home Buyers

Specific to the mortgage industry, rapid rescoring allows a lender to update a borrower’s credit file within days rather than months. This is typically used when a borrower pays down a large balance to qualify for a lower interest rate right before closing.

13. Professional Financial Counseling

The complexity of 2026’s financial products has led to a resurgence in financial advisors. These professionals provide tailored roadmaps, distinguishing between "bad debt" (high-interest consumer loans) and "good debt" (investments in education or real estate).

14. AI-Driven Credit-Building Apps

A new generation of apps uses AI to analyze spending patterns and suggest the optimal day to pay a bill to ensure the lowest balance is reported to the bureaus.

15. Hybrid Credit Builder Cards

Fintech companies have introduced cards that behave like a debit card but report to bureaus like a credit card. These are particularly popular among gig economy workers with fluctuating incomes.

II. Chronology: The Evolution of the Credit System

To understand the 2026 landscape, one must look at the pivotal shifts over the last decade:

- 2014-2018: The Rise of FICO 9. The industry began ignoring paid collection accounts and giving less weight to medical debt, recognizing that medical crises are not always indicative of financial irresponsibility.

- 2020-2022: The Pandemic Response. The CARES Act implemented temporary protections for credit scores during the COVID-19 era, preventing lenders from reporting late payments for those in forbearance.

- 2024: The Medical Debt Revolution. Major credit bureaus began removing all medical debts under $500 from credit reports, and the CFPB proposed a total ban on medical debt appearing on credit files to increase mortgage accessibility.

- 2025: The Integration of Alternative Data. "Trended data" became the standard. Lenders began looking not just at a snapshot of today’s debt, but at the trajectory of a consumer’s balances over the previous 24 months.

- 2026: The "Open Banking" Era. Consumers now have more control, choosing to "boost" their scores by voluntarily linking utility, phone, and even streaming service payment data to their profiles.

III. Supporting Data: The Cost of Poor Credit

The impact of these 15 strategies is best illustrated through the lens of cost. Data from 2025-2026 lending cycles shows a stark disparity:

- Mortgage Rates: A borrower with a 760 score may qualify for a 5.5% APR on a 30-year fixed mortgage. A borrower with a 620 score might be offered 7.2%. Over the life of a $400,000 loan, the difference in interest paid exceeds $150,000.

- Auto Insurance: In many states, credit scores influence insurance premiums. Statistical models suggest that drivers with "poor" credit pay up to 60% more for the same coverage than those with "excellent" credit, as insurers correlate credit health with risk management.

- Utilization Impact: For a consumer with a $10,000 total limit, carrying a $4,000 balance (40% utilization) can lower a score by 30 to 45 points compared to carrying a $500 balance (5%).

IV. Official Responses: Regulators and Industry Giants

The Consumer Financial Protection Bureau (CFPB) has remained vocal about the "automated injustice" of algorithmic scoring. In a recent 2026 briefing, the Bureau stated:

"Credit reports must be a reflection of reality, not a repository for outdated or inaccurate grievances. We are moving toward a system where consumers have total transparency into how their scores are calculated and a streamlined path to correcting errors."

The "Big Three" bureaus—Equifax, Experian, and TransUnion—have responded by launching more "opt-in" features. Experian’s leadership noted in a recent quarterly report that "the future of credit is permissioned data," suggesting that the most successful consumers in 2026 will be those who proactively share their positive financial behaviors beyond just credit card usage.

Consumer advocacy groups, however, remain cautious. The National Consumer Law Center (NCLC) warns that while alternative data helps many, it may also create new "digital redlining" if the algorithms inadvertently penalize lower-income zip codes or specific spending patterns.

V. Implications: The Future of Economic Access

The implications of credit-building strategies in 2026 extend far beyond the individual. On a macroeconomic level, a population with higher average credit scores leads to more robust consumer spending and lower default rates for banks, which stabilizes the housing market.

However, the "credit gap" remains a concern. As credit-building becomes more tech-dependent, those without digital literacy or access to high-speed internet may find themselves excluded from the best financial products. The 15 strategies outlined above are not just tips; they are essential survival skills for the 21st-century economy.

In conclusion, the path to a 850 score in 2026 is paved with a blend of old-fashioned discipline and modern technological leverage. By understanding the mechanics of utilization, the power of alternative data, and the legal rights afforded by the Fair Credit Reporting Act, consumers can transform their credit from a barrier into a bridge toward generational wealth.

Disclaimer: This report is for informational purposes and does not constitute legal or financial advice. For specific credit repair needs, consumers should consult with qualified professionals or legal firms specializing in credit law.