")

Whether you are a seasoned sommelier curating a high-end cellar or a casual enjoyer picking up a bottle for a weekend dinner, the price tag on your wine does more than reflect the quality of the vintage or the reputation of the vineyard. Hidden within every bottle is a complex, often opaque layer of government levies that significantly impacts the final cost. As of 2025, the estimated economic impact of consumption taxes on wine in the United States has reached a staggering $7.2 billion, highlighting a fiscal reality that few consumers fully grasp.

While the wine industry remains a robust pillar of the American economy, the regulatory framework governing its taxation is increasingly viewed by economists as an "arcane" relic of a bygone era. To understand the true cost of a glass of wine, one must peel back the layers of federal excise duties, state-level volume taxes, and the curious influence of state-run liquor monopolies.

The Landscape of Alcohol Taxation: A Categorical Mismatch

The American system of alcohol taxation is built on an outdated categorical hierarchy. Historically, states have levied taxes based on a rigid classification: beer is taxed at the lowest rate, wine at a moderate rate, and distilled spirits at the highest. The logic, however loose, was based on the average alcohol by volume (ABV) of each category.

However, as the market evolves—with high-ABV beers, low-alcohol spirits, and complex wine-based cocktails—this categorical structure has begun to fracture. When adjusted for actual alcohol content, the tax burden is rarely consistent. In many states, wine is taxed at a higher effective rate than beer, even when the ABV is comparable. In some jurisdictions, the bias is reversed, favoring wine over beer at a ratio of two-to-one.

Experts at the Tax Foundation and other policy institutes argue that this categorical approach is inefficient and distortive. They propose a fundamental shift toward "neutral" taxation: taxing products directly according to their actual alcohol content. Such a modernization would eliminate the confusion caused by "arcane" statutory definitions and create a simpler, more equitable landscape for both producers and consumers.

A Geography of Burden: From California to Kentucky

The disparity in wine taxation across state lines is stark. Because the U.S. grants states significant autonomy in how they regulate and tax alcohol, a bottle of wine can carry a vastly different tax burden depending on where it is purchased.

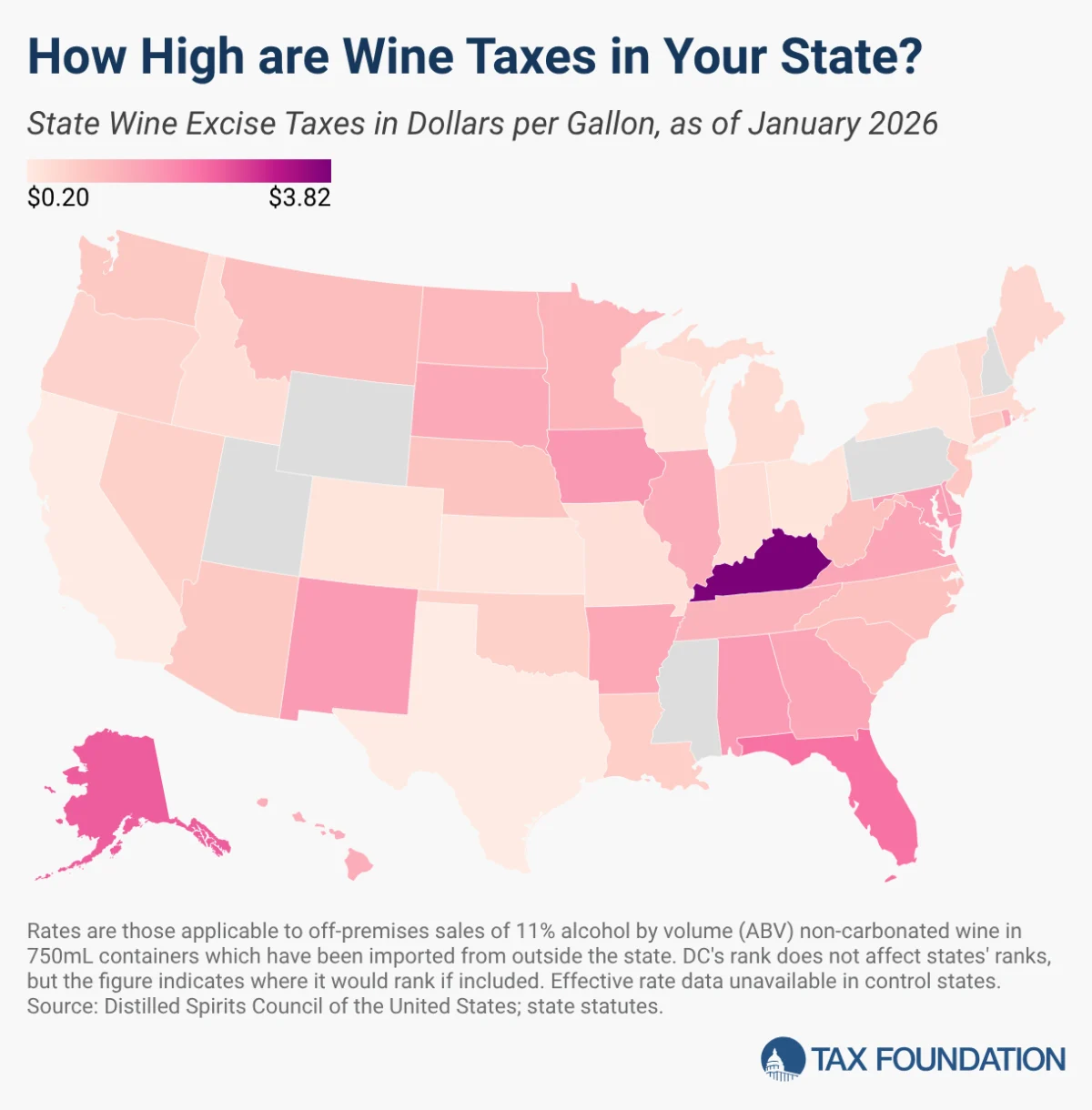

Kentucky currently holds the title for the highest tax burden on wine in the nation, with an effective rate of $3.82 per gallon. This is largely driven by the state’s 10 percent wholesale tax, which compounds the impact of standard excise duties. Following Kentucky, the states with the highest tax environments include Alaska ($2.50 per gallon), Florida ($2.25 per gallon), and Iowa ($1.75 per gallon).

On the opposite end of the spectrum lies California. As the heart of the American wine industry—home to the globally renowned Napa Valley—California maintains a tax rate of just $0.20 per gallon. This competitive environment is shared by Texas ($0.204 per gallon), Wisconsin ($0.25 per gallon), and both Kansas and New York, which sit at $0.30 per gallon.

These figures reflect "ad quantum" (volume-based) taxes, but they do not account for the additional fees and layers of complexity found in states that operate as government monopolies.

Chronology and Evolution of the Tax Code

The tax environment for alcohol has seen a slow but steady evolution since 2021. While many states have maintained static volume-based taxes, the inflationary pressures of the post-pandemic era have forced a reevaluation of how these revenues are collected.

Historically, excise taxes were designed to be simple, fixed-rate collections. However, as the value of the dollar shifts, these fixed-rate taxes lose their "real" value unless they are indexed to inflation. Conversely, ad valorem taxes (percentage-based) have proven volatile, fluctuating wildly based on consumer behavior and international trade policy. The imposition of tariffs on imported wine, for instance, has periodically suppressed industry growth, leading to unpredictable revenue streams for states relying on percentage-based levies.

The Monopoly Factor: When the State Becomes the Seller

Five U.S. states—Mississippi, New Hampshire, Pennsylvania, Utah, and Wyoming—have moved beyond simple regulation to seize a government monopoly on the sale of alcohol. In these states, the "tax" is often indistinguishable from the "markup," making it nearly impossible for consumers to identify exactly how much of their purchase price is going to state coffers.

- Mississippi: While the state levies a $0.35 per gallon excise tax, it also imposes a 3 percent markup dedicated to the Mental Health Programs Fund.

- New Hampshire: The New Hampshire Liquor Commission prides itself on low effective taxes (averaging $0.046 per gallon), but the state derives significant revenue through its 16.5 percent net margins on retail sales.

- Pennsylvania: The Pennsylvania Liquor Control Board (PLCB) wields broad authority to adjust prices. With reported net margins of 5.3 percent and an additional 18 percent tax on spirits, the price of alcohol is heavily manipulated to balance the state budget.

- Utah: Known for some of the strictest alcohol laws in the nation, Utah mandates a minimum markup of 88.5 percent on wine, effectively treating the consumer as a source of significant general tax revenue.

- Wyoming: The state combines a $0.28 per gallon excise tax with a 17.6 percent markup calculated by the state’s Liquor Division.

Industry Subsidies: The Hidden Goal of Excise Taxes

A unique feature of the current tax landscape is the "dedicated fund" model. Seven states—Colorado, Idaho, Iowa, Missouri, Oregon, Ohio, and Washington—utilize excise taxes to fund specific entities like Wine Commissions or Agriculture Business Development Funds.

In these states, the tax is not merely a revenue-gathering mechanism for the general budget; it is a tool for industrial policy. By taxing the entire market, these states essentially force consumers of out-of-state or budget-friendly wines to subsidize the promotion and development of local vineyards. While supporters argue this fosters economic growth, critics maintain that it creates an unlevel playing field, artificially inflating the cost of non-local products to protect domestic interests.

Implications for the Future: Modernization or Stagnation?

The rise of "ready-to-drink" (RTD) wine cocktails and low-alcohol wine innovations presents a significant challenge to the current regulatory framework. Because these products often straddle the line between wine, spirit, and seltzer, they frequently fall into a "no-man’s-land" of tax definitions.

Under current rigid statutes, these innovative products are often subject to "drastic over-taxation." When a product doesn’t fit neatly into a category, regulators often default to the most expensive tax bucket available, effectively punishing the manufacturer for innovation.

The implications of this status quo are clear:

- Consumer Price Inflation: Rigid, categorical taxes prevent the market from normalizing prices, keeping costs higher for the average consumer.

- Market Distortion: The practice of using taxes to fund specific industry lobbies prevents natural competition, favoring state-protected producers over innovators.

- Fiscal Inefficiency: Relying on unadjusted volume taxes leads to a long-term erosion of value, while volatile ad valorem taxes create budgetary instability for states.

Conclusion: A Call for Neutrality

As the wine industry navigates an era of shifting consumer preferences and global economic pressure, the consensus among policy researchers is that the current tax system is ripe for reform. The path forward, according to industry advocates, is the abandonment of arbitrary categorical definitions in favor of a direct tax based on actual alcohol content.

By taxing the ethanol content rather than the "type" of beverage, states could simplify the regulatory burden, lower costs for consumers, and encourage the growth of the next generation of wine products. Until such modernization occurs, however, the price of a bottle of wine will remain not just a reflection of the grape or the harvest, but a complex, localized calculation of the tax environment in which it was sold. For the American consumer, the lesson is clear: when you uncork your next bottle, you are participating in a multi-billion dollar fiscal experiment that spans from the vineyard to the state capital.