For many, a university education is viewed as the definitive gateway to professional success and financial stability. However, the reality of modern academia is more complex. According to the Education Data Initiative, approximately 39% of first-time, bachelor’s degree-seeking students fail to complete their programs within an eight-year window. This statistic reflects a myriad of challenges—ranging from unforeseen financial hardships and family emergencies to health crises—that can derail a student’s academic journey.

Yet, leaving school without a diploma does not erase the financial obligation of the debt incurred. Borrowers who do not graduate remain legally responsible for their student loans, often facing the same high interest rates as their degreed peers, but without the corresponding bump in earning potential that a degree typically provides. This creates a challenging financial paradox. While these individuals may feel trapped, refinancing remains a viable, albeit complex, pathway toward financial relief.

The Financial Reality of Non-Graduates

When a student leaves a degree program early, the burden of repayment begins almost immediately. For many, this debt feels particularly heavy because they lack the "credential premium" that justifies the investment. If you are struggling with high-interest private loans or federal debt that feels unmanageable, you may be considering refinancing.

Refinancing is the process of replacing one or more existing student loans with a single new loan from a private lender. The goal is to secure a lower interest rate, reduce the monthly payment amount, or consolidate multiple payments into one streamlined bill. While many traditional lenders automatically disqualify applicants who do not hold a degree, the market has shifted to accommodate a broader range of borrowers.

Chronology of the Repayment Struggle

For the average non-graduate, the timeline of financial pressure typically follows a specific, stressful progression:

- Departure from Academia: The student leaves their institution, triggering the six-month grace period for federal loans.

- Repayment Commencement: The first bill arrives, often accompanied by confusion regarding repayment plans and the lack of a degree to boost income.

- The "High-Interest" Trap: Many students realize their initial loans carry rates that make the principal balance grow rather than shrink.

- The Search for Alternatives: Faced with mounting interest, the borrower looks to consolidate or refinance, only to find that many banks have a "degree-required" policy.

- Strategic Shift: The borrower begins to look for "non-graduate friendly" lenders, focusing on building credit and steady income to qualify.

Supporting Data and Lending Options

It is a common misconception that graduation is a prerequisite for refinancing. While it is true that your options are more limited, several lenders have carved out niches for non-graduates who demonstrate financial responsibility.

Leading Lenders for Non-Graduates

If you are looking to lower your interest rate, these institutions are known for their more flexible criteria:

- Earnest: One of the more flexible lenders, Earnest focuses on your overall financial picture rather than just your educational status. Applicants need a strong credit score, at least six years since their last enrollment, and must have attended a Title IV-accredited institution.

- Citizens Bank: This institution offers a path for those who have a track record of reliability. They require that you have made at least 12 qualifying monthly payments after leaving school, proving you are a responsible borrower.

- Advantage Education Loan: With loan amounts starting at $7,500, this is a strong option for those who may need to lean on a cosigner if their individual credit history is not yet robust.

- EDvestinU: Catering to those who attended Title IV, degree-granting institutions, they offer refinancing up to $200,000. They are particularly friendly toward applicants who use a cosigner to secure a better rate.

- MEFA: Requiring a minimum of $10,000 in debt, MEFA focuses on U.S. citizens or permanent residents with a consistent history of on-time payments.

- RISLA: A standout for its national availability, RISLA does not require you to reside in or have attended school in Rhode Island. They offer significant flexibility in terms of loan amounts and repayment periods.

The Calculus of Refinancing: An Analytical View

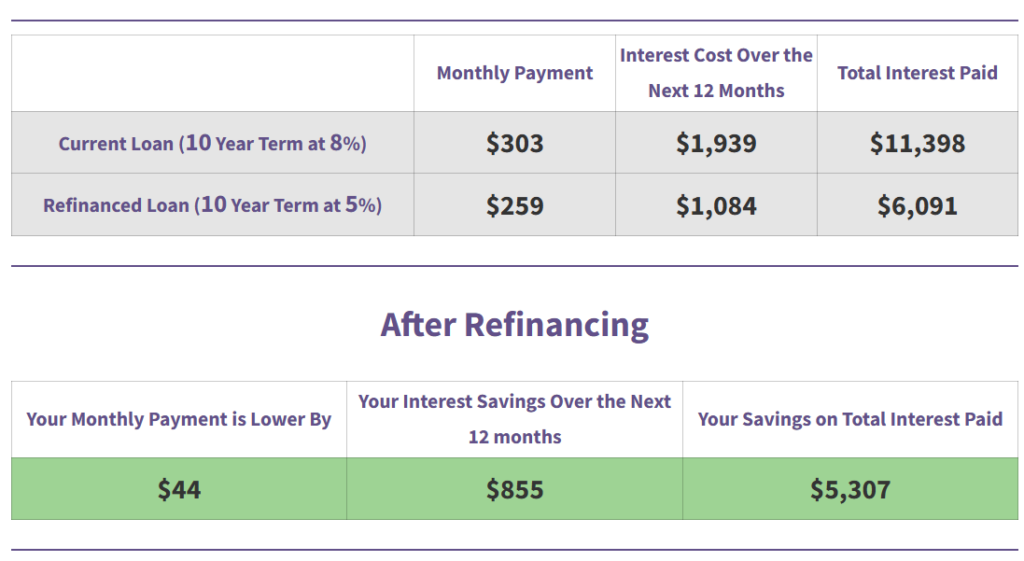

To understand the potential impact of refinancing, consider a borrower with a $25,000 balance at an 8% interest rate. Under a standard repayment plan, the monthly payment would be roughly $303. By refinancing that same balance to a 4.5% interest rate, the monthly payment drops to approximately $259. Over the life of the loan, this represents a savings of over $5,300 in interest alone.

However, these numbers must be weighed against the loss of federal protections. When you refinance federal loans into a private one, you permanently waive benefits such as:

- Income-Driven Repayment (IDR) Plans: These programs tie your payments to your earnings, which is crucial for those in lower-paying entry-level positions.

- Public Service Loan Forgiveness (PSLF): If you work for a non-profit or government entity, you lose the ability to have your balance forgiven after 10 years of service.

- Deferment and Forbearance: Private lenders rarely offer the same level of flexibility during periods of economic hardship compared to the federal government.

Official Perspectives and Expert Guidance

Financial advisors and loan experts consistently warn that refinancing is a "one-way door." Once you move federal debt to a private lender, you cannot move it back.

"The decision to refinance should be treated as a strategic financial move, not a quick fix," says a spokesperson for Student Loan Planner. "If you are struggling, always exhaust federal options first—such as the new Repayment Assistance Plan or IDR—before moving to the private market. If you have private loans already, however, there is little downside to refinancing to a lower rate, provided you meet the lender’s credit and income requirements."

Implications for Future Financial Health

For those who cannot yet qualify for refinancing, or who choose to keep their federal benefits, the path forward involves deliberate financial cultivation. To improve your chances of qualifying for a better rate in the future, consider the following strategies:

- Strengthen Your Credit Score: Pay down high-interest credit card debt and ensure all monthly bills are paid on time.

- Increase Your Debt-to-Income Ratio: Focus on career growth or a side hustle to show lenders that you have the income to support the loan.

- Seek a Cosigner: A parent or relative with strong credit can be the bridge between a rejected application and a low-interest approval.

- Monitor Your Payment History: Consistent on-time payments are the single most important metric for many lenders, specifically those like Citizens Bank.

Conclusion: Taking Control of Your Debt

The absence of a degree does not mean the absence of a financial future. While the road to managing student debt can feel isolating for non-graduates, the availability of specialized refinancing options provides a tangible way to save money and simplify the repayment process.

Before making a final decision, take the time to run your specific numbers through a professional-grade refinance calculator. Assess your long-term goals—do you plan on entering public service? Is your income likely to fluctuate? Do you have a trusted family member who could serve as a cosigner? By asking these questions, you transition from being a passive borrower to an active manager of your financial destiny.

If you remain unsure about the best path forward, consider booking a professional consultation to analyze your specific debt profile. Navigating the world of student loans is difficult, but with the right information, you can ensure that your past education doesn’t dictate your future financial success.