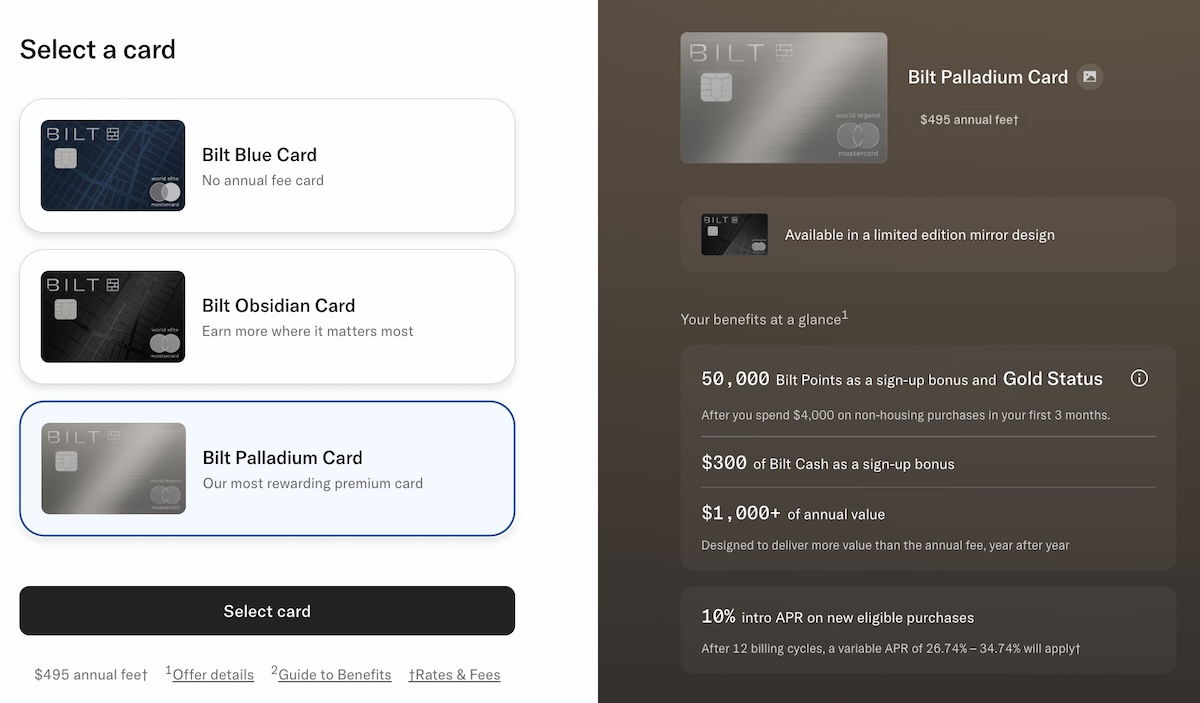

The landscape of personal finance and loyalty rewards has shifted significantly this year as Bilt, the platform best known for pioneering rewards on rent and housing payments, overhauled its credit card portfolio. Following a strategic transition from Wells Fargo to Cardless, Bilt now offers three distinct tiers of Mastercard products: the entry-level Bilt Blue Card, the mid-range Bilt Obsidian Card, and the ultra-premium Bilt Palladium Card.

For consumers who have long sought to optimize their monthly housing expenditures, these changes represent a pivot toward a more structured, tiered rewards model. However, the introduction of a $495 annual fee for the Palladium product has sparked a debate among rewards enthusiasts: does the value proposition justify the cost, or are users better served by lower-tier alternatives?

Main Facts: The New Bilt Hierarchy

Bilt’s new lineup is designed to cater to different spending profiles, from the casual renter to the high-net-worth individual who treats housing payments as a strategic financial lever.

- Bilt Blue Card (No Annual Fee): Designed for accessibility, this card allows users to enter the Bilt ecosystem without a recurring cost. While it earns 1x points on general spending, its primary value remains the ability to earn rewards on rent.

- Bilt Obsidian Card ($95 Annual Fee): A middle-ground option for those who want higher earning potential in specific categories without committing to the premium price tag of the Palladium card.

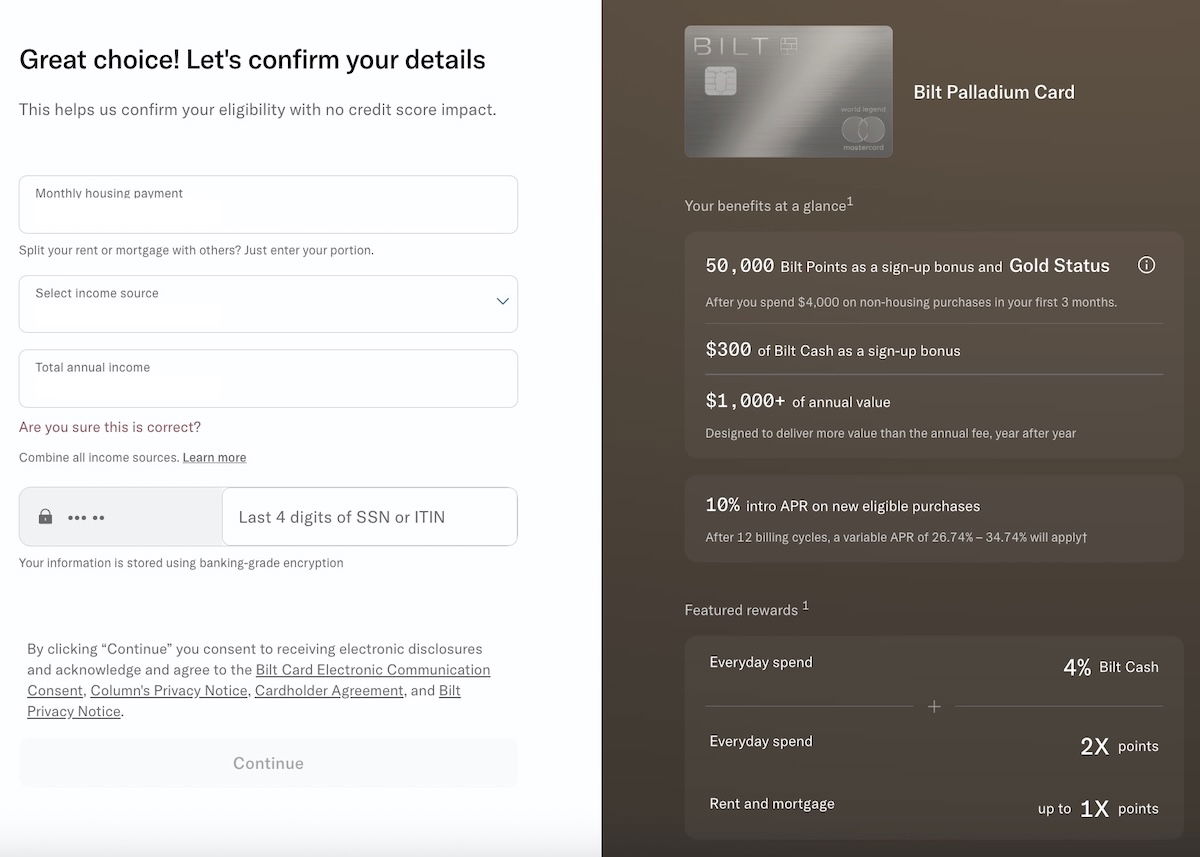

- Bilt Palladium Card ($495 Annual Fee): The flagship product. It is the only card in the current lineup to offer a significant welcome bonus—50,000 points and Bilt Gold status after spending $4,000 within the first 90 days—alongside a $300 Bilt Cash credit upon approval.

The core of Bilt’s value remains the transferability of its points to partners such as Alaska Airlines, World of Hyatt, and various other travel programs. Unlike traditional cards that focus solely on merchant categories, Bilt’s unique selling point is the ability to earn points on non-bonused everyday spending at a rate of 2x, coupled with the ability to turn spending into "Bilt Cash" to offset housing costs.

Chronology: The Transition to Cardless

The evolution of these products followed a major structural change in Bilt’s operational partnerships. Previously serviced by Wells Fargo, the transition to Cardless was executed to provide a more integrated experience for Bilt members.

- Early Year Announcement: Bilt announced the end of its legacy partnership, signaling a shift in how its rewards infrastructure would be managed.

- Migration Period: Existing cardholders were given the opportunity to migrate their accounts to the new Cardless-serviced platform. The process was marketed as a seamless transition, utilizing a soft credit pull rather than a hard inquiry for existing members.

- Application Launch: The new portal opened, allowing users to select between the Blue, Obsidian, and Palladium tiers.

- Integration of Benefits: Features like the points accelerator and the new hotel credit portal were rolled out, requiring users to navigate new redemption structures, specifically the requirement of a two-night minimum stay for the Palladium card’s hotel credits.

Supporting Data: The Math of the Palladium Card

To determine the true value of the Bilt Palladium Card, one must weigh the $495 annual fee against the tangible returns. For an individual spending $100,000 annually, the math becomes quite compelling.

If a user generates 2x points on that $100,000, they accrue 200,000 Bilt points. When paired with the ability to earn 4% back in Bilt Cash, the net return on investment (ROI) significantly outpaces most standard rewards cards. The "icing on the cake," as many analysts point out, is the ability to leverage this Bilt Cash to subsidize housing costs, effectively reducing one’s largest monthly liability while simultaneously accumulating travel currency.

However, this value is predicated on the user’s ability to maximize redemptions. Bilt points are highly valued due to their transfer partners; if a user is not utilizing high-value redemptions—such as luxury hotel stays or business-class flight awards—the effective value of the points drops, making the $495 fee harder to justify.

Official Responses and Platform Exclusions

One of the most critical aspects of the Bilt ecosystem, which has drawn both praise and frustration, is the explicit exclusion of certain spending categories. Notably, Bilt does not award points for tax payments. In the world of high-end credit card strategy, "manufactured spending" through tax payments is a common method for reaching spend thresholds. By excluding this, Bilt has signaled a move toward preventing "gaming" of their rewards system.

Bilt’s position is that their rewards are intended for genuine consumer behavior—rent and everyday living—rather than tax-related financial maneuvers. For many power users, this is a point of contention. It necessitates holding a secondary card for tax payments, complicating the wallet strategy of the average cardholder.

Furthermore, the $400 in annual hotel credits ($200 semi-annually) comes with a "two-night minimum stay" constraint. While this encourages brand loyalty within the Bilt portal, it limits the flexibility of the credit. For a business traveler who frequently stays in hotels for single nights, this benefit may effectively be worth $0, further straining the justification for the $495 annual fee.

Implications for the Future of Rewards

The existence of a "savvy" customer base is both a benefit and a risk for Bilt. Because their users are significantly more engaged than those of traditional banks, they are more likely to extract maximum value from every bonus and point redemption. This makes the Bilt customer base inherently less profitable for the issuer than a customer who carries a balance or ignores their points.

The long-term implication is a likely trend toward further "devaluations" or restrictions. If Bilt’s current redemption rates prove unsustainable, we may see a narrowing of transfer partner ratios or stricter requirements for earning points on rent.

Is it Worth the Investment?

The decision to apply for the Bilt Palladium Card currently rests on three pillars:

- Welcome Bonus Utilization: The 50,000-point bonus and $300 cash credit effectively wipe out the annual fee for the first year. It is a "no-lose" scenario for the first 12 months.

- High-Volume Spending: If you spend enough annually to trigger the 2x points threshold on non-bonused items, the card pays for itself through sheer volume.

- Transfer Partner Strategy: If you are a travel hacker who values World of Hyatt or Alaska Airlines miles, the earning potential of the Bilt ecosystem remains peerless.

However, for those who value simplicity or do not have high monthly housing/general expenses, the Bilt Blue Card remains the superior choice. It offers the core utility of the Bilt ecosystem—paying rent and earning points—without the pressure to justify a high-tier fee.

Ultimately, the Bilt Palladium Card is an experimental tool for the modern consumer. It is a product for those who enjoy the "game" of credit card rewards. As we move into the next year, the market will be watching closely to see if Bilt maintains its aggressive earning structures or if the economic realities of the platform force a change in strategy. For now, the consensus is clear: if you are a high-spender, the Palladium is worth the trial. If you are a casual user, stick to the no-fee alternative and protect your bottom line.