By Financial News Desk

In an era of fluctuating interest rates and tightening lending standards, the American consumer’s relationship with their credit score has shifted from passive observation to active management. A comprehensive new survey conducted by Lexington Law, a leading voice in credit repair and consumer advocacy, has unveiled a significant trend: nearly two-thirds of consumers are currently engaged in a concerted effort to rehabilitate their financial reputations.

The findings, released this week, highlight a growing demand for professional intervention in the face of complex credit reporting systems. With over 73% of respondents identifying credit repair as their primary financial need, the data suggests that the modern consumer no longer views a low credit score as a permanent life sentence, but rather as a challenge that requires specialized tools and legal expertise to overcome.

Main Facts: A Portrait of Financial Determination

The core of the Lexington Law survey results underscores a powerful sentiment of resilience among American households. The data indicates that 63.4% of respondents are not merely concerned about their credit but are actively taking steps to improve it. This group is split evenly into two distinct categories: those who are aware of a generally low score and wish to elevate it (31.7%), and those who have identified specific, often erroneous, negative items on their reports that they want removed (31.7%).

This 50/50 split reveals a sophisticated understanding of credit mechanics. Consumers are beginning to distinguish between "credit building"—which involves positive habits like timely payments—and "credit repair," which involves the legal process of challenging inaccurate, unverified, or unfair derogatory marks.

However, the survey also exposed a persistent "knowledge gap." Despite the ubiquity of financial apps and "free score" advertisements, 8.65% of respondents admitted they had no idea what their current credit score was. In a financial ecosystem where credit scores influence everything from the ability to rent an apartment to the interest rates on a car loan, this nearly 9% of the population remains "financially invisible," navigating the economy without a clear map of their standing.

Chronology: The Evolution of Consumer Credit Advocacy

To understand the current surge in credit repair interest, one must look at the historical trajectory of consumer rights in the United States.

The journey began in earnest with the Fair Credit Reporting Act (FCRA) of 1970, which established the first set of rules regarding how consumer data is collected and distributed. For decades, the system remained largely opaque, with consumers having little recourse when errors occurred. The landscape shifted again in 1996 with the Credit Repair Organizations Act (CROA), which provided a legal framework for companies to assist consumers in exercising their rights under the FCRA.

Lexington Law entered this space in 2004, a pivotal year that marked the beginning of the digital credit era. At that time, the primary hurdle for consumers was access; getting a copy of a credit report often required a written request and a waiting period. Over the last two decades, the "chronology of credit" has accelerated:

- 2004–2010: The rise of online banking made credit scores more visible, but the process of disputing errors remained a manual, bureaucratic nightmare for the average individual.

- 2010–2020: The post-Great Recession era saw a massive spike in identity theft and reporting errors as financial institutions merged and data was migrated across legacy systems.

- 2020–Present: The COVID-19 pandemic and subsequent inflationary period created a "perfect storm." While government stimulus provided temporary relief, the expiration of those programs, combined with high interest rates, has forced consumers to look at their credit scores as a survival tool to lower their cost of living.

This chronology explains why, in 2024, the demand for credit repair has reached a fever pitch. Consumers are no longer content to wait for "time" to heal their credit; they are seeking proactive solutions to meet immediate economic pressures.

Supporting Data: Analyzing the "Multi-Faceted" Approach

The survey didn’t just ask about credit repair; it delved into the secondary tools consumers are using to stabilize their financial foundations. While 73.2% prioritized credit repair services, the data showed a "cluster" of interests that suggest a holistic approach to financial health:

- Credit Score Monitoring (26.8%): Consumers want real-time feedback. The interest in monitoring suggests that people are wary of "surprise" drops in their scores and want to catch identity theft or reporting errors the moment they happen.

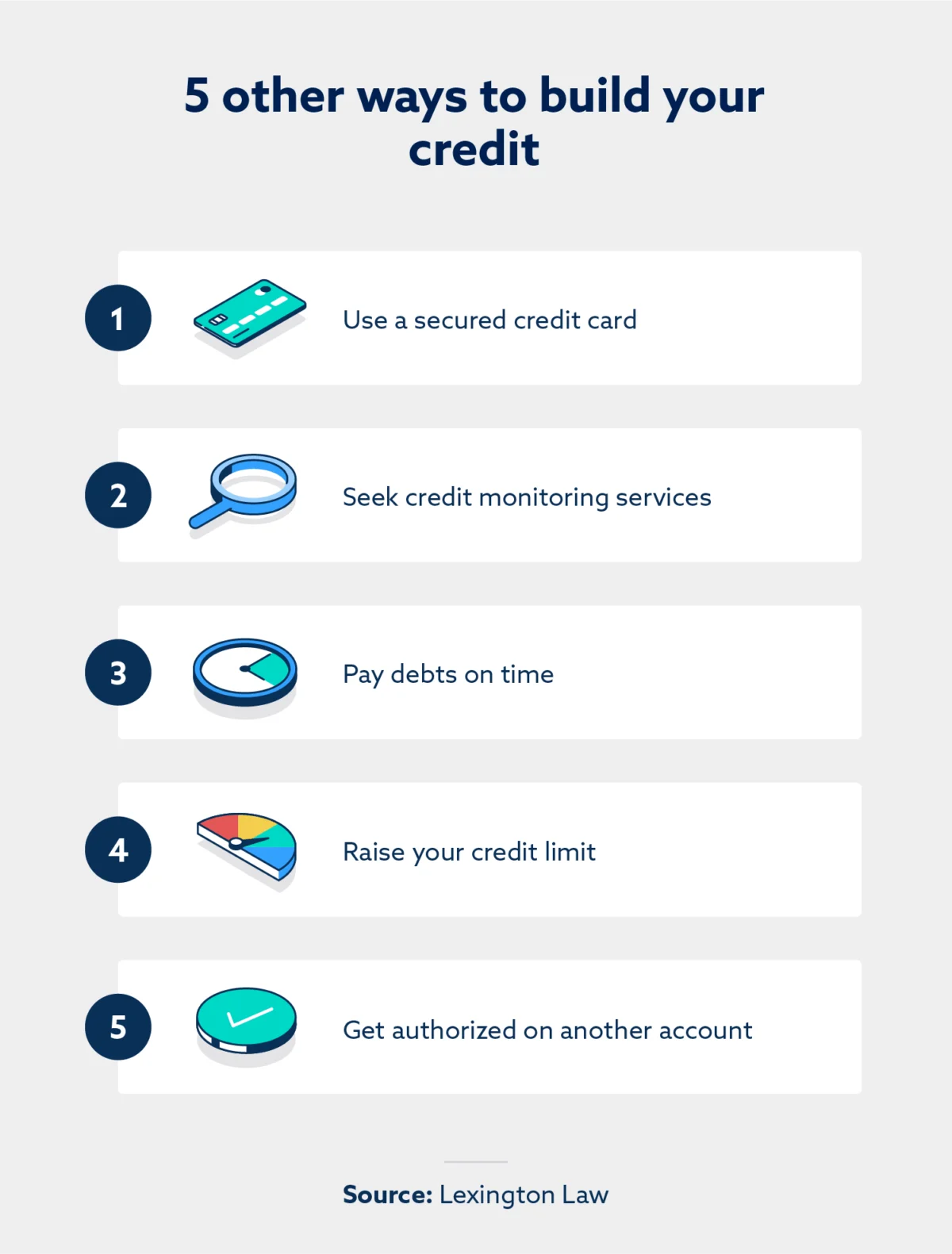

- Credit Building Tools (25.77%): This represents the "positive" side of the ledger—using secured cards or credit-builder loans to prove creditworthiness.

- Identity Theft Protection (24.74%): As data breaches become a weekly occurrence in the corporate world, nearly a quarter of respondents see identity protection as inseparable from credit health.

- Debt Consolidation (23.71%): This reflects the burden of high-interest revolving debt. Consumers are looking to streamline their payments to improve their debt-to-income ratios, a key component of the FICO score.

Table 1: Consumer Priorities in Financial Health

| Service | Percentage of Interest |

|---|---|

| Credit Repair Services | 73.20% |

| Credit Score Monitoring | 26.80% |

| Credit Building Tools | 25.77% |

| Identity Theft Protection | 24.74% |

| Debt Consolidation | 23.71% |

The dominance of "Credit Repair Services" in this data set—outpacing the next closest category by nearly 50 points—indicates that consumers perceive "fixing the past" as more urgent than "monitoring the present."

Official Responses: The Professional Perspective

Representatives from Lexington Law emphasize that the survey results validate their long-standing mission. The firm asserts that the complexity of the law is the primary barrier for most Americans.

"Credit laws are not designed to be easily navigated by the layperson," a spokesperson for the firm noted. "Between the FCRA, the FDCPA (Fair Debt Collection Practices Act), and the CROA, there is a dense thicket of regulations. Our survey shows that people recognize this. They aren’t just looking for a quick fix; they are looking for experienced professionals—paralegals and attorneys—who understand how to hold credit bureaus and creditors accountable."

Lexington Law’s official stance is that the credit reporting system is fundamentally flawed. According to various Federal Trade Commission (FTC) studies, as many as one in five consumers have a verified error on at least one of their credit reports. The firm argues that when 73% of survey respondents ask for repair services, they are reacting to a system that frequently fails to produce accurate data.

"Our role is to empower the consumer," the firm stated. "When a member sees that 63% of their peers are in the same boat, it removes the stigma of a low credit score. It turns a source of shame into a project of empowerment."

Implications: What This Means for the American Economy

The implications of this data are far-reaching, touching on the housing market, the labor force, and the broader macroeconomy.

1. The Real Estate Market Barrier:

With mortgage rates at decade-highs, a difference of 50 points on a credit score can mean the difference between an affordable monthly payment and being priced out of a home entirely. The high demand for credit repair (73.2%) suggests a massive segment of the population is currently "sidelined" from the housing market, waiting for their scores to reach the threshold for prime lending rates.

2. The Rental Crisis:

Property management companies are increasingly using automated "credit screening" software. A single unverified negative item can lead to an automatic rejection. The survey’s finding that 31.7% of people want specific negative items removed suggests a direct link to the struggle for housing stability.

3. The Psychological Shift:

Perhaps the most profound implication is the shift in consumer psychology. For decades, the credit score was a "black box" that judged the consumer. The survey results indicate a reversal: the consumer is now judging the score. By seeking repair services and building tools, Americans are treating their credit reports as a "financial resume" that they have the right to edit and improve.

4. Economic Mobility:

If 63% of people succeed in their journey to improve their credit, the result would be a significant unlocking of consumer purchasing power. Higher scores lead to lower interest rates, which leaves more disposable income in the pockets of families. This "credit-driven stimulus" could be a vital component of economic growth in the coming years.

Conclusion: Moving Toward a Transparent Future

The Lexington Law survey serves as a wake-up call to the financial industry. The data is clear: the American consumer is motivated, informed, and ready to act. However, they are also overwhelmed by the technicalities of a system that often feels stacked against them.

As we move forward, the focus must remain on transparency and education. While the "Credit Knowledge Gap" remains a concern—particularly for the 8.65% who do not know their scores—the overwhelming trend is toward proactive management. For the millions of Americans represented in this survey, the journey to a better credit score is not just about a number; it is about reclaiming their seat at the table of the American economy.

For those ready to begin that journey, the message from industry experts is consistent: you do not have to navigate the complexities of the law alone. With the right support, the path from a "low score" to "financial freedom" is not just possible—it is currently being walked by 63% of the nation.