Main Facts: The Evolving Landscape of Consumer Credit

In the financial ecosystem of 2026, a credit score remains the most influential three-digit number in a consumer’s life. As the global economy grapples with shifting interest rates and a competitive housing market, the ability to establish and maintain a robust credit profile has transitioned from a financial advantage to a fundamental necessity. Both FICO® and VantageScore®—the industry standards—continue to utilize a range of 300 to 850, where higher scores signal lower risk to lenders, translating into lower interest rates and expanded borrowing capacity.

However, the methodology for "building credit fast" has undergone a significant transformation. Traditional methods, such as taking out a high-interest personal loan, are being eclipsed by "alternative data" integration and fintech-driven solutions. Today, credit building is no longer a passive process of waiting years for history to accumulate; it is an active, strategic endeavor.

Financial experts emphasize that while every credit profile is unique, the core pillars of credit health remain consistent: payment history (comprising approximately 35-40% of a score) and credit utilization (accounting for roughly 30%). In 2026, the focus has shifted toward high-velocity strategies that leverage every financial move a consumer makes—from paying rent to managing subscription services.

Chronology: From Traditional Limits to Modern Accessibility

To understand the current state of credit building, one must look at the timeline of how consumer data has been reported and utilized over the last decade:

- 2015–2019: The Traditional Era. Credit scores were almost exclusively determined by "hard" credit data—credit cards, mortgages, and auto loans. Rent and utility payments were largely invisible to the "Big Three" bureaus (Equifax®, Experian®, and TransUnion®).

- 2020–2022: The Fintech Surge. The rise of "Buy Now, Pay Later" (BNPL) and credit-builder apps began to bridge the gap for the "credit invisible"—those with no formal credit history. The industry saw the introduction of tools like Experian Boost, allowing consumers to self-report utility bills.

- 2023–2025: The Integration of Alternative Data. Federal regulators and credit bureaus began formalizing the inclusion of rent reporting and cash-flow data (checking account activity) into mainstream scoring models. This era marked a shift toward "inclusive credit."

- 2026: The Holistic Credit Era. As of this year, credit building is a multi-channel effort. The 15 strategies outlined in current financial literature represent a synthesis of traditional banking discipline and modern technological leverage.

Supporting Data: 15 High-Impact Strategies for 2026

The path to a higher score in 2026 is paved with specific, actionable tactics. These strategies are categorized by their speed of impact and the specific score components they target.

I. Institutional Credit-Building Tools

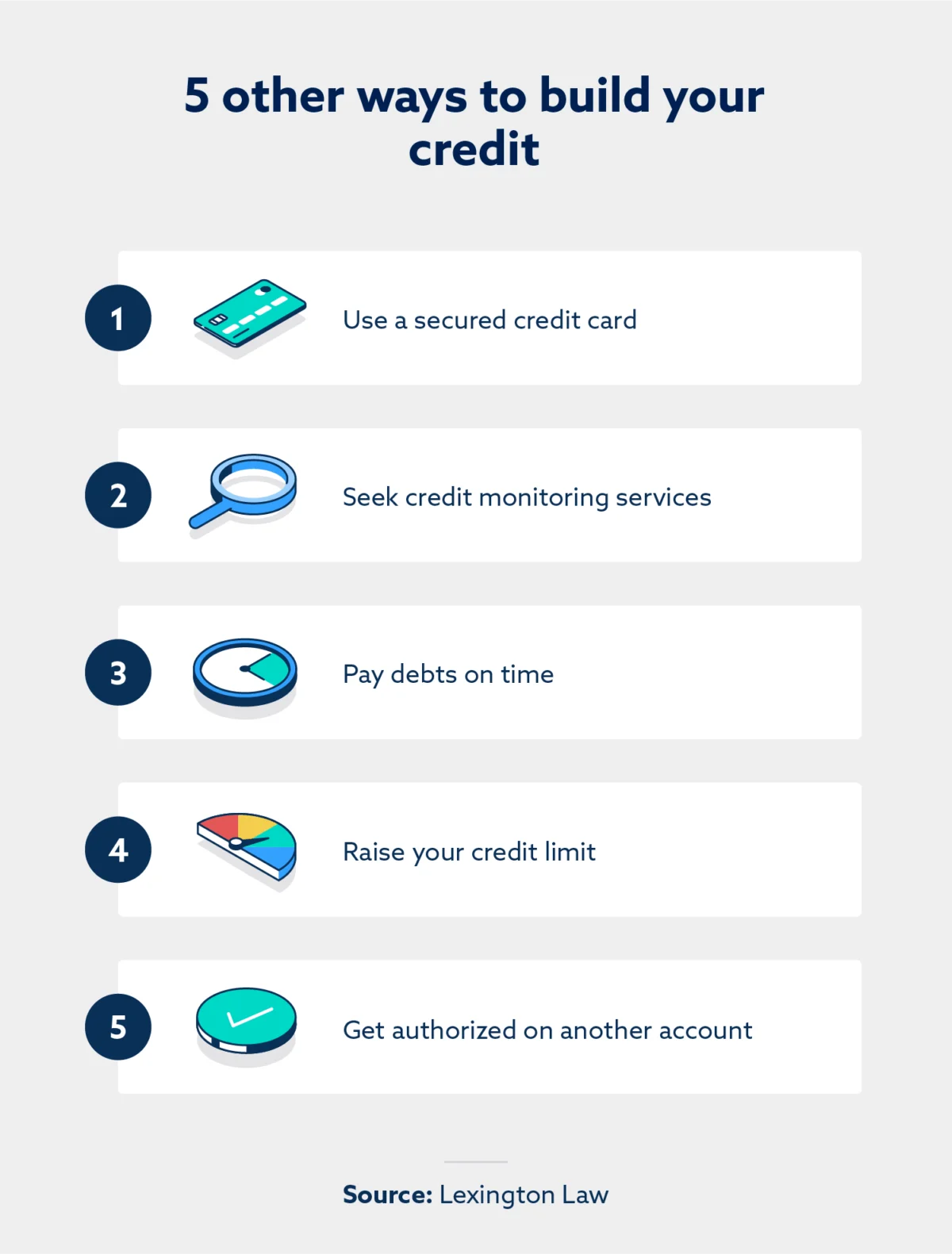

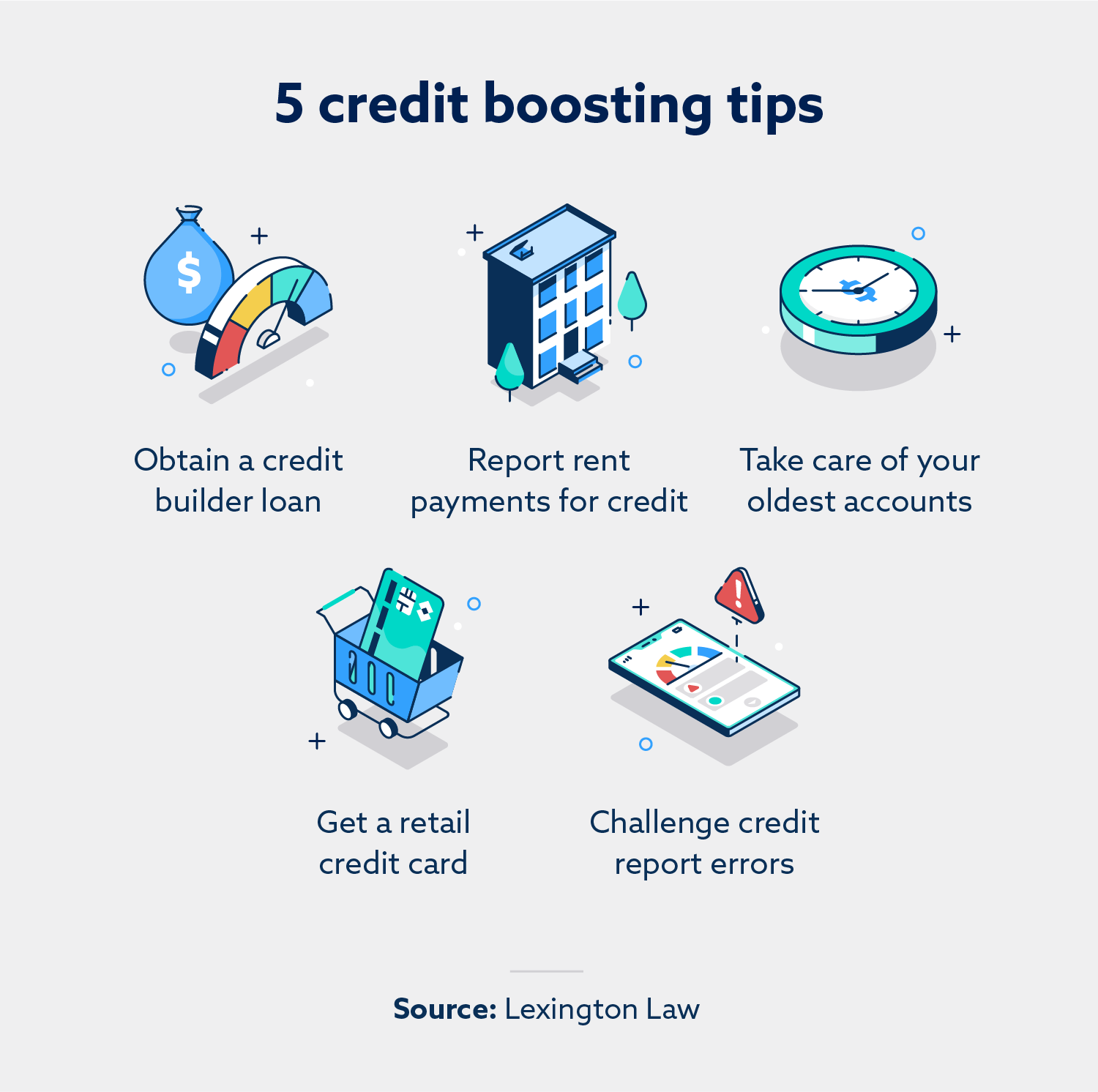

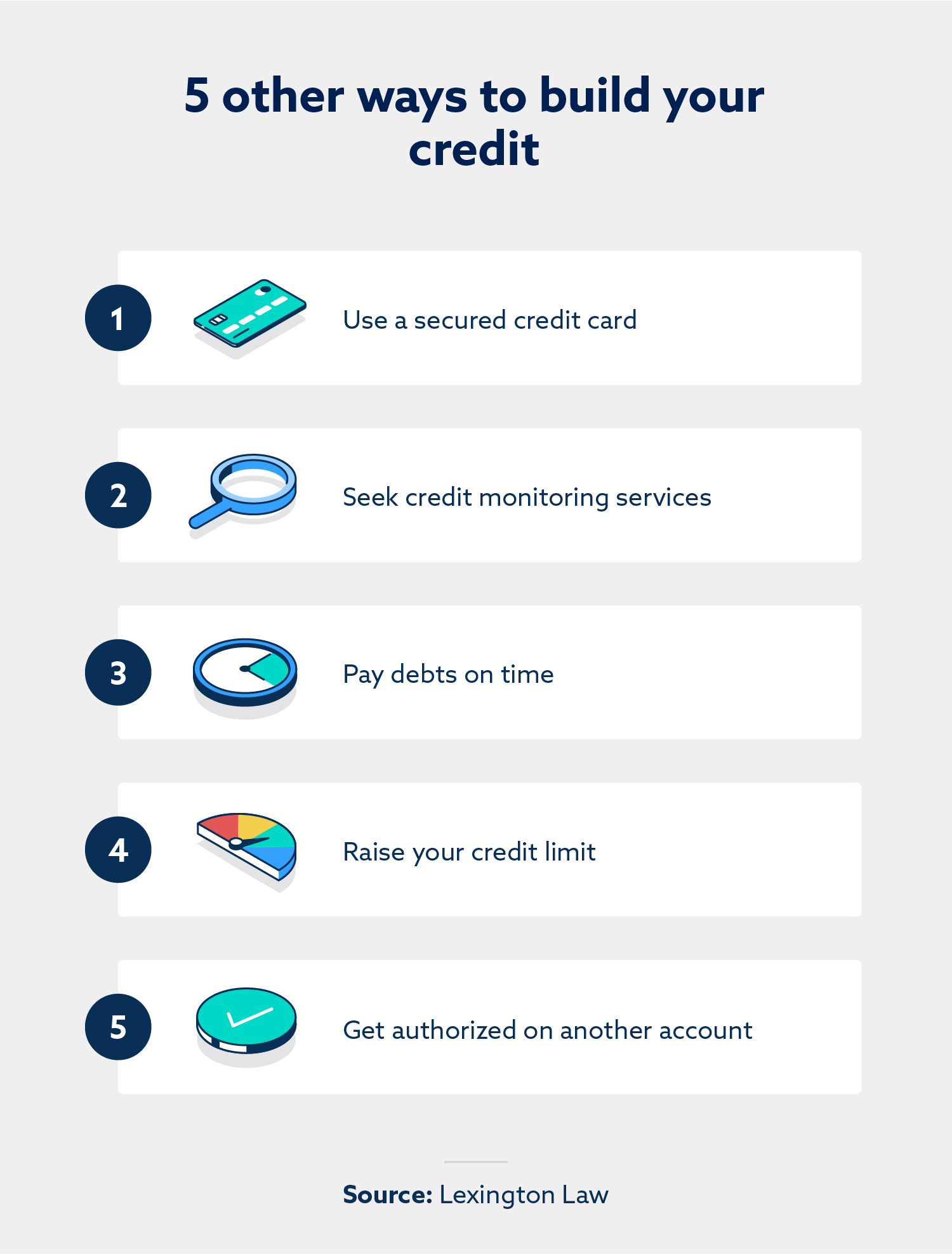

1. Credit Builder Loans: Unlike traditional loans, these function as a reverse installment plan. The lender holds the "loaned" amount in a secured account while the borrower makes monthly payments. These payments are reported to bureaus, building a positive history. Upon completion, the borrower receives the funds.

2. Secured Credit Cards: These remain a cornerstone for those with "thin" files. By providing a cash deposit as collateral, consumers can access a credit line. In 2026, many secured cards offer "graduation" paths to unsecured lines in as little as six months of responsible use.

3. Student Credit Cards: Designed for those with limited income and history, these cards have lower entry barriers but require proof of enrollment and responsible management to avoid high-interest traps.

II. Leveraging Recurring Expenses

4. Rent Payment Reporting: Historically, rent was the largest expense that didn’t help a credit score. Today, services can transmit rental data to all three bureaus. For a consumer starting from scratch, this can establish a score in as little as 90 days.

5. Credit-Building Apps: Modern apps analyze a user’s bank account to identify regular payments for streaming services, utilities, and insurance, reporting these "on-time" behaviors to the bureaus to pad the payment history metric.

III. Strategic Account Management

6. Maintaining Oldest Accounts: Length of credit history accounts for 15% of a FICO® score. Journalistic data shows that consumers who keep their first credit card open—even if unused—maintain a higher "average age of accounts," which stabilizes their score during new applications.

7. Increasing Credit Limits: By requesting a higher limit on an existing card without increasing spending, a consumer immediately lowers their credit utilization ratio. Experts recommend keeping utilization below 30%, though the "prime" tier of borrowers often stays below 10%.

8. Becoming an Authorized User: Known as "credit piggybacking," this allows a person to be added to the account of someone with excellent credit. The primary cardholder’s history is then reflected on the authorized user’s report.

IV. Corrective and Expedited Actions

9. Challenging Credit Report Errors: Inaccuracies—such as accounts that don’t belong to the consumer or incorrectly reported late payments—can decimate a score. Legal firms, such as Lexington Law, specialize in identifying these discrepancies and challenging them under the Fair Credit Reporting Act (FCRA).

10. Rapid Rescoring Services: Primarily used during the mortgage application process, this service allows a lender to expedite the updating of a credit report (within days rather than months) after a balance is paid off or an error is corrected.

11. Credit Monitoring Services: These tools provide real-time alerts on score changes and potential identity theft, allowing consumers to react instantly to negative fluctuations.

V. Consumer Habits and Expert Guidance

12. Timely Payments: This remains the most critical factor. In 2026, automation through "autopay" features has become the standard recommendation to ensure no payment is ever missed.

13. Retail Credit Cards: While often carrying higher interest rates, these cards are easier to obtain and can serve as a quick way to diversify a "credit mix" for frequent shoppers.

14. Meeting with Financial Advisors: Professional guidance helps in creating a tailored "roadmap" to credit health, moving beyond generic advice to specific debt-reduction strategies.

15. Specialized Credit Builder Cards: Distinct from secured cards, these often function through fintech platforms that link to a bank account to prevent overspending, ensuring the user only spends what they can immediately pay back.

Official Responses: Regulatory and Industry Perspectives

The shift toward rapid credit building has drawn significant attention from federal regulators and industry leaders. The Consumer Financial Protection Bureau (CFPB) has recently emphasized the importance of data accuracy, noting that as more "alternative data" (like rent and utilities) enters the system, the risk of reporting errors increases.

"The integrity of the credit reporting system is the bedrock of our financial economy," a CFPB representative noted in a recent symposium. "While we encourage innovations that help ‘credit invisible’ Americans enter the system, we are vigilantly monitoring firms to ensure that consumers are not being exploited by high-fee ‘credit repair’ schemes that promise the impossible."

Major credit bureaus have also responded by launching their own proprietary tools to help consumers "self-optimize." Spokespersons from Experian and TransUnion have stated that the goal for 2026 is "transparency," allowing consumers to see exactly how specific actions—like paying down a specific $500 debt—will impact their score before they even make the payment.

Implications: The Socioeconomic Impact of Credit Health

The implications of these credit-building strategies extend far beyond individual bank accounts. In the 2026 economy, credit health is increasingly tied to the "wealth gap." Those who can quickly build or repair their credit gain access to homeownership and entrepreneurship, which are the primary drivers of generational wealth.

However, experts warn of a "digital divide" in credit. As credit building becomes more reliant on apps, smartphones, and digital banking, those in "underbanked" communities may find it harder to utilize these 15 strategies. The move toward holistic data also raises privacy concerns; as consumers share more of their daily financial life (rent, utilities, Netflix subscriptions) with bureaus, the "surveillance" of personal spending habits reaches unprecedented levels.

Ultimately, the strategies of 2026 prove that credit is no longer a static grade assigned by a distant institution. It is a dynamic, manageable asset. For the modern consumer, the message is clear: through a combination of traditional discipline and the strategic use of new financial technology, the "doors of opportunity" can be opened faster than ever before.

Editorial Note: This article is for informational purposes and does not constitute legal or financial advice. Consumers are encouraged to consult with certified financial planners or legal experts regarding their specific credit situations.