In an era where financial fluidity dictates the quality of one’s lifestyle, the credit score has evolved from a mere metric into a definitive "financial passport." As we observe Credit Awareness Month, the spotlight intensifies on the systemic importance of credit health. While many consumers view credit scores as enigmatic or punitive, financial experts and legal advocates emphasize that credit is a manageable asset. By understanding the underlying mechanics of credit reporting and adopting disciplined fiscal habits, individuals can unlock significant opportunities in housing, lending, and even employment.

The following analysis explores the fundamental pillars of credit management, the regulatory framework protecting consumers, and the long-term implications of maintaining a robust credit profile.

1. Main Facts: The Five Pillars of Credit Scoring

To navigate the complexities of credit, one must first understand the mathematical models—primarily FICO and VantageScore—that determine a consumer’s creditworthiness. While these models vary slightly, they generally rely on five core pillars:

I. Payment History (35%)

This is the most critical factor in any scoring model. It reflects whether a consumer pays their obligations on time. Even a single 30-day delinquency can cause a significant drop in a score, and major derogatory marks like foreclosures or bankruptcies can linger for seven to ten years.

II. Credit Utilization (30%)

Also known as "amounts owed," this metric compares the total credit used against the total credit available. High utilization—even if bills are paid in full—can signal to lenders that a consumer is overextended.

III. Length of Credit History (15%)

The "age" of your accounts matters. This factor considers the age of your oldest account, the age of your newest account, and the average age of all accounts. A longer history provides more data for lenders to assess risk.

IV. Credit Mix (10%)

Lenders prefer to see a variety of credit types, such as "revolving" credit (credit cards) and "installment" loans (mortgages, auto loans, or student loans). Successfully managing different types of credit demonstrates financial versatility.

V. New Credit (10%)

This tracks how many new accounts have been opened or applied for recently. Frequent applications result in "hard inquiries," which can temporarily suppress a score.

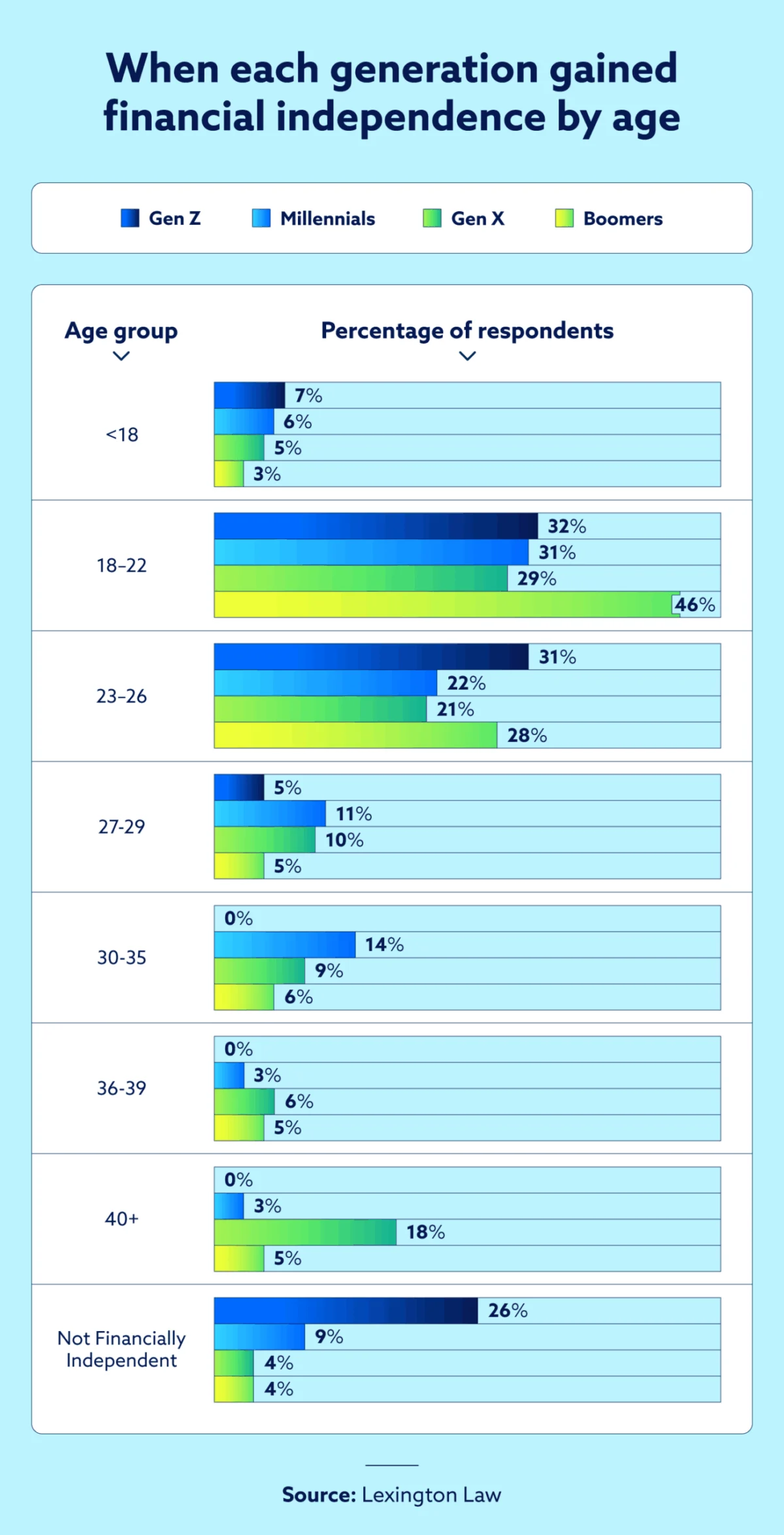

2. Chronology: The Lifecycle of Credit Management

Building and maintaining credit is not a static event but a chronological journey that spans an individual’s adult life. Understanding the timeline of credit allows consumers to plan for major milestones.

Phase 1: The Establishment (Ages 18–25)

The journey typically begins with "thin files"—profiles with little to no credit history. During this phase, individuals often utilize secured credit cards or become authorized users on a parent’s account. The goal here is to initiate the "Length of Credit History" clock.

Phase 2: Strategic Expansion (Ages 25–40)

As consumers enter their prime earning years, they often transition to installment loans, such as auto financing or first-time mortgages. This is the period where "Credit Mix" becomes vital. Consumers must be wary of "lifestyle creep," where increased spending leads to higher credit utilization, potentially damaging scores just as they seek major loans.

Phase 3: The Maintenance and Monitoring Era (Ages 40+)

For established consumers, the focus shifts to protecting a high score. This involves regular monitoring for identity theft and ensuring that old, dormant accounts are not closed prematurely. Closing an old account can shorten the average age of credit and reduce the total available credit limit, inadvertently spiking the utilization ratio.

Phase 4: Recovery and Rectification (Post-Financial Setback)

Financial setbacks—medical emergencies, job loss, or divorce—can happen at any time. The chronology of credit repair begins the moment a consumer recommits to on-time payments. Over time, the impact of old negative marks fades, and new, positive data begins to dominate the report.

3. Supporting Data: The Economic Impact of a Credit Score

The difference between a "Fair" score (580–669) and an "Exceptional" score (800–850) is not just a matter of pride; it translates into thousands of dollars in real-world costs.

The Cost of Borrowing

According to data from the Informa Research Services, a consumer with a 760 FICO score might qualify for a 30-year fixed mortgage at an interest rate 1.5% to 2% lower than someone with a 620 score. Over the life of a $300,000 loan, this difference can amount to over $100,000 in additional interest payments for the lower-scoring individual.

The Prevalence of Inaccuracy

A landmark study by the Federal Trade Commission (FTC) revealed that approximately 20% of consumers had an error on at least one of their three major credit reports (Equifax, Experian, and TransUnion). Furthermore, 5% of consumers had errors so significant that they were being overcharged for financial products. This underscores the necessity of the "Annual Credit Report" check-up.

The 30% Threshold Myth

While many financial advisors suggest keeping credit utilization below 30%, data from FICO suggests that "high achievers"—those with scores above 800—typically maintain a utilization rate of less than 7%. This "gold standard" of utilization is a primary driver for those seeking to move from "Good" to "Excellent" status.

4. Official Responses and Legal Frameworks

The credit industry is governed by a strict set of federal laws designed to protect consumers from predatory practices and inaccurate reporting.

The Fair Credit Reporting Act (FCRA)

The FCRA is the cornerstone of consumer credit rights. It mandates that the information in a credit report must be accurate, complete, and verified. If a consumer identifies an error, the credit bureaus are legally obligated to investigate and remove the item if it cannot be verified within 30 days.

The Role of the Consumer Financial Protection Bureau (CFPB)

The CFPB serves as the federal watchdog for the financial industry. It frequently issues reports on the conduct of credit bureaus and debt collectors. Official guidance from the CFPB emphasizes that consumers have the right to dispute inaccurate information themselves or enlist the help of professional services.

Expert Perspective: Lexington Law

Legal advocates, such as those at Lexington Law, highlight that credit awareness is a form of consumer empowerment. They argue that many consumers are unaware of their rights under the FCRA and the Fair Debt Collection Practices Act (FDCPA). By leveraging these laws, consumers can ensure that their credit reports are a fair and accurate reflection of their financial behavior, rather than a collection of outdated or erroneous data points.

5. Implications: Why Credit Awareness Matters Beyond Loans

The implications of a credit score extend far beyond the ability to get a credit card. In the modern economy, credit health is a proxy for reliability and stability.

Housing and Utilities

Landlords increasingly use credit scores to screen tenants. A low score may result in a rejected rental application or a requirement for a much higher security deposit. Similarly, utility companies (electricity, water, and internet) often check credit to determine if a deposit is required to initiate service.

Employment Opportunities

In several states, employers are permitted to check a modified version of a candidate’s credit report, particularly for roles involving financial responsibility, access to sensitive data, or senior management. While they cannot see the score itself, they can see the history of late payments and bankruptcies, which may influence hiring decisions.

Insurance Premiums

In many jurisdictions, auto and homeowners’ insurance companies use "credit-based insurance scores." Actuarial data suggests a correlation between credit health and insurance risk. Consequently, a lower credit score can lead to significantly higher insurance premiums, adding another layer of financial strain.

The Wealth Gap and Financial Mobility

Systemically, credit health plays a role in the widening wealth gap. Those with high scores have access to low-interest capital, allowing them to invest in real estate and equities. Conversely, those with low scores are often forced into the "subprime" market, where high interest rates and fees make it difficult to accumulate savings, creating a cycle of debt.

Conclusion: Building a Resilient Financial Future

Improving a credit score is not an overnight feat; it is a marathon of consistency and awareness. The path to a healthier profile is paved with simple, repeatable actions: paying every bill on time, keeping balances low, and limiting the frequency of new applications.

As Credit Awareness Month draws attention to these issues, the message from financial experts is clear: you are not your credit score, but your credit score dictates much of your financial reach. By utilizing tools like AnnualCreditReport.com and understanding the protections offered by the FCRA, consumers can take the driver’s seat in their financial lives. Whether you are rebuilding after a setback or fine-tuning a near-perfect score, the journey toward credit health is one of the most valuable investments an individual can make in their future.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute legal, financial, or credit advice. Readers should consult with professional advisors regarding their specific financial situations. This content is intended to foster credit awareness and encourage the responsible management of personal finances.