For the casual enthusiast browsing a local shop or a seasoned sommelier curating a high-end cellar, the price tag on a bottle of wine is often viewed as a reflection of origin, vintage, and prestige. However, buried within that retail price is a complex, often opaque layer of government levies that remain largely invisible to the consumer. As the wine industry continues to be a cornerstone of the American beverage market, the fiscal architecture supporting it—or, in some cases, burdening it—has come under increasing scrutiny.

In 2025 alone, the total amount of consumption taxes paid on wine in the United States is estimated to be a staggering $7.2 billion. This figure, while significant, is merely the tip of the iceberg in an economic landscape defined by inconsistent state policies, archaic categorical definitions, and an urgent need for regulatory modernization.

The Fiscal Landscape: A Patchwork of Levies

The taxation of wine in the United States is characterized by a "triple-threat" of financial obligations: federal excise taxes, state-level excise taxes, and, in some jurisdictions, state-managed monopolies that act as de facto tax collectors through artificial markups.

At the federal level, the Alcohol and Tobacco Tax and Trade Bureau (TTB) imposes a baseline excise tax. For standard 11 percent ABV (alcohol by volume) still wine, the federal rate sits at $1.07 per gallon. While this may seem straightforward, the reality is complicated by a tiered system of tax credits available to domestic producers based on annual production volumes, specifically designed to support smaller wineries.

However, the true complexity—and the primary source of frustration for industry analysts—lies at the state level. States typically position wine taxes as a middle ground between beer (often taxed lower) and distilled spirits (often taxed higher). Yet, this "middle-ground" logic often ignores the actual alcohol content of the product. When adjusted for ABV, the tax landscape shifts dramatically. Some states favor wine, while others punish it with rates that, on an alcohol-content basis, far exceed those of beer or spirits.

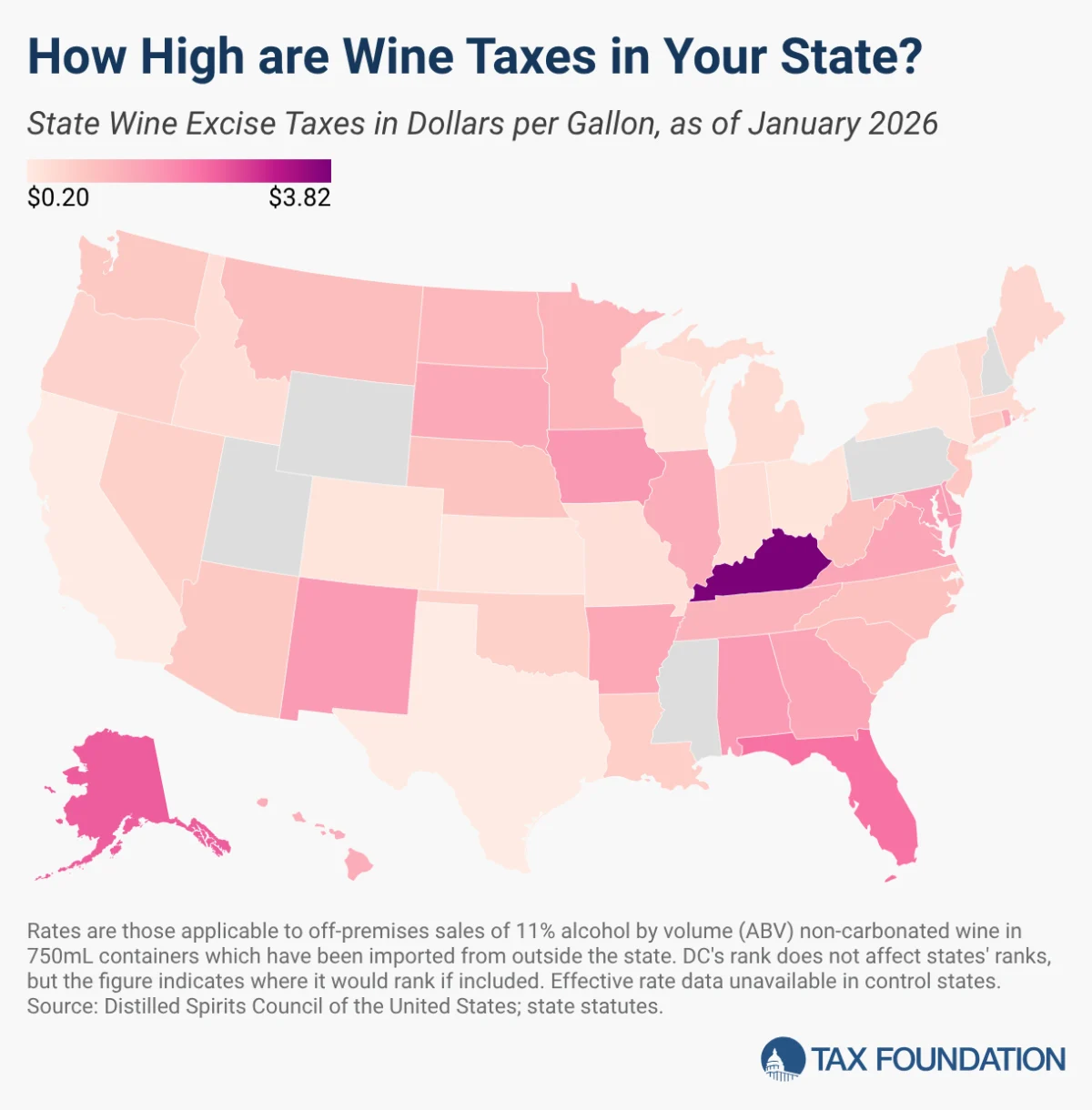

State-by-State Disparity

The geographical variance in wine taxation is stark. Kentucky currently holds the title for the most expensive tax environment for wine, levying an effective rate of $3.82 per gallon, compounded by a 10 percent wholesale tax. In contrast, California—the engine of the American wine industry and home to the globally recognized Napa Valley—maintains one of the lowest tax burdens in the nation at just $0.20 per gallon.

This vast chasm between $0.20 and $3.82 illustrates a lack of national uniformity that complicates logistics, pricing, and distribution for national wine brands. States like Alaska ($2.50 per gallon) and Florida ($2.25 per gallon) sit at the high end of the spectrum, while Texas ($0.204), Wisconsin ($0.25), and New York ($0.30) join California in the low-tax tier.

Chronology of Regulatory Challenges

The debate over alcohol taxation is not a modern phenomenon, but it has reached a boiling point in the 2020s. Following the legislative adjustments made in 2021, the industry has faced a shifting regulatory environment.

- Pre-2021: The industry operated under a relatively static tax environment, with minor adjustments to federal excise rates and standard state-level updates.

- 2021–2023: Significant legislative discussions began regarding the "modernization" of alcohol taxes. Experts pushed for a shift away from categorical taxation toward an ABV-based model.

- 2024–2025: Several states faced increased pressure to address the rise of "Ready-to-Drink" (RTD) wine cocktails. These products, which often blend wine with other ingredients, frequently fall into a legal gray area, leading to instances of "taxation by default"—where they are categorized as spirits due to their format, resulting in significantly higher tax rates than traditional wine.

The "Monopoly" Exception: When the State Becomes the Merchant

A critical obstacle in analyzing wine taxation is the existence of the "control states." In Mississippi, New Hampshire, Pennsylvania, Utah, and Wyoming, the government has established a monopoly over the sale of alcohol. In these jurisdictions, traditional excise tax rates are often secondary to the state’s ability to manipulate retail pricing directly.

In Utah, for instance, state statutes mandate a minimum markup of 88.5 percent on wine. Because the state sets the price, the "tax" is effectively baked into the shelf price, making it nearly impossible for the average consumer to isolate the cost of the government’s take versus the actual value of the wine. Similarly, Pennsylvania’s Liquor Control Board has broad authority to adjust markups, which has resulted in an environment where pricing is dictated by administrative policy rather than market demand.

Supporting Data: Subsidies and Special Interests

A notable feature of state wine taxation is the emergence of dedicated funds. In seven states—Colorado, Idaho, Iowa, Missouri, Oregon, Ohio, and Washington—a portion of the excise tax collected on all wine sales is earmarked for the support of the local wine industry. These funds support Wine Commissions and Agricultural Business Development initiatives.

While supporters argue that these funds are essential for fostering regional economic growth and promoting domestic viticulture, critics argue that this represents an unfair tax on the broader market to subsidize specific domestic interests. By taxing imports to pay for the marketing of local grapes, these states are engaging in a form of protectionism that distorts the national market.

Implications for the Future: The Call for Modernization

The current system of taxing wine is increasingly viewed by economists and industry advocates as "arcane." The rigid, categorical definitions of the past fail to account for the rapid innovation currently reshaping the beverage industry.

The ABV Solution

The most widely supported reform is the transition to an ABV-based tax system. Under this model, the tax rate would be determined solely by the amount of alcohol in the container, regardless of whether the product is a traditional Chardonnay, a sparkling wine, or a wine-based cocktail.

Why this matters:

- Neutrality: It removes the bias against specific product categories, ensuring that innovation in product formulation is not stifled by punitive tax classifications.

- Simplicity: It streamlines the administrative burden on both regulators and producers, reducing the compliance costs that currently disproportionately affect smaller wineries.

- Future-Proofing: An ABV-based system would naturally accommodate new product types as they emerge, preventing the need for frequent legislative overhauls.

Risks of the Status Quo

The reliance on ad quantum (volume-based) taxes poses a long-term risk to government revenues. Because these taxes are often fixed, they lose their real value over time due to inflation and currency debasement. Conversely, ad valorem (value-based) taxes—while more resistant to inflation—are highly susceptible to market volatility. When consumer trends shift away from high-end wine toward lower-cost alternatives, or when international trade disputes trigger retaliatory tariffs, the revenue generated from ad valorem taxes can collapse unexpectedly.

Conclusion: A Call for Transparency

The $7.2 billion the American public will pay in wine taxes in 2025 is more than just a line item in a federal or state budget; it is an economic force that shapes what we drink, what we pay, and how the industry evolves.

As policymakers look toward the future, the primary challenge will be to move away from the rigid, historical categorizations that have defined alcohol policy for decades. By embracing a more modern, neutral, and transparent tax framework based on alcohol content, the United States could foster a more competitive and innovative wine industry—one where the price of a bottle reflects the quality of the craft rather than the complexity of the tax code.

Ultimately, whether you are a casual enjoyer or a professional in the field, the movement toward "tax modernization" is not just about reducing costs; it is about ensuring that the American wine market remains a fair, efficient, and dynamic space for both producers and consumers for years to come.