As the mercury climbs and Americans head outdoors for the long-awaited summer season, the ritual of cracking open a cold beer remains a staple of social life. However, for those perusing the cooler aisles or settling into a neighborhood pub, there is a hidden element at play that significantly influences the price of every pour. While the cost of hops, barley, water, and yeast are the foundational elements of brewing, the single most expensive ingredient in your beer is not a raw material at all—it is the tax burden.

The Anatomy of the Beer Tax

The economics of the American brewing industry are far more intricate than they appear to the average consumer. According to data from the Tax Foundation and the Beer Institute, the cumulative tax burden on beer can account for as much as 40.8 percent of the final retail price. To put this in perspective, for a significant portion of the beer market, the total tax impact—comprising federal excise taxes, state-level levies, and local assessments—often exceeds the combined costs of labor and raw materials.

This burden is rarely transparent. Unlike standard sales taxes, which are clearly itemized at the bottom of a retail receipt, beer taxes are typically "baked in" to the final price. These are largely excise taxes—levies imposed on specific goods rather than broad consumption—collected at the wholesale or manufacturing level. Consequently, the consumer remains largely oblivious to the fact that nearly half of their purchase price is essentially a transfer payment to local, state, and federal treasuries.

A Chronology of Regulation and Revenue

The current system of alcohol taxation in the United States is a patchwork quilt of post-Prohibition-era policies and modern fiscal requirements. Historically, alcohol has been viewed by policymakers as an ideal "sin tax" target: it is a non-essential good with relatively inelastic demand, making it a reliable, if sometimes volatile, source of government revenue.

- The Post-Repeal Framework: Following the ratification of the 21st Amendment in 1933, the federal government established a robust system of excise taxation on alcoholic beverages. This was designed not only to raise funds to help stabilize the national budget during the Great Depression but also to establish a regulatory framework that allowed states to control the distribution and sale of alcohol within their own borders.

- The Rise of Modern Excise Taxes: Throughout the mid-to-late 20th century, states began to layer their own specific excise taxes on top of federal rates. These were initially uniform but grew increasingly complex as states looked for ways to address budget deficits without raising broad-based income or property taxes.

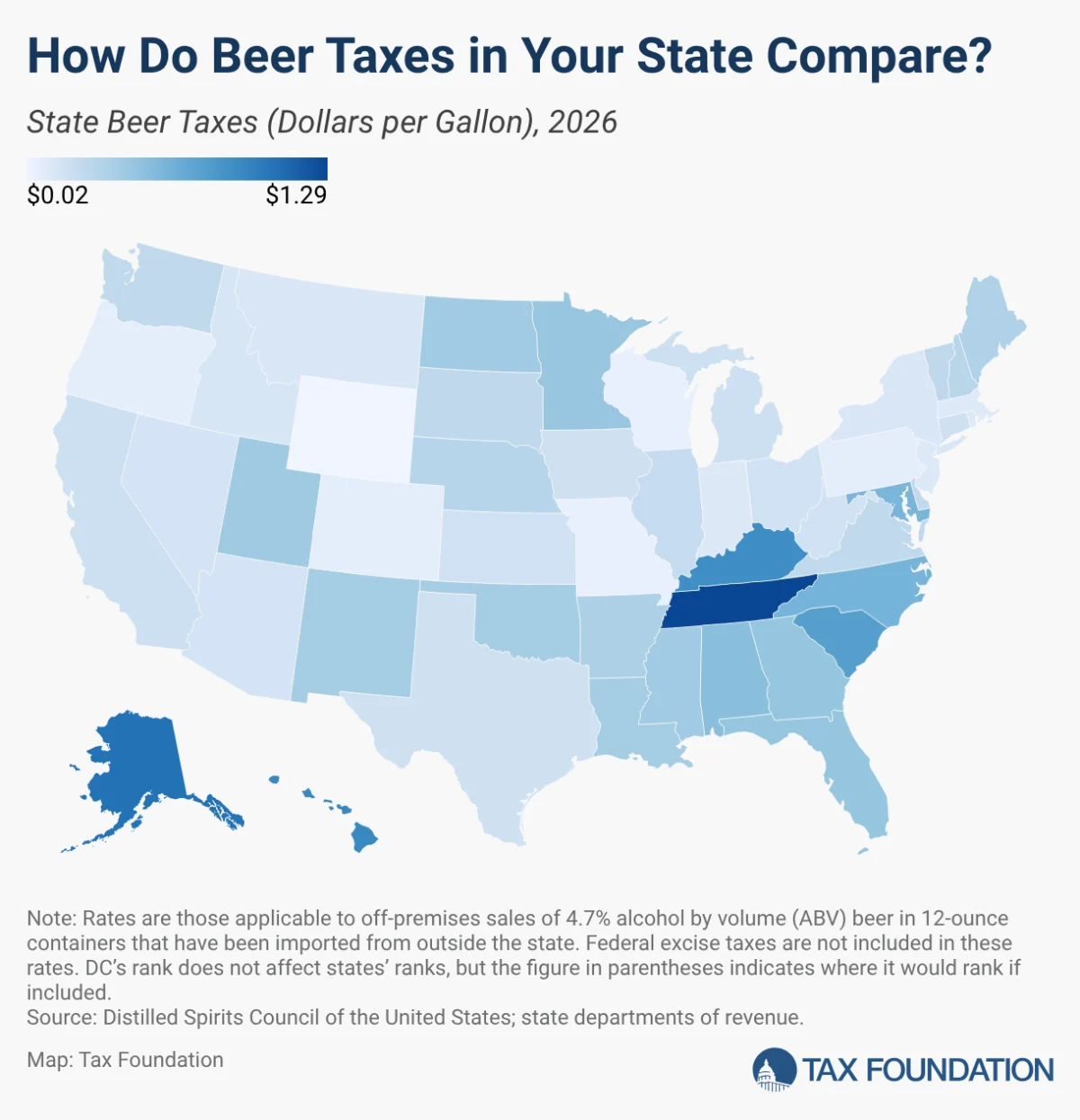

- Recent Legislative Shifts (2025–2026): The landscape remains in flux. For instance, Missouri recently took steps to bolster its local brewing economy by signing legislation that reduced the tax rate on beer manufactured within the state to just $0.02 per gallon. Conversely, other jurisdictions continue to tighten regulations, with some states introducing "tiered" taxation based on alcohol-by-volume (ABV) thresholds or even the physical size of the container.

Data Analysis: The Great Geographical Divide

The "cost of a cold one" varies wildly depending on one’s zip code. The U.S. federal excise tax serves as a baseline, ranging from $0.113 per gallon for small domestic brewers (producing under 60,000 barrels) to $0.581 per gallon for imports. However, the true variance emerges at the state level.

The High-Tax Leaders

The states with the highest tax burden per gallon represent a mix of high-cost-of-living regions and states with aggressive revenue-generation models.

- Tennessee: Leading the nation with a burden of $1.287 per gallon.

- Alaska: Following closely at $1.07 per gallon.

- Hawaii: Rounding out the top three at $0.93 per gallon.

The Low-Tax Havens

At the other end of the spectrum, states like Wyoming ($0.019 per gallon), Missouri ($0.06 per gallon), and Wisconsin ($0.065 per gallon) maintain significantly lower tax environments, often reflecting a legislative priority to keep the industry competitive and accessible.

It is important to note that these figures represent statewide averages. In reality, the complexity is compounded by local municipal taxes. For example, the Municipality of Anchorage, Alaska, imposes an additional 5 percent local sales tax on alcohol, while Alabama and Georgia implement uniform local taxes that add roughly 50 cents per gallon, independent of state-level mandates.

Regulatory Complexity and Industry Challenges

Beyond the simple per-gallon tax, the industry is governed by an "arcane categorical system." Alcohol is taxed by classification—beer, wine, and spirits—rather than by the actual alcohol content. This leads to profound inefficiencies.

For example, in Idaho, the tax framework changes drastically once a beverage crosses the 5 percent ABV threshold. Beer exceeding this limit is statutorily reclassified and taxed as wine, effectively tripling the tax burden from $0.15 to $0.45 per gallon. This creates a regulatory "cliff" that discourages innovation, as brewers must navigate arbitrary thresholds that do not account for modern brewing techniques or changing consumer preferences.

Furthermore, the industry is currently grappling with shifting consumer behaviors. Younger generations are increasingly pivoting toward low- or no-alcohol alternatives. When combined with the rising costs of tariffs on imported brewing components and the administrative burden of complying with 50 different state regulatory frameworks, the traditional beer industry is facing a period of significant contraction.

Implications for Policy and the Future of Brewing

The reliance on beer as a consistent revenue stream presents a long-term danger for state budgets. As the industry faces downward pressure from shifting demographics and the "premiumization" of the beverage market, revenue generated from traditional ad quantum (quantity-based) taxes often fails to keep pace with inflation.

The Case for Modernization

Industry experts and policy analysts, including those at the Tax Foundation, argue that the current system is ripe for reform. The primary recommendation is a transition toward a neutral, ABV-based tax system. By taxing alcohol content rather than arbitrary categories, policymakers could:

- Simplify Compliance: Reducing the administrative cost for distributors and retailers who currently manage thousands of different tax codes.

- Increase Neutrality: Ensuring that all alcoholic beverages are taxed equitably based on their strength, rather than their historical classification.

- Foster Innovation: Allowing brewers to experiment with new products—such as hard seltzers or non-traditional fermented beverages—without the fear of falling into a punitive tax bracket.

The Economic Ripple Effect

Policymakers must also consider the economic footprint of the beer industry. From the hop farms of the Pacific Northwest to the bottling plants in the Midwest and the craft taprooms in urban centers, the beer industry supports hundreds of thousands of jobs. When taxes are layered excessively, it can suppress retail demand, which in turn reduces the demand for raw materials and labor.

As the 2026 fiscal cycle approaches, state legislatures will likely face pressure to address these budget gaps. While the temptation to raise excise taxes on alcohol remains a perennial favorite of those looking to balance budgets, the diminishing returns and the complexity of the current system suggest that the old methods may no longer be sustainable.

Conclusion: A Toast to Transparency

The complexity of the American beer tax landscape is a testament to how far a simple, historic beverage has been integrated into the machinery of government finance. While the average consumer may never see the $1.287 tax per gallon in Tennessee or the local surcharge in Anchorage on their receipt, it remains a tangible factor in the price of their pint.

As the industry continues to evolve in the face of changing consumer tastes and economic pressures, the debate over how we tax our most cherished beverages will likely intensify. For the consumer, it serves as a reminder that every purchase is also a policy transaction. For the policymaker, the challenge lies in moving away from archaic, categorical structures toward a more rational, transparent, and modern framework that recognizes the realities of the 21st-century market. Whether through simplified ABV-based taxing or a reduction in the reliance on excise revenue, the path toward a more efficient system is essential for both the economic health of the industry and the wallet of the American beer drinker.