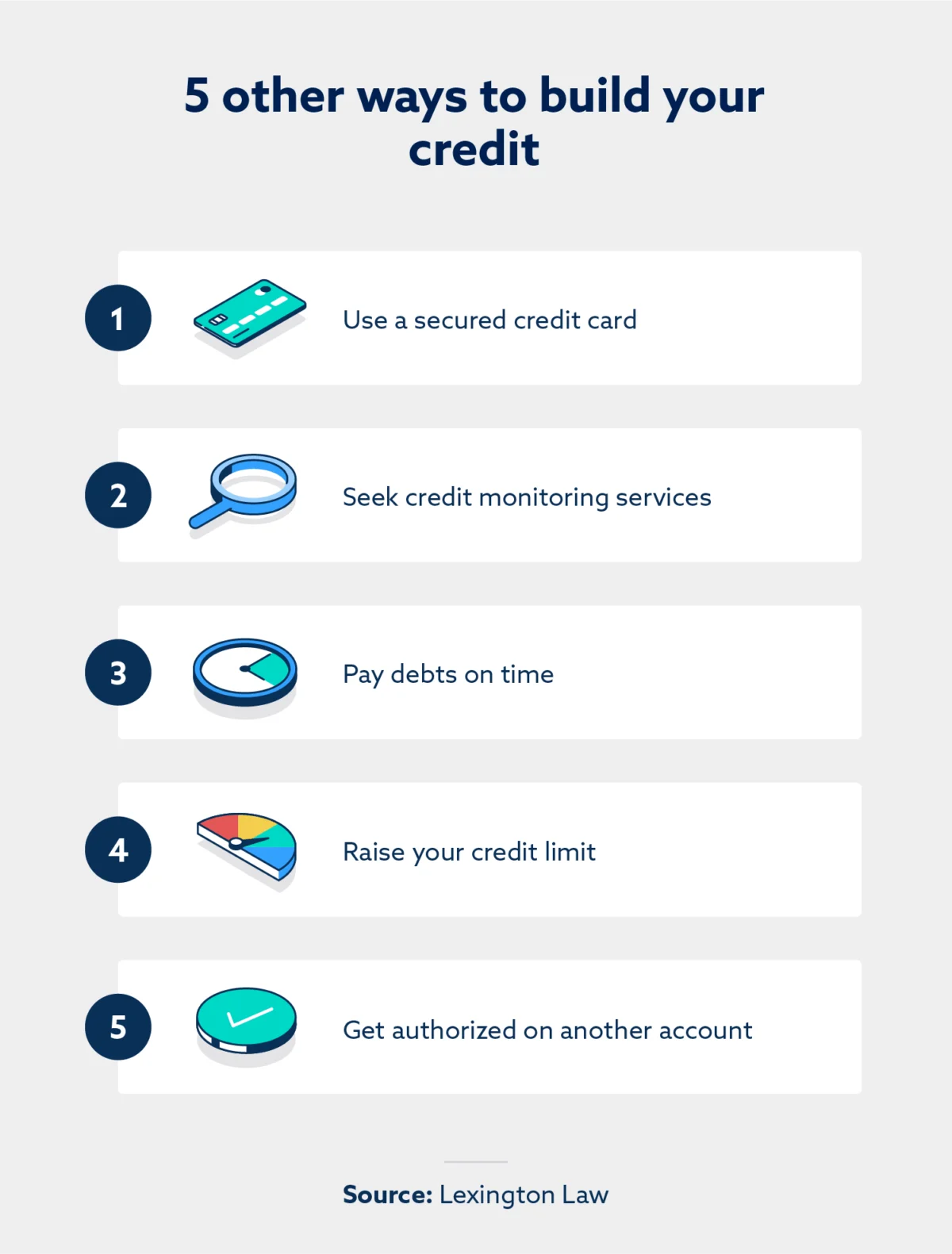

")

In an era defined by economic fluctuations, the American credit score has evolved from a mere financial metric into a definitive marker of social and economic mobility. For millions of Americans, a credit score is the gatekeeper to homeownership, reliable transportation, and even employment opportunities. However, when financial setbacks occur—ranging from medical emergencies to systemic economic downturns—credit scores often bear the brunt of the impact.

The process of rebuilding credit is frequently shrouded in mystery and clouded by the emotional weight of perceived failure. Yet, legal experts and financial advocates, including the team at Lexington Law, emphasize a crucial reality: credit setbacks are not permanent, and the path to recovery is paved with legal rights and systematic habits. This article explores the mechanics of credit restoration, the legal protections afforded to consumers, and the strategic steps necessary to reclaim financial agency.

Main Facts: The Current State of Consumer Credit

The landscape of consumer credit in the United States is both vast and prone to error. According to data from the Federal Trade Commission (FTC), a significant percentage of consumer credit reports contain inaccuracies that could lead to higher interest rates or denied loan applications.

The Prevalence of Reporting Errors

Recent studies suggest that as many as one in five consumers has a verifiable error on at least one of their three major credit reports (Equifax, Experian, and TransUnion). These errors range from "mixed files"—where two individuals with similar names have their data merged—to "zombie debts" that should have aged off the report but remain active.

The Impact of Credit Inequity

A low credit score is not merely a number; it is a financial tax. A consumer with a "fair" credit score (580–669) may pay tens of thousands of dollars more in interest over the life of a mortgage compared to a consumer with a "very good" score (740–799). Rebuilding credit confidence is, therefore, a matter of significant long-term wealth preservation.

The Legal Right to Accuracy

Under the Fair Credit Reporting Act (FCRA), consumers possess the legal right to an accurate, fair, and substantiated credit report. This federal law empowers individuals to challenge any information that is inaccurate, outdated, or unverifiable. Understanding this legal framework is the first step in transitioning from a passive victim of financial circumstances to an active participant in credit management.

Chronology: The Lifecycle of Credit Reconstruction

Rebuilding credit is not an overnight event; it is a chronological progression that requires persistence. Financial experts typically break down the recovery timeline into four distinct phases.

Phase 1: The Audit (Months 1–2)

The journey begins with a comprehensive audit of one’s current standing. Consumers are entitled to a free credit report from each of the three bureaus via AnnualCreditReport.com. During this phase, the goal is to identify every negative item and categorize them:

- Inaccuracies: Accounts that do not belong to the consumer or incorrect balances.

- Outdated Items: Negative marks older than seven years (or ten for certain bankruptcies).

- Legitimate Negatives: On-time payments that were missed or high balances that are accurately reported.

Phase 2: The Dispute and Challenge Process (Months 2–6)

Once errors are identified, the formal dispute process begins. Consumers (or their legal representatives) submit challenges to the credit bureaus. By law, bureaus typically have 30 to 45 days to investigate. If the bureau cannot verify the accuracy of the disputed item, they are legally obligated to remove it. This phase often requires multiple rounds of correspondence to ensure that corrected information remains corrected.

Phase 3: The Habit Reinforcement Phase (Months 6–24)

While the dispute process addresses the past, habit reinforcement secures the future. This period focuses on the two most significant factors in a FICO score: payment history and credit utilization.

- Payment History: Establishing a streak of 100% on-time payments.

- Utilization Management: Reducing credit card balances to below 30% (ideally below 10%) of the total available limit.

Phase 4: The Maturity Phase (Year 2 to Year 7)

As time passes, the "weight" of old negative items diminishes. Credit scoring models are weighted toward recent behavior. A three-year-old late payment has significantly less impact than a three-month-old one. By the seventh year, most negative marks fall off entirely, leaving a "clean slate" supported by years of positive habits.

Supporting Data: The Mechanics of the Score

To rebuild credit effectively, one must understand the mathematical components that dictate the score. The FICO score, used by 90% of top lenders, is calculated based on five key categories of data.

1. Payment History (35%)

This is the single most important factor. Even one 30-day late payment can cause a score to drop by 60 to 100 points, depending on the consumer’s starting score. Conversely, a consistent history of on-time payments is the fastest way to demonstrate reliability to lenders.

2. Amounts Owed / Credit Utilization (30%)

Utilization is calculated by dividing total credit card balances by total credit limits. For example, a consumer with a $1,000 limit and a $900 balance has a 90% utilization rate, which signals high risk to lenders. Lowering this ratio is often the quickest way to see a "jump" in a credit score because, unlike payment history, utilization has no "memory"—once the balance is paid down, the score benefits almost immediately in the next reporting cycle.

3. Length of Credit History (15%)

The age of your oldest account, the age of your newest account, and the average age of all accounts contribute to this metric. This is why experts often advise against closing old credit card accounts, even if they are not being used, as they provide the "anchor" for a long credit history.

4. Credit Mix (10%)

Lenders like to see that a consumer can handle different types of credit, such as revolving credit (credit cards) and installment loans (auto loans, mortgages, or student loans).

5. New Credit (10%)

Opening multiple new accounts in a short period represents a risk. Each "hard inquiry" can result in a small, temporary dip in the score.

Official Responses and Expert Perspectives

The credit repair industry has faced scrutiny in the past, leading to the implementation of the Credit Repair Organizations Act (CROA). Professional firms like Lexington Law operate within these strict regulatory frameworks to provide consumer advocacy.

The Role of Professional Advocacy

Legal experts argue that while consumers can manage the dispute process themselves, the complexity of the bureaus’ automated systems often makes professional intervention more effective. "The credit reporting system is massive and largely automated," says a representative of Lexington Law. "Our role is to ensure that the consumer’s voice isn’t lost in the algorithm. We advocate for the consumer’s right to a fair report by holding bureaus and creditors accountable to the standards set by the FCRA."

The Shift from Shame to Strategy

Psychological experts in financial wellness note that the greatest barrier to credit rebuilding is often emotional. Shame regarding past financial mistakes can lead to "ostriching"—the tendency to ignore bills and credit reports. Experts suggest that viewing credit as a "system" rather than a "moral scorecard" allows consumers to detach their self-worth from their score and focus on the strategic steps required for improvement.

Implications: The Long-Term Benefits of Credit Confidence

The implications of a successful credit rebuild extend far beyond the ability to secure a loan. It represents a fundamental shift in one’s financial trajectory and quality of life.

Economic Mobility and Wealth Building

A healthy credit score is a prerequisite for building generational wealth. It allows for the purchase of appreciating assets (homes) at lower costs. Furthermore, in many states, insurance companies use credit-based insurance scores to determine premiums for auto and homeowners’ insurance. A higher score can literally save a household thousands of dollars in annual expenses.

Employment and Security

In certain industries—particularly finance, government, and high-level management—employers may conduct credit checks as part of the background screening process. While they do not see the score itself, they see the credit report. A history of financial responsibility is often viewed as a proxy for reliability and trustworthiness in sensitive roles.

Mental Health and Peace of Mind

Financial stress is a leading cause of anxiety and marital discord. Rebuilding credit confidence provides a sense of control over one’s future. Knowing that an unexpected car repair or medical bill can be managed without a "cascading failure" of one’s financial life provides a level of psychological security that is difficult to quantify but essential for well-being.

The Bottom Line

The journey to rebuilding credit is a marathon, not a sprint. It requires a dual-pronged approach: correcting the inaccuracies of the past through legal disputes and securing the future through disciplined financial habits. As the economy continues to evolve, the ability to navigate the credit system remains one of the most vital skills for the modern consumer.

Whether through self-education or professional partnership, the first step remains the same: facing the report. By understanding their rights under the FCRA and committing to small, consistent wins, any consumer can turn the page on a difficult financial chapter and begin writing a new story of stability and success.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute legal, financial, or credit advice. Rebuilding credit involves various factors, and results may vary based on individual circumstances. For specific legal or financial concerns, consumers should consult with qualified professionals.