Across the European continent, the Value Added Tax (VAT) remains the primary engine of government revenue. Yet, embedded within the complex architecture of these tax systems is a crucial policy lever: the VAT registration threshold. These thresholds, designed to spare small enterprises from the burdensome administrative costs of compliance, have become a focal point of debate among economists and policymakers. As nations grapple with the trade-off between supporting small business growth and maintaining tax neutrality, the landscape of VAT exemption is shifting rapidly, revealing deep-seated economic distortions that may be hindering long-term productivity.

The Landscape of Exemption: Nominal vs. Real Value

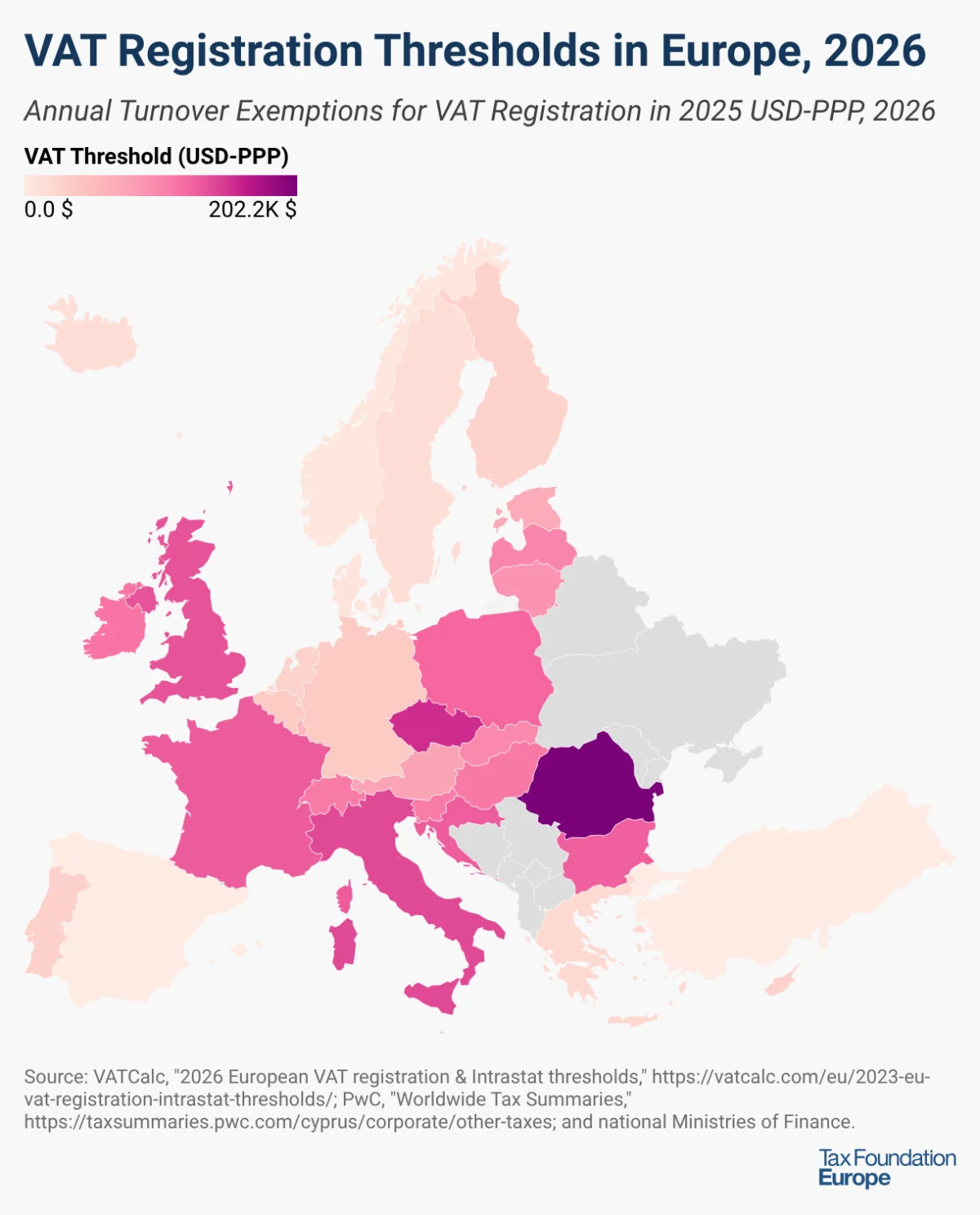

When examining the 32 major European nations, the disparity in how countries define "small business" is stark. In nominal terms, Switzerland leads the pack with the highest absolute VAT exemption threshold, set at CHF 100,000 (approximately €106,724). Following closely are the United Kingdom and France, with thresholds of £90,000 (€105,043) and €87,000, respectively.

However, looking at nominal figures alone provides an incomplete picture. The economic utility of these thresholds is heavily influenced by the cost of living and local price levels. To understand the true impact, economists use Purchasing Power Parity (PPP) to adjust these figures. When viewed through the lens of PPP, the leaderboard shifts significantly. Romania currently boasts the highest adjusted threshold at RON 395,000 (roughly $202,206), followed by the Czech Republic (CZK 2,000,000 or $155,039) and Italy (€85,000 or $140,246).

At the other end of the spectrum, some nations have opted for total inclusion. Spain and Turkey stand as the only countries in the cohort that do not maintain a VAT threshold at all. In these jurisdictions, every business—regardless of turnover—is required to enroll in the VAT system, ensuring a uniform tax base but placing a heavier administrative burden on micro-enterprises.

A Chronology of Recent Policy Shifts

The last 24 months have seen a noticeable trend toward raising thresholds, as governments attempt to provide relief to small businesses facing inflationary pressures.

- September 2025: Romania took decisive action to support its small business sector by increasing its VAT registration threshold from RON 300,000 to RON 395,000. This move effectively shielded a larger segment of the economy from the compliance costs associated with VAT.

- January 2026: Hungary initiated a multi-year plan to raise its threshold. The initial hike moved the limit from HUF 18 million to 20 million (€45,250 to €50,280). This policy is part of a broader fiscal strategy, with a further increase to HUF 22 million (€55,310) slated for 2027.

- January 2026: Poland followed suit, adjusting its threshold from PLN 200,000 to 240,000 (€47,170 to €56,610), reflecting a concerted effort to simplify the tax environment for nascent firms.

- April 2026: The Belgian parliament passed legislation to increase the VAT exemption threshold from €25,000 to €30,000. While the legislative approval was a significant milestone, the administrative implementation of the policy remains pending, highlighting the bureaucratic delays that often accompany tax reform.

The "Notch" Effect: Economic Distortions and Bunching

While the intent behind these thresholds—reducing administrative and compliance costs—is benevolent, the economic reality is far more complex. These thresholds create what economists call a "notch," or a tax cliff.

The mechanism is simple but destructive: a firm that generates a turnover one euro above the threshold suddenly becomes liable for VAT on its entire value-added, rather than just the marginal amount exceeding the threshold. This creates a powerful, artificial incentive for firms to remain small.

Empirical research has consistently identified "bunching" behavior, where businesses artificially cap their revenue or underreport their earnings specifically to stay below the tax line. This leads to a misallocation of resources. By favoring smaller, tax-advantaged firms over larger, more productive competitors, the system inadvertently discourages companies from scaling up. When a firm avoids growth to escape a tax liability, it fails to realize economies of scale, ultimately dampening aggregate national productivity.

The Czech Republic serves as a poignant case study. With one of the highest PPP-adjusted thresholds in Europe, the nation has seen a distinct "spike" in the distribution of its corporations just below the cutoff point. As the government has periodically raised the threshold, the "bunching" point has shifted in tandem, confirming that firms are actively tailoring their business operations to avoid the tax, rather than maximizing their economic potential.

Implications for Policymakers

The debate over VAT thresholds forces policymakers to reconcile two competing goals: simplicity and efficiency.

1. The Cost of Compliance

Proponents of high thresholds argue that for micro-enterprises, the administrative cost of VAT registration—which involves filing, record-keeping, and dealing with tax authorities—is disproportionately high compared to the revenue collected. For a sole proprietor, these costs can act as a significant barrier to entry, stifling entrepreneurship.

2. The Erosion of the Tax Base

Conversely, the fiscal implications of high thresholds cannot be ignored. Every enterprise exempted from VAT represents a leakage in the tax base. As more firms stay below the "notch," the overall revenue collected by the state diminishes, potentially forcing governments to increase VAT rates on compliant businesses to compensate for the lost revenue.

3. Neutrality and Competitiveness

The most significant danger, however, is the distortion of the market. When the tax code creates a "size penalty," it penalizes efficiency. A larger firm that could provide goods or services at a lower cost might be pushed out of the market by a smaller, less efficient competitor that enjoys a VAT-free advantage. This prevents the market from naturally weeding out less productive firms, leading to a stagnant business ecosystem.

Toward a Solution: The Case for Reform

The empirical evidence suggests that high VAT thresholds, while politically popular, come with a high price tag in the form of reduced economic dynamism. The "bunching" behavior observed in countries like the Czech Republic suggests that the current model is effectively putting a ceiling on the growth of the SME sector.

To mitigate these costs, tax experts and international organizations are increasingly suggesting that policymakers should look toward "tapering" or phasing out thresholds entirely. By gradually introducing VAT obligations as a firm grows—rather than hitting them with a sudden cliff—governments can eliminate the incentive for firms to remain artificially small.

Furthermore, digital transformation offers a path forward. With the advent of e-invoicing and automated tax software, the administrative burden of VAT compliance is falling rapidly. As technology makes it easier and cheaper to manage tax obligations, the historical justification for high thresholds—the "administrative burden"—is weakening.

Ultimately, if European nations are to foster a more competitive and productive business environment, they must move away from policies that incentivize stagnation. Eliminating or significantly lowering VAT thresholds, while perhaps politically challenging in the short term, is a necessary step toward ensuring that tax policy supports, rather than suppresses, the natural evolution of business.

Conclusion

As Europe navigates a period of economic transition, the management of VAT registration thresholds will remain a critical issue. While the recent waves of increases in Hungary, Poland, Romania, and Belgium demonstrate a desire to support small businesses, they also underscore the need for a more sophisticated approach. By understanding the "notch" effect and the long-term dangers of bunching, policymakers can begin to design tax systems that offer genuine support to small firms without creating the structural distortions that hinder the broader economy. The future of European growth depends not on protecting small firms from tax, but on creating an environment where they have every incentive to grow into the giants of tomorrow.