Across the European continent, the Value Added Tax (VAT) serves as the primary engine for government revenue, yet its application remains far from uniform. A critical component of this tax architecture is the registration threshold—a revenue ceiling below which small businesses are exempt from charging VAT. While these thresholds are often framed as relief for small enterprises, a comprehensive analysis reveals a complex landscape of economic distortion, administrative burden, and unintended behavioral consequences.

The Landscape of VAT Exemption: A Continental Comparison

When examining the absolute monetary value of VAT exemption thresholds across 32 major European nations, Switzerland stands in a league of its own. With a threshold set at CHF 100,000 (€106,724), the Swiss approach offers the most generous cushion for small businesses to operate without the administrative overhead of the VAT system. Following closely behind are the United Kingdom and France, which maintain thresholds of £90,000 (€105,043) and €87,000, respectively.

However, the continental picture is defined as much by its outliers as by its standard-bearers. Spain and Turkey represent the most stringent end of the spectrum, serving as the only two countries among the group that do not implement a threshold at all. In these jurisdictions, every business—regardless of its annual turnover—is mandated to enroll in the VAT system from its inception. This total-coverage approach removes the "tax cliff" inherent in other systems but places a significantly higher compliance burden on micro-entrepreneurs and startups.

The PPP Adjustment: Economic Weight vs. Nominal Value

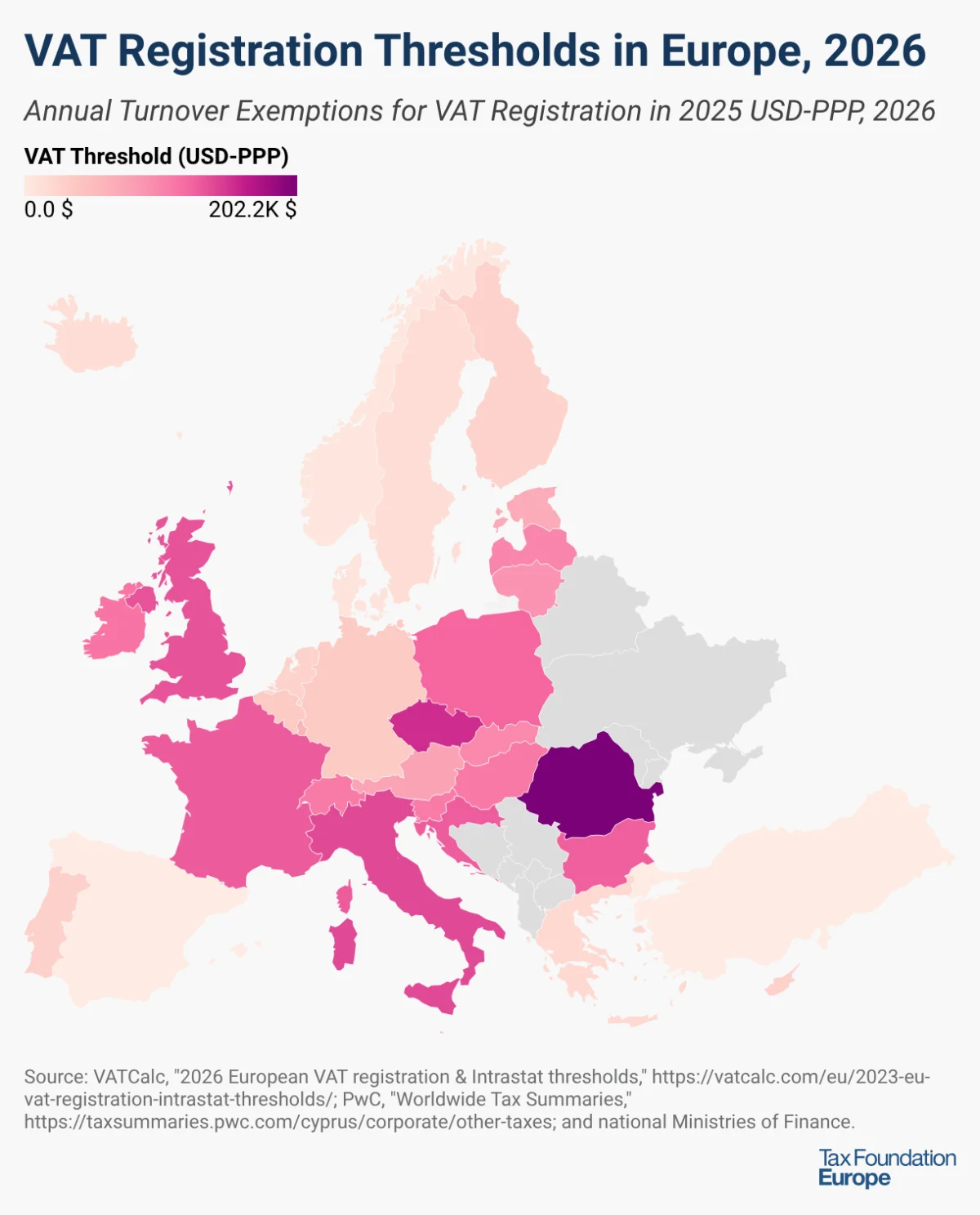

Nominal figures often mislead when comparing the fiscal reality across borders with vastly different price levels. A threshold of €50,000 provides vastly different "economic space" in Romania than it does in Luxembourg. When analysts adjust for Purchasing Power Parity (PPP)—which levels the playing field by accounting for the cost of living and business operations—the leaderboard shifts dramatically.

Romania emerges as the clear leader in this metric, with a PPP-adjusted threshold equivalent to $202,206 (RON 395,000). This suggests that Romanian policymakers have placed a significant premium on shielding the smallest economic actors from the complexities of VAT compliance. The Czech Republic follows with an adjusted threshold of $155,039 (CZK 2,000,000), and Italy rounds out the top tier with a PPP-adjusted value of $140,246 (€85,000). These figures highlight that the true "value" of a tax exemption is not found in a bank statement, but in the relative purchasing power of the currency within the domestic market.

Chronology of Recent Regulatory Shifts

The last 18 months have witnessed a flurry of legislative activity as European governments reassess their VAT strategies in the face of inflationary pressures and evolving digital economies.

- September 2025: Romania took decisive action by raising its threshold from RON 300,000 to RON 395,000, effectively modernizing its support for small businesses to align with current economic conditions.

- January 2026: Poland implemented a significant hike, moving its threshold from PLN 200,000 to 240,000. This shift reflected a broader regional trend of easing administrative burdens on the SME sector.

- January 2026: Hungary initiated the first phase of a multi-year plan to increase its exemption limit, moving from HUF 18 million to 20 million.

- April 2026: The Belgian Parliament approved a legislative push to raise its threshold from €25,000 to €30,000. As of mid-2026, the final implementation protocols are currently pending, reflecting the often-lengthy bureaucratic process of tax reform.

- Looking Ahead (2027): Hungary is scheduled to continue its trajectory, with a further increase to HUF 22 million already codified in national policy.

The Economic Implications: Efficiency vs. Distortion

The existence of a VAT threshold is a classic example of a "second-best" policy solution. While the intent is to reduce the administrative and compliance costs for small firms—allowing them to focus on growth rather than tax reporting—the practice introduces significant market distortions.

The "Notch" Effect and Business Behavior

The most severe structural issue with VAT thresholds is the creation of a "notch," or tax cliff. Because the threshold is a binary cutoff, a firm that earns one euro above the limit is suddenly liable for VAT on its entire value-added, rather than just the marginal amount exceeding the threshold.

This creates a perverse incentive structure. Empirical evidence, particularly from the Czech Republic, demonstrates a phenomenon known as "bunching." Researchers have observed a sharp spike in the number of corporations with turnover just below the statutory limit. When the government raises the threshold, the "bunching" point shifts in tandem. This indicates that businesses are not merely growing organically; they are actively managing their turnover, underreporting income, or scaling back their operations to remain safely beneath the threshold.

The Productivity Trap

Beyond the individual firm, these thresholds can stifle aggregate economic productivity. By effectively subsidizing smaller firms, the tax code can inadvertently disadvantage larger, more efficient competitors. When tax-advantaged micro-enterprises are protected from the competitive rigors of the VAT system, they may lack the incentive to scale, innovate, or adopt more efficient business models. This results in a market crowded with "lifestyle" businesses that are artificially kept small by the tax code, potentially preventing the emergence of larger, more productive firms that could drive national GDP growth.

Official Perspectives and Policy Recommendations

Policymakers face a perennial dilemma: how to balance the need for tax revenue with the desire to foster an entrepreneurial environment. The administrative cost of collecting VAT from a business with minimal revenue can often exceed the actual tax collected, making a threshold a rational administrative tool. However, the economic cost of market distortion is a growing concern for international fiscal bodies.

The consensus among tax experts and economic researchers is increasingly leaning toward the reduction or elimination of these thresholds. By narrowing the gap or moving toward a sliding scale, governments could theoretically mitigate the "notch" effect.

Addressing the Compliance Gap

The primary argument for maintaining thresholds remains the "compliance gap." If thousands of micro-enterprises were forced into the VAT system, the cost of auditing, monitoring, and processing these returns would be immense. Modern digital reporting, such as real-time invoicing and automated tax software, is being presented as the solution. By lowering the cost of compliance through technology, governments could theoretically eliminate the need for high thresholds without placing an undue burden on small business owners.

Conclusion: The Future of VAT Strategy

As Europe navigates the complexities of the mid-2020s, the VAT threshold debate remains a focal point of tax policy. The recent wave of increases in Poland, Hungary, Romania, and Belgium demonstrates that for many, the immediate political priority is providing relief to small businesses struggling with rising costs.

However, as the data from the Czech Republic and other markets show, these reliefs come with long-term economic trade-offs. The "bunching" behavior is a clear signal that tax thresholds—while intended to help—can become a ceiling for growth. Moving forward, the most effective tax regimes will likely be those that transition away from blunt, high-threshold exemptions in favor of digital-first compliance tools that allow businesses of all sizes to participate in the economy without creating artificial barriers to growth.

Ultimately, the goal for European policymakers must be to design a system where tax compliance is a seamless background function, rather than a strategic factor in a business’s decision to grow. Whether through the adoption of more advanced digital systems or the gradual lowering of thresholds to remove "cliffs," the objective remains the same: a more neutral, efficient, and transparent tax landscape.