In the evolving financial landscape of 2026, a credit score is no longer merely a reflection of past borrowing; it is a dynamic digital asset that dictates a consumer’s access to the modern economy. As interest rates remain a pivotal factor in household wealth, the difference between a "good" and "excellent" credit score can translate into hundreds of thousands of dollars in savings over a lifetime. Whether a consumer is entering the market for the first time or rehabilitating a damaged profile, the methodologies for building credit have shifted from slow, passive waiting to proactive, data-driven management.

Main Facts: The Credit Ecosystem in 2026

The contemporary credit scoring model remains dominated by two primary entities: FICO® and VantageScore®. Both utilize a scale ranging from 300 to 850, where higher numbers signify lower risk to lenders. However, the criteria for achieving these scores have become more nuanced.

In 2026, lenders are increasingly looking beyond simple payment tallies. They are evaluating "trended data"—how a consumer manages their balances over time rather than a single snapshot in a month. Despite these technological shifts, the foundational pillars of credit remain:

- Payment History: Constituting roughly 35% of a FICO score, this remains the single most influential factor.

- Credit Utilization: The ratio of outstanding balances to total available credit (ideally kept below 30%).

- Credit Age: The longevity of accounts, which provides a historical context for financial behavior.

- Credit Mix: The diversity of account types, including revolving (credit cards) and installment (loans).

The democratization of credit reporting has also reached a zenith, with non-traditional data—such as rent and utility payments—now playing a central role in establishing scores for "credit-invisible" individuals.

Chronology: The Evolution of Credit Building

To understand the current strategies, one must look at the timeline of how credit reporting has transitioned from a closed-door banking secret to a transparent, consumer-managed process.

The Traditional Era (Pre-2010s)

Credit building was a slow process. Consumers typically started with a small personal loan or a "gas card." Information flowed one way: from the bank to the bureau. Consumers often didn’t know their scores until they were rejected for a loan.

The Transparency Revolution (2010s – 2020)

The introduction of free credit monitoring apps and the FICO Open Access program allowed consumers to see their scores in real-time. Secured credit cards became the primary tool for rebuilding, and the Consumer Financial Protection Bureau (CFPB) began stricter oversight of credit reporting inaccuracies.

The Fintech & Alternative Data Era (2021 – 2025)

The industry saw a surge in "credit-builder" products. Companies began allowing consumers to self-report rent and streaming service payments. This period marked the shift from "waiting for credit to grow" to "actively manufacturing credit" through specialized financial products.

The Integrated Landscape (2026)

Today, credit building is an integrated part of daily financial life. Apps, legal services, and banking platforms work in tandem to update scores in near real-time, allowing for "rapid rescoring" and immediate dispute resolution.

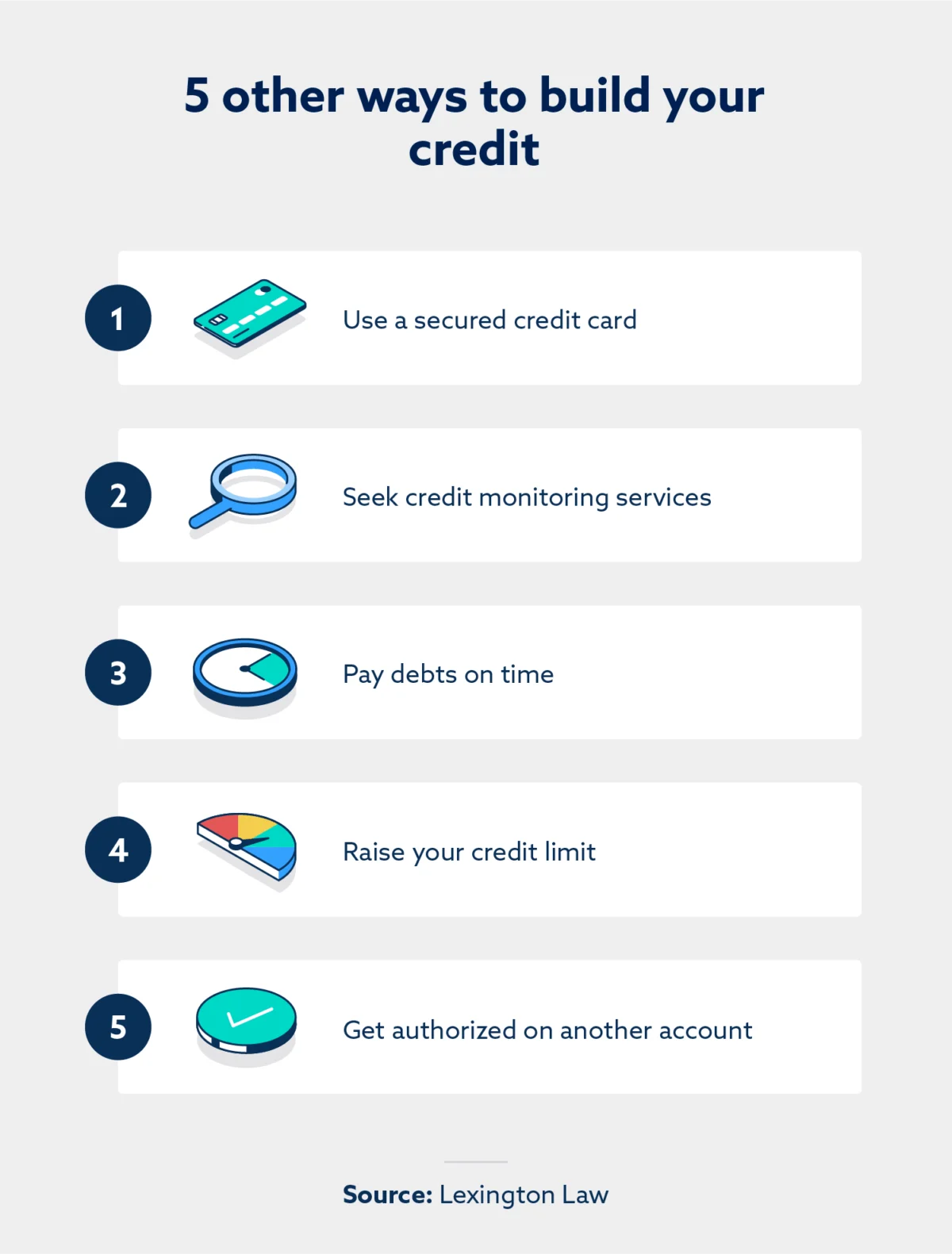

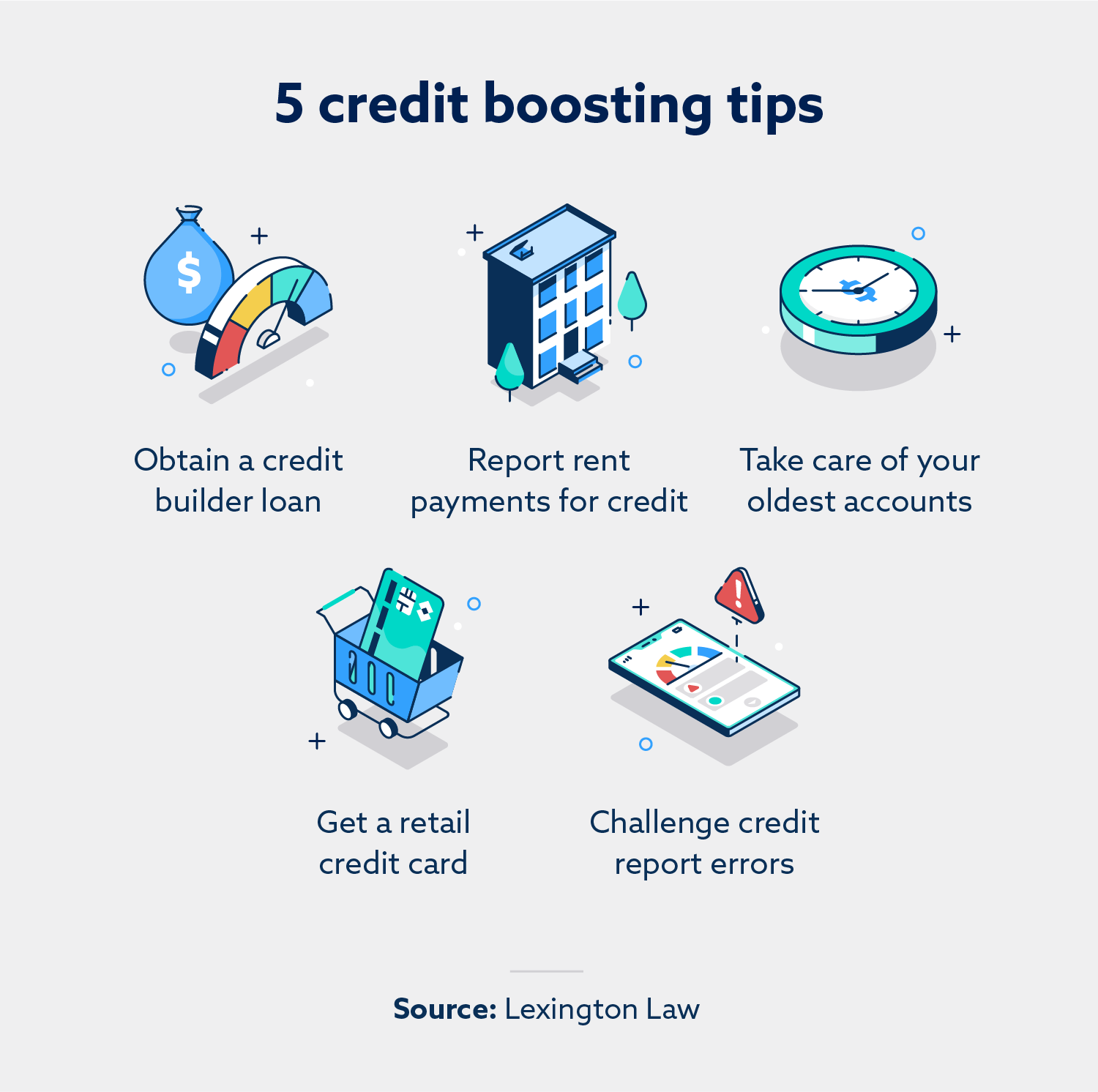

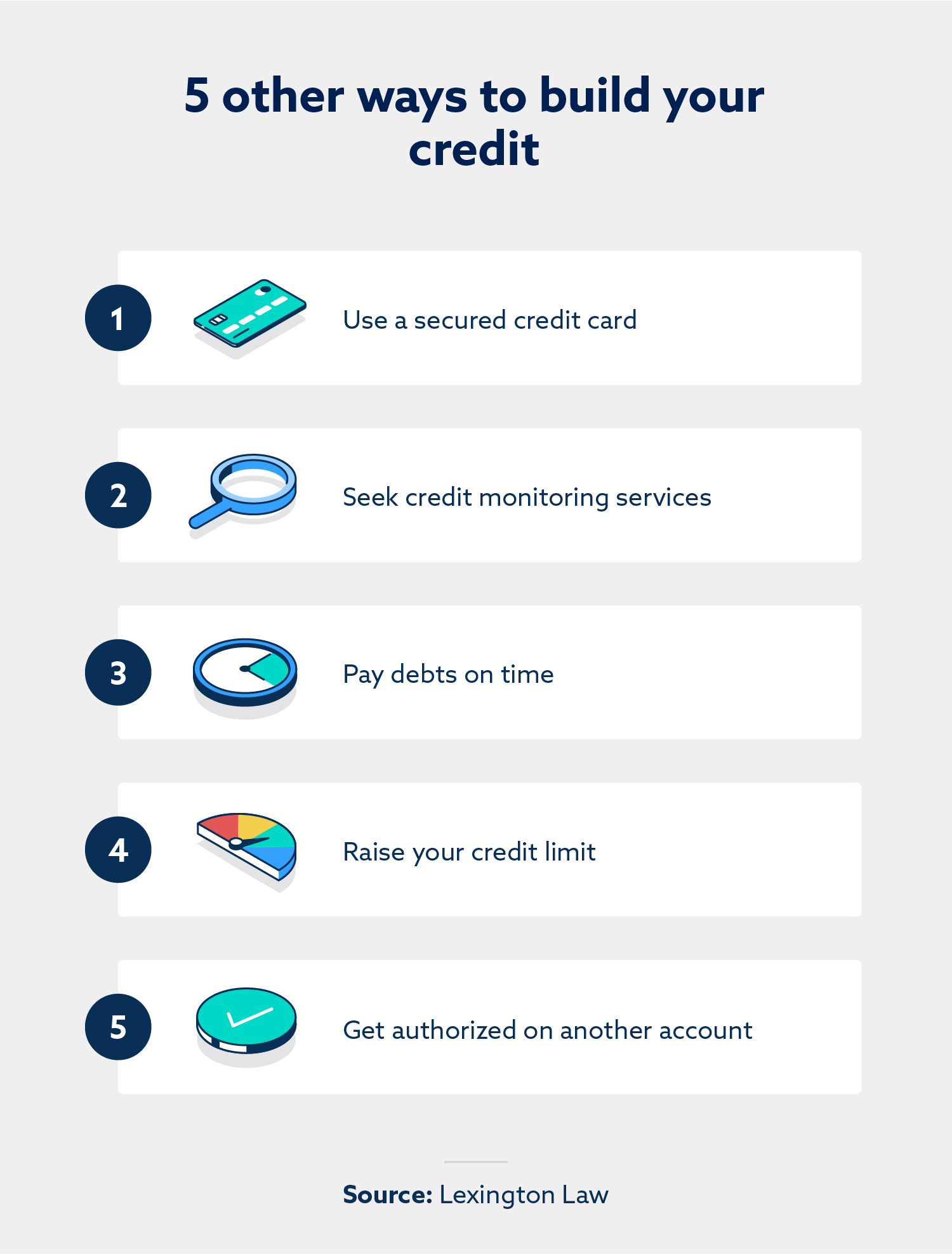

Supporting Data: 15 Strategic Methods to Build Credit Fast

For those seeking to optimize their profiles in the current market, the following 15 strategies represent the most effective levers available.

1. Credit Builder Loans

Unlike traditional loans, the proceeds of a credit builder loan are held in a secured account while the borrower makes payments. Once the term ends, the borrower receives the funds. This creates a documented history of on-time installment payments without the risk of the borrower overspending.

2. Rent Payment Reporting

For decades, rent was the largest monthly expense that didn’t help a credit score. In 2026, services that transmit rental data to Equifax, Experian, and TransUnion are essential for newcomers. This can establish a positive history in as little as 30 days.

3. Preservation of Account Longevity

The "Length of Credit History" accounts for 15% of a score. Consumers are often tempted to close old, unused cards to "clean up" their wallets. However, keeping these accounts open maintains the average age of the profile. Experts suggest asking issuers to waive annual fees rather than closing the account.

4. Strategic Use of Retail Cards

While store cards often carry higher interest rates, they frequently have lower barriers to entry. For a frequent shopper, these cards can provide a quick boost to the "total available credit" limit, provided the balance is paid in full every month to avoid interest charges.

5. Systematic Error Correction

Inaccuracies remain a systemic issue. A 2021 study by Consumer Reports found that more than one-third of consumers found errors in their credit reports. Professional firms, such as Lexington Law Firm, specialize in identifying these discrepancies—such as "zombie debts" or misreported late payments—and challenging them legally.

6. Secured Credit Cards

By providing a cash deposit as collateral, consumers can access a line of credit that behaves exactly like a traditional card. In 2026, many secured cards offer "graduation" paths, where the deposit is returned and the card becomes unsecured after six to twelve months of responsible use.

7. Holistic Credit Monitoring

Knowledge is a defensive tool. Modern monitoring services provide alerts for hard inquiries, new accounts, and changes in utilization. These services often include identity theft insurance, which has become vital in an era of increasing digital fraud.

8. Automation of Payments

With payment history being the heaviest weighted factor, a single 30-day late payment can drop a high score by over 100 points. Autopay is no longer a luxury; it is a fundamental requirement for credit maintenance.

9. Expansion of Credit Limits

By requesting a higher limit on existing cards, a consumer can instantly lower their credit utilization ratio. For example, a $500 balance on a $1,000 limit is 50% utilization. If the limit is raised to $2,000, that same $500 balance becomes 25% utilization, often resulting in an immediate score increase.

10. Authorized User Status ("Piggybacking")

By being added as an authorized user to a family member’s long-standing, high-limit account, a consumer can "inherit" that account’s positive history. This is one of the fastest ways for young adults to establish a score from scratch.

11. Student-Specific Credit Products

Banks in 2026 offer specialized cards for students that prioritize education and proof of enrollment over a lengthy income history. These products serve as an entry point into the banking ecosystem.

12. Rapid Rescoring for Mortgages

When a consumer is in the process of buying a home, they cannot wait 45 days for a bureau to update. Rapid rescoring services, usually initiated by a mortgage lender, can update a credit file within three to seven business days by providing proof of paid-off debts directly to the bureaus.

13. Professional Financial Advisory

The complexity of modern debt—including student loans, "Buy Now, Pay Later" (BNPL) services, and mortgages—often requires a tailored strategy. Financial advisors provide the context that automated apps cannot, helping consumers prioritize which debts to pay first for maximum score impact.

14. Credit-Building Applications

The rise of fintech has birthed apps that offer micro-lines of credit or report utility payments (gas, water, electricity) to the bureaus. These apps gamify the process, providing rewards for maintaining a high score.

15. Credit Builder Cards

Distinct from secured cards, these often function by linking to a user’s bank account and only allowing them to spend what they have, while reporting the activity as a line of credit. This eliminates the risk of debt accumulation while still building the "revolving credit" portion of the score.

Official Responses and Regulatory Context

The regulatory environment in 2026 has become increasingly protective of the consumer. The Consumer Credit Protection Act and subsequent amendments have mandated that credit reporting must be fair, accurate, and substantiated.

Officials from the Consumer Financial Protection Bureau (CFPB) have recently emphasized that "credit invisibility" is a form of economic exclusion. In response, the major bureaus—Equifax, Experian, and TransUnion—have launched initiatives to include "permissioned data." This allows consumers to opt-in to having their banking cash-flow data analyzed, which can help those with "thin" credit files prove their reliability.

However, the industry also warns against "credit repair" scams. Official guidance suggests that consumers should only work with reputable firms that follow the Credit Repair Organizations Act (CROA), which prohibits companies from making false claims or charging for services before they are performed.

Implications: The Long-term Value of Credit Mastery

The implications of an optimized credit score extend far beyond the ability to get a credit card. In 2026, credit scores are used by:

- Employers: During the hiring process for roles involving financial responsibility.

- Landlords: To determine security deposit amounts and lease eligibility.

- Insurance Companies: To calculate premiums for auto and homeowners’ insurance.

- Utility Providers: To decide whether to require a deposit for new service.

Furthermore, the "Cost of Credit" is a major driver of wealth inequality. A borrower with a 760 score may receive a mortgage rate 1.5% lower than a borrower with a 620 score. Over a 30-year loan on a $400,000 home, that 1.5% difference can amount to over $150,000 in interest.

In conclusion, building credit in 2026 is a multifaceted discipline. It requires a combination of foundational habits, the adoption of new fintech tools, and the occasional intervention of legal professionals to ensure the accuracy of one’s financial reputation. As the economy becomes increasingly digitized, the ability to curate and protect one’s credit profile remains one of the most critical components of modern financial literacy.