For four decades, the financial services industry has operated under a persistent, albeit flawed, paradigm: the "siloed" approach to retirement planning. Investors have been encouraged to treat their investment portfolios, their home equity, and their insurance products as separate entities, rarely integrating them into a cohesive strategy. However, as the demographic tide of an aging population rises and the costs of longevity skyrocket, this fragmented model is failing the "mass affluent"—those retirees who are too wealthy to qualify for immediate state assistance, yet too vulnerable to withstand the crushing costs of prolonged medical care.

Jerry Golden, a veteran innovator in the insurance and annuity space, argues that the time for a radical design shift is here. Having spent his career pioneering products like the "Accumulator"—an invention that provided downside protection for variable annuities and helped spawn a $1 trillion industry—Golden is now turning his attention to the most pressing crisis facing modern retirees: the intersection of inflation, healthcare costs, and the looming reality of a new federal Medicaid rule.

Main Facts: A New Regulatory Landscape

The retirement planning landscape is bracing for a significant shift in 2028. A new federal Medicaid rule will establish a hard cap on allowable home equity for those seeking long-term care (LTC) coverage under Medicaid, limiting it to $1 million. Unlike previous state-by-state regulations, which often adjusted for inflation and allowed for higher equity thresholds, this federal mandate will apply across the board (with the exception of farm families) and will not be indexed to inflation.

For middle-class homeowners in high-cost-of-living areas, this creates an existential threat. If your primary asset—your home—is valued above the $1 million threshold, you will effectively be disqualified from Medicaid LTC coverage unless you liquidate or restructure your assets. This policy change threatens to force many seniors to sell their homes prematurely, incurring significant transaction costs, tax liabilities, and the emotional trauma of leaving their communities.

Chronology: The Path to "HomeEquity2Income"

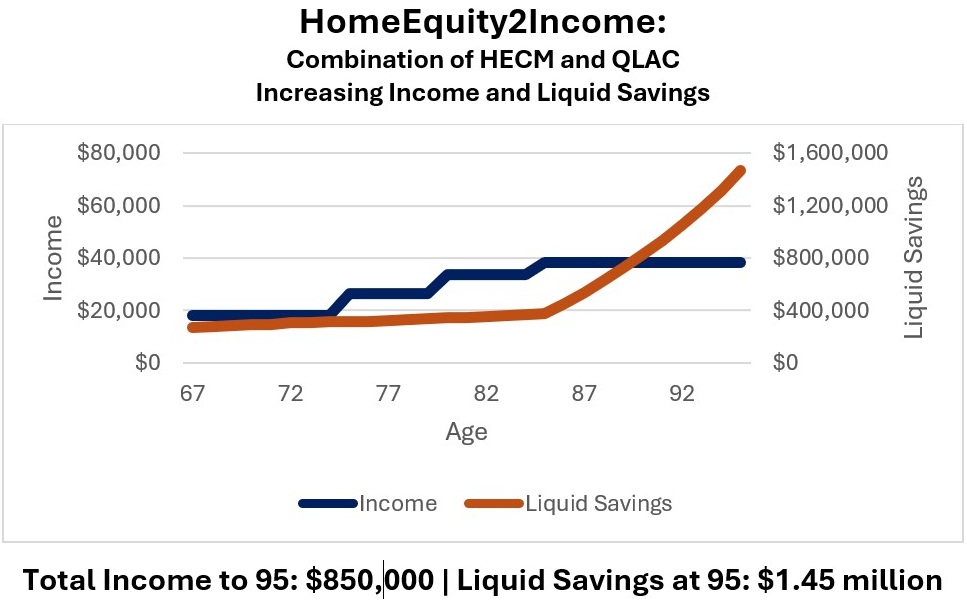

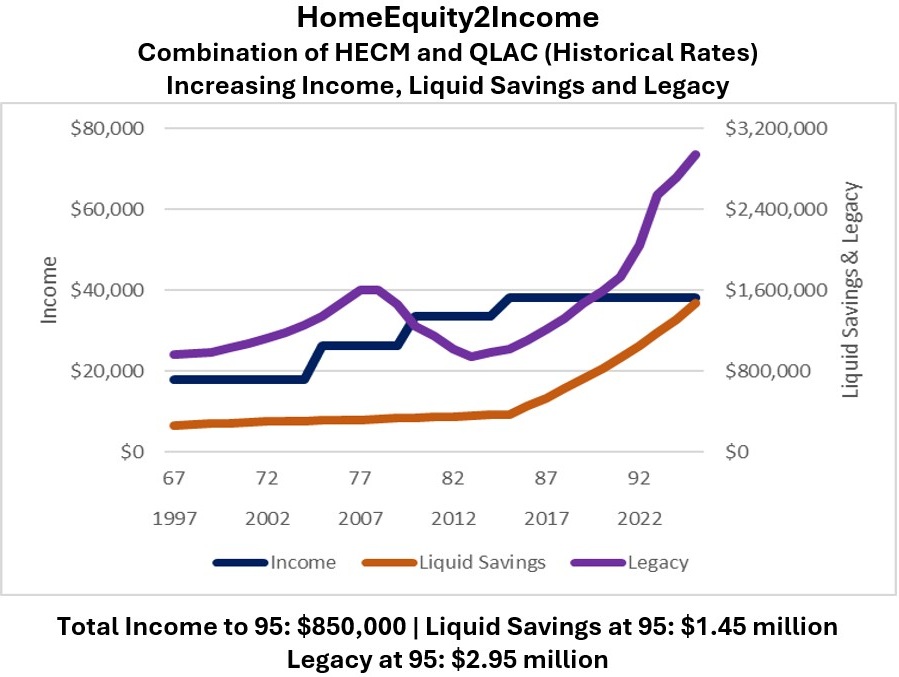

The development of a new strategy, dubbed "HomeEquity2Income" (H2I), is the result of years of analyzing the gaps in traditional retirement planning. The methodology is not a new product, but rather a new design—a strategic integration of existing tools.

- 1980s–2010s: The era of the annuity boom. Products were designed to provide income, but often at the expense of liquidity. The "4% rule" became the standard, yet failed to account for the catastrophic risks of long-term care.

- 2020–2024: Rising inflation and medical costs exposed the fragility of the 4% withdrawal strategy. Meanwhile, the U.S. government began tightening the net on Medicaid qualification, leading to the 2028 home equity cap announcement.

- The Present: The emergence of H2I. By recognizing that housing wealth often represents 50% of a retiree’s net worth, planners are now moving toward a model where home equity is treated as a core investment asset rather than a "dead" resource.

Supporting Data: Why the Old Ways Fail

Retirement is no longer just about investment returns; it is about risk management. Data from the U.S. Department of Health and Human Services (HHS) suggests that 50% of individuals aged 85 and older will require some form of long-term care services. With annual costs for such care ranging between $80,000 and $150,000, and rising at an historical rate of 3% to 5% annually, a standard $2 million portfolio—split between a home and an IRA—can be depleted in less than a decade if a health event occurs.

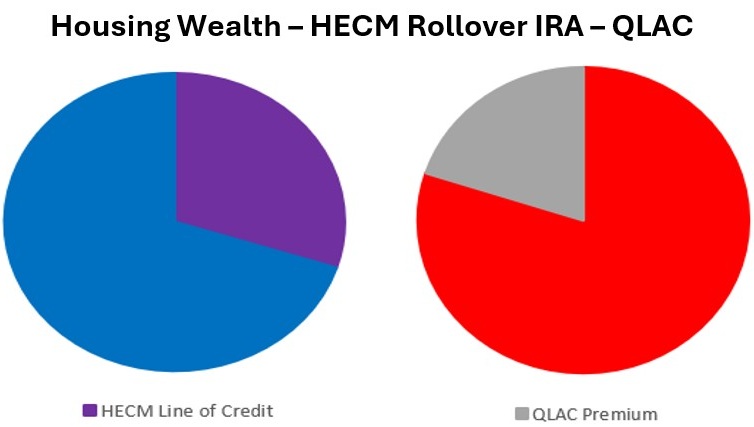

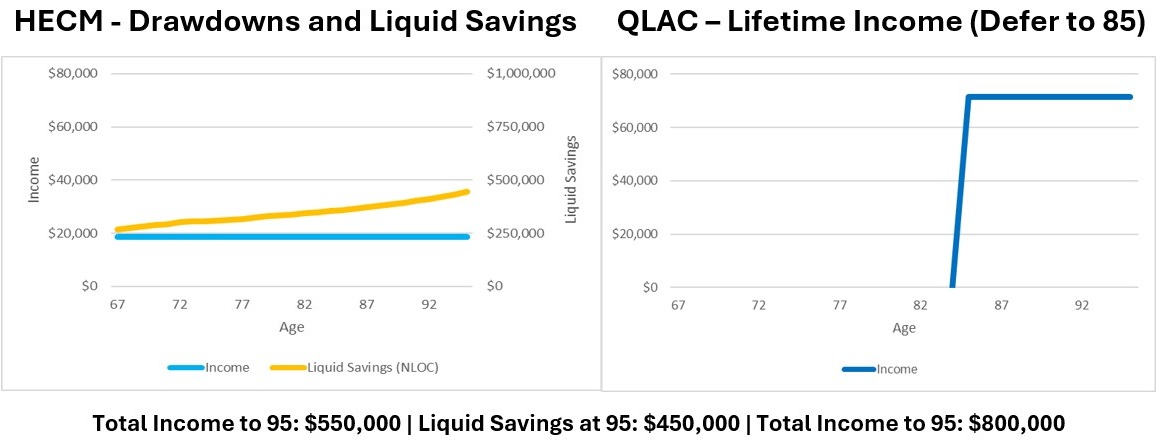

Traditional portfolios, which rely on withdrawing 4% to 5% annually, often fail to account for the "sequence of returns" risk or the sudden, massive liquidity demands of nursing home care. By integrating a Home Equity Conversion Mortgage (HECM) with a Qualified Longevity Annuity Contract (QLAC), the H2I strategy allows retirees to:

- Unlock Liquidity: Use the HECM line of credit to create a cash buffer.

- Ensure Longevity: Use the QLAC to defer taxes and provide a guaranteed income floor that starts at a later, predetermined age.

- Protect the Legacy: Avoid the forced sale of the home by leveraging its equity to cover the cost of care, thereby preserving other assets for heirs.

Official Responses and Industry Perspectives

While the financial industry has traditionally viewed reverse mortgages (HECMs) with skepticism, often citing high fees and the risk of borrowing too much, the H2I framework changes the narrative. It reframes the HECM not as a "last resort" loan, but as a sophisticated financial management tool.

Similarly, the QLAC has been historically underutilized. By pairing it with a HECM, the strategy addresses the primary objection to both products: the lack of liquidity. When used together, they create a synthetic "safety net." Financial advisers who adopt this algorithmic approach are reporting that retirees feel more secure, knowing they do not have to "spend down" their IRA to qualify for care, nor do they need to surrender their lifestyle to meet strict Medicaid means tests.

Implications for the Future of Retirement

The implications of this shift are profound. For the "mass affluent," the ability to "age in place" while maintaining a steady, tax-efficient income is the ultimate goal. The H2I approach suggests that the solution to the retirement crisis is not necessarily higher investment returns, but better asset management and coordination.

Breaking Down the Silos

The core of this new philosophy is the breakdown of the barriers between three traditionally separate domains:

- Investment Portfolios: Usually managed by stockbrokers or robo-advisors.

- Annuity Products: Often sold by insurance agents with little regard for the client’s home equity.

- Housing Wealth: Often ignored by financial planners until the client is in crisis.

By integrating these three pillars, the H2I model allows for a higher starting income—often reaching upwards of $130,000 to $170,000 for a retiree with a $2 million total net worth, including home value.

Long-Term Care Scenario Testing

In a series of stress tests, the H2I model demonstrates resilience against various long-term care scenarios. Whether the retiree requires a home aide for five years or needs to move into an assisted living facility, the H2I strategy provides the necessary cash flow to cover these expenses without liquidating the primary portfolio at a loss.

Furthermore, the strategy addresses the tax implications of retirement. By using a QLAC, retirees can defer taxable distributions from their IRAs, potentially lowering their annual tax bill during the early years of retirement—a critical factor in maintaining the longevity of their savings.

The Verdict: A Proactive Approach

The message to retirees is clear: the 2028 Medicaid rule is a wake-up call. Relying on government safety nets is becoming increasingly difficult, and the "set it and forget it" investment approach is insufficient for the current economic reality.

Instead of waiting for a crisis, retirees should consider "stacking their building blocks." This means:

- Assessing the total net worth: Include the home as a vital component of the income-generating machine.

- Using Algorithms: Rely on data-driven planning rather than rules of thumb.

- Executing with Purpose: Partner with advisers who understand the intersection of insurance, housing wealth, and investment strategies.

As the financial landscape continues to evolve, the distinction between those who successfully navigate their later years and those who struggle will be defined by their ability to adapt. The H2I model, by shifting the focus from mere wealth accumulation to strategic wealth deployment, offers a blueprint for a more stable, secure, and dignified retirement.

Disclaimer: This article is intended for educational purposes and reflects the views of the contributor. Retirement planning is highly individualized; readers are encouraged to consult with certified financial advisers and review their specific circumstances against current SEC and FINRA standards. For further details on how to build a personalized plan, visit resources like Go2Income.