By Financial Correspondent

The traditional narrative of the "American Dream"—one defined by upward mobility achieved solely through individual grit and hard work—is facing a profound reckoning. As the cost of living outpaces wage growth and housing prices reach historic highs, a new study suggests that financial success in modern America is increasingly tied to the "Bank of Mom and Dad" rather than just professional merit.

A comprehensive survey of 1,000 Americans conducted by Lexington Law Firm has unveiled a stark reality: the path to wealth is no longer a level playing field. From the delayed independence of Gen Z to the pessimistic outlook of high-earning Gen Xers, the data paints a picture of an economy where generational timing and parental support are the primary architects of financial stability.

Main Facts: The Correlation Between Inheritance and High Earnings

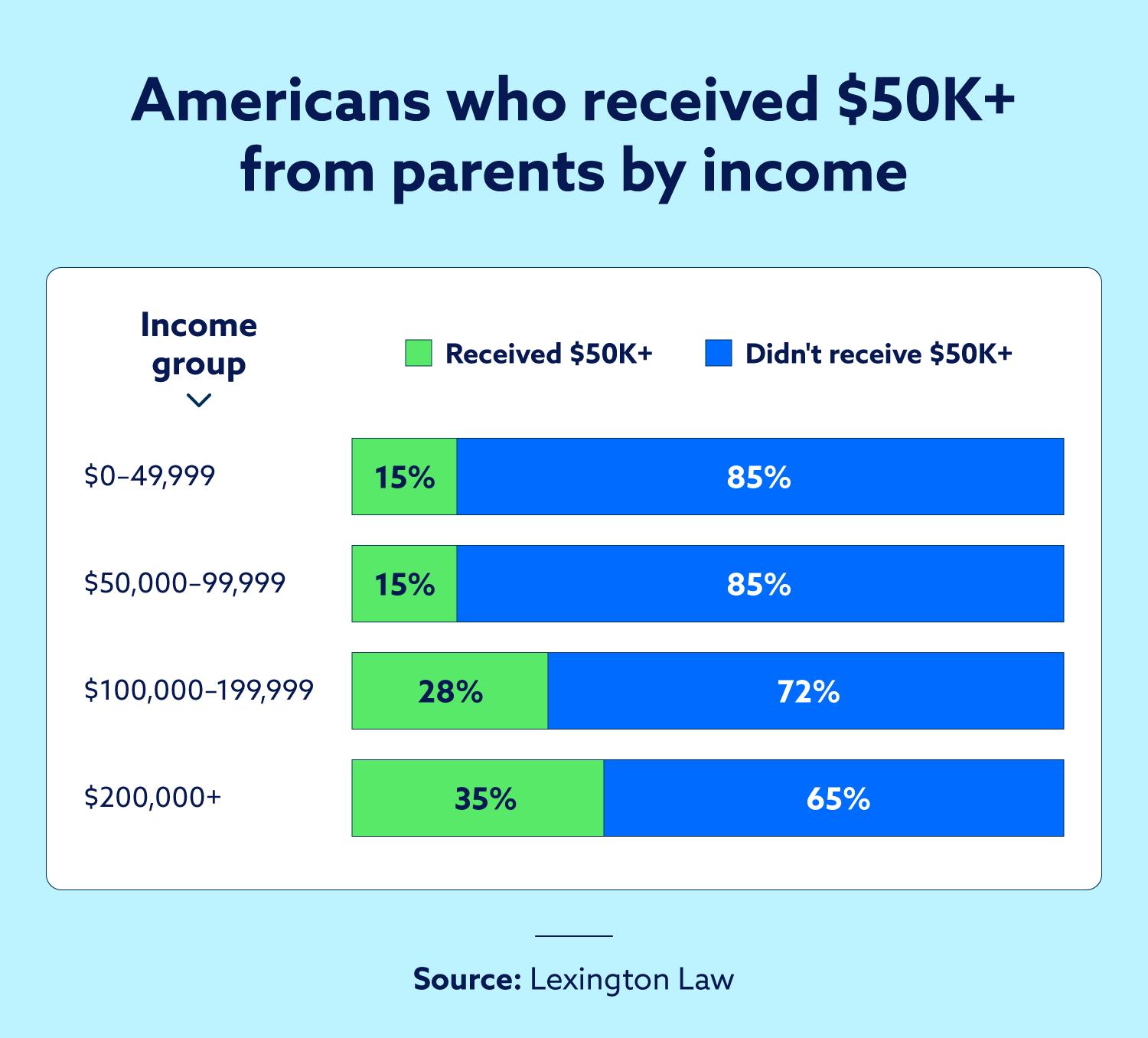

The most striking revelation from the report challenges the long-standing archetype of the "self-made" high earner. While many individuals in the top income brackets credit their success to personal initiative, the data suggests a significant correlation between high annual earnings and early-life financial infusions.

According to the survey, individuals earning $125,000 or more per year are 2.5 times more likely to have received substantial financial assistance from their parents compared to lower-income earners. Specifically, 36 percent of these high earners received $50,000 or more in parental support, whereas only 14 percent of those in lower income brackets could say the same.

This "head start" often manifests in critical life milestones, such as the ability to graduate debt-free or secure a down payment on a first home. For those without this safety net, the climb toward financial freedom is not just steeper—it is often delayed by decades. The survey found that more than half of Americans (53 percent) received $10,000 or less from their families, highlighting a growing "support gap" that dictates long-term wealth trajectories.

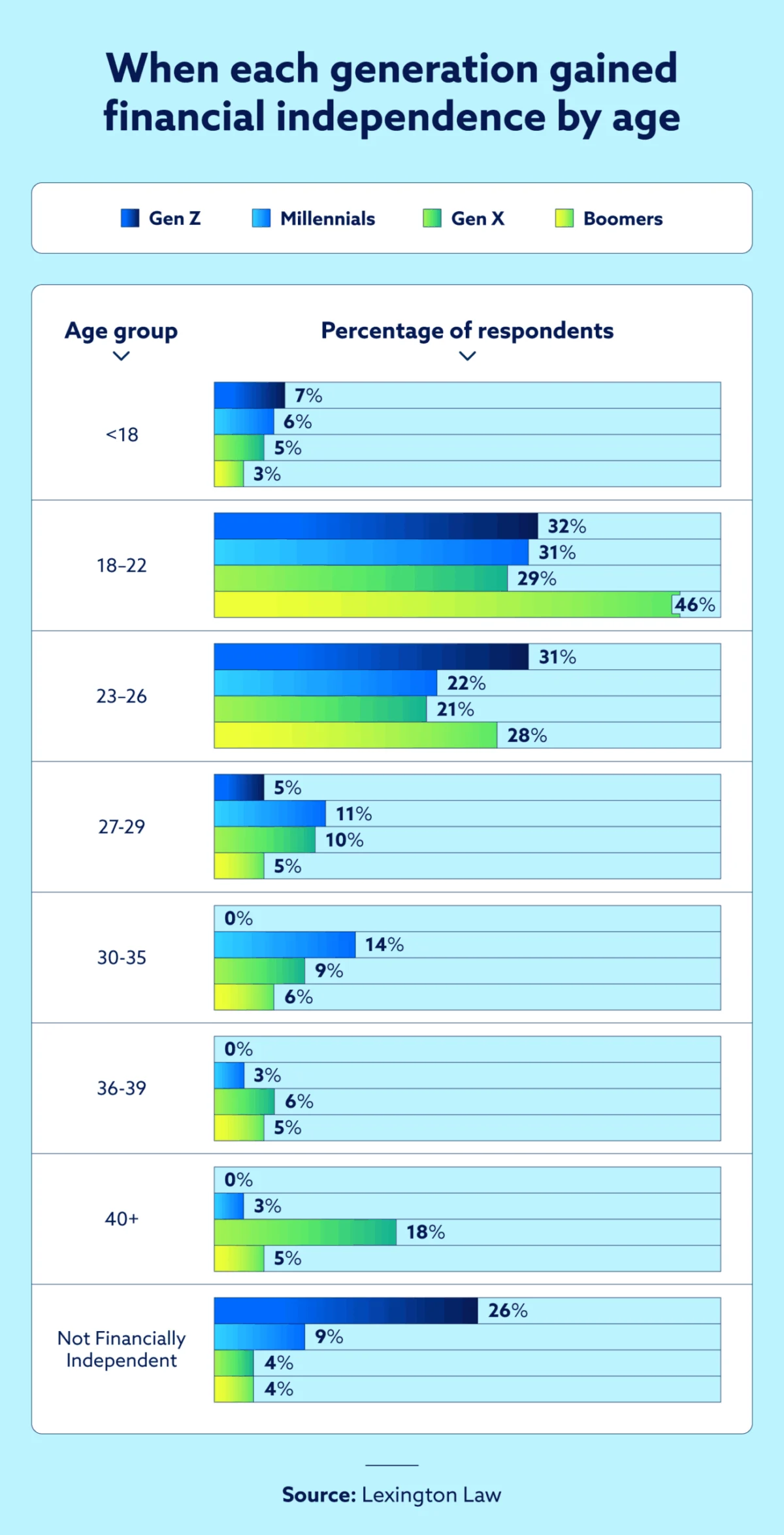

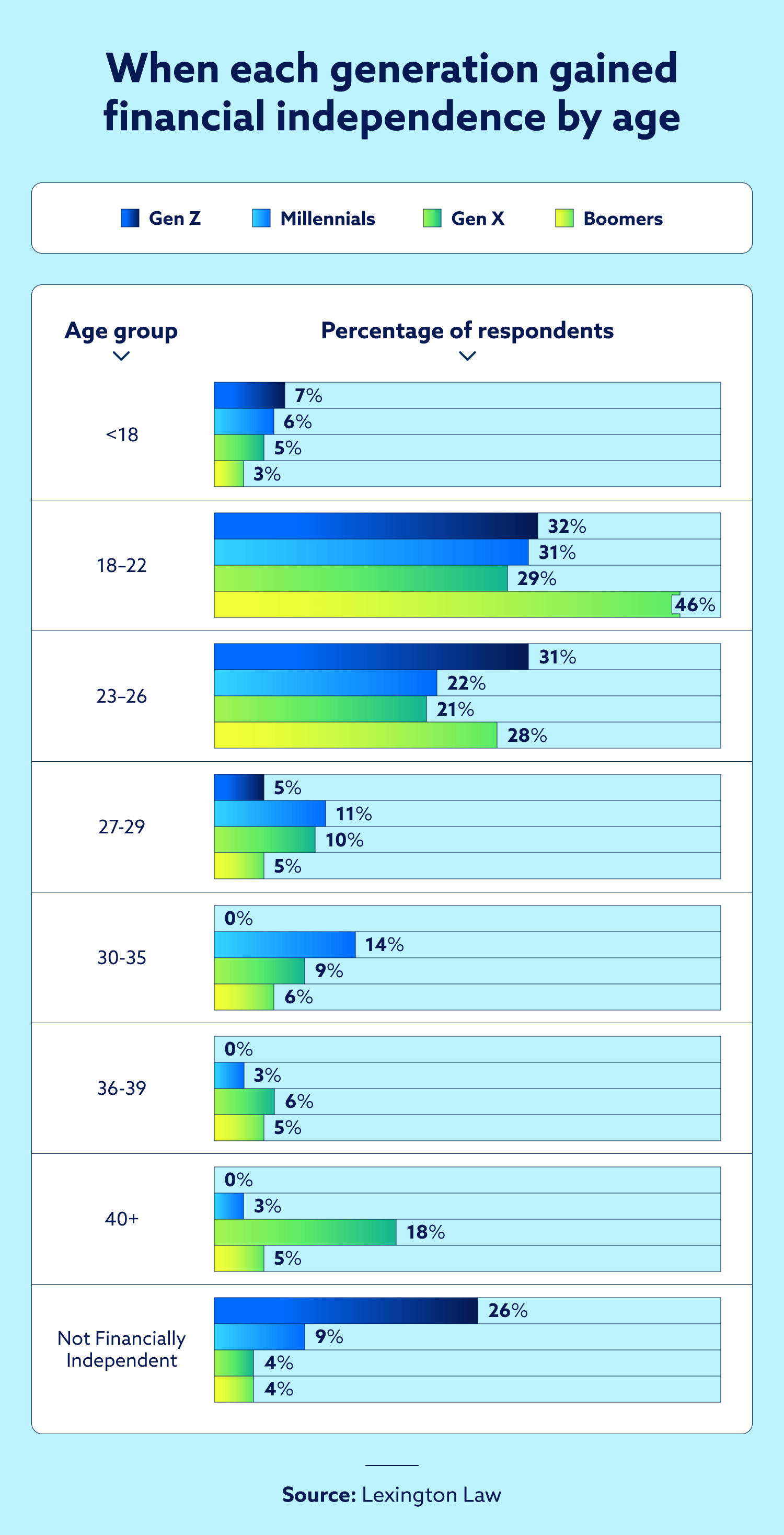

Chronology: The Shifting Timeline of Financial Independence

To understand the current crisis, one must look at the chronological shift in how and when Americans achieve financial autonomy. The survey highlights a dramatic departure from the economic conditions enjoyed by the Baby Boomer generation compared to the reality facing Gen Z and Millennials today.

The Boomer Era: A Fast Track to Autonomy

In the mid-20th century, the roadmap to independence was relatively short. Nearly half of Baby Boomers (48 percent) reported reaching full financial independence by the age of 22. This early start allowed for decades of compounding interest in retirement accounts and the accumulation of home equity during periods of lower relative housing costs.

The 2008 Pivot and the Rise of the "Boomerang" Generation

The 2008 financial crisis served as a pivotal moment that permanently altered the timeline for Gen X and older Millennials. The survey notes that 36 percent of Gen Xers did not achieve financial independence until after age 30. This delay was further exacerbated by the stagnation of wages in the decade following the Great Recession.

The Modern Era: Delayed Launch as the New Normal

Today, the timeline has shifted even further. Only 36 percent of Gen Z respondents reached financial independence between the ages of 23 and 29. More telling is that 26 percent of Gen Zers remain financially reliant on their parents well into their late 20s. This is not merely a matter of "failure to launch"; rather, it is a structural response to an economy where entry-level wages have failed to keep pace with the 20 percent surge in the cost of living seen over the last four years.

Supporting Data: A Generational Heatmap of Financial Anxiety

The Lexington Law survey provides a granular look at how different age groups perceive their obstacles and their futures. The results show that while every generation faces challenges, the nature of those challenges varies significantly.

Gen X: The High-Earning Pessimists

Gen X currently holds the title of the highest-earning generation, with 54 percent reporting annual incomes over $100,000. They also reported the highest levels of historical parental support, with 23 percent having received over $50,000. Despite this, Gen X maintains the bleakest outlook. Nearly half (49 percent) are pessimistic about their financial future over the next 10 years. This pessimism likely stems from their position as the "sandwich generation," simultaneously funding their children’s education while managing the healthcare costs of aging Boomer parents.

Gen Z: The Optimistic Realists

In a surprising paradox, Gen Z remains the most optimistic generation despite acknowledging that the cards are stacked against them. An overwhelming 87 percent believe they will eventually be as successful as, or more successful than, their parents. Yet, 72 percent of these same respondents believe the current economic system is "rigged" in favor of older generations. This suggests a generation that is hyper-aware of systemic flaws but maintains a resilient belief in their own ability to navigate them.

The Universal Obstacle: Cost of Living

When asked to identify the primary roadblock to building wealth, there was a rare moment of cross-generational consensus.

- 73% cited the rising cost of living (groceries, gas, utilities) as the #1 obstacle.

- 65% pointed to housing costs, which have outpaced inflation in nearly every major U.S. market.

- 49% identified stagnant wages as a critical barrier.

- 62% of Boomers specifically cited healthcare costs as their primary concern, highlighting the fragility of wealth in the face of medical inflation.

Official Responses and Economic Context

The findings of the Lexington Law survey align with broader data from federal agencies, providing a sobering context for the individual sentiments expressed by respondents.

The U.S. Bureau of Labor Statistics (BLS) recently confirmed that the Consumer Price Index (CPI) has surged by more than 20 percent since 2021. While nominal wages have risen, "real wages"—inflation-adjusted earnings—have struggled to maintain the same velocity. This creates a "treadmill effect" where workers earn more but can afford less.

Furthermore, the U.S. Department of the Treasury has released reports indicating that young adults today are significantly more likely to rely on family resources than previous generations. The Treasury attributes this to the "triple threat" of high student loan debt, a lack of affordable entry-level housing, and the increased educational requirements for middle-class jobs.

The U.S. Federal Reserve’s latest report on the Economic Well-Being of U.S. Households echoed these sentiments, noting that housing costs have become the primary driver of financial fragility. The Fed’s data suggests that for those earning between $125,000 and $200,000, financial independence is often delayed until age 35 or 40 precisely because of the debt-to-income ratios required to live in high-productivity urban centers.

Implications: The Future of the American Middle Class

The implications of this generational wealth gap extend far beyond individual bank accounts; they suggest a fundamental shift in the American social contract.

The Erosion of Social Mobility

If the primary predictor of high earnings is a $50,000 parental "gift," the United States risks moving toward a more stratified, inheritance-based economy. This "hereditary meritocracy" makes it increasingly difficult for those from lower-income backgrounds to break into the upper-middle class, regardless of their education or work ethic.

The Credit Imperative

As parental support becomes a prerequisite for traditional wealth-building milestones like homeownership, those without family wealth must rely more heavily on credit. The survey underscores that for the "non-inherited" class, maintaining a pristine credit report is not just a financial chore—it is a vital survival tool. In an economy where you cannot rely on a parental down payment, your ability to access low-interest capital becomes the only viable lever for upward mobility.

The Political and Social Tensions

The fact that 72 percent of the youngest workforce feels the system is "rigged" suggests a looming period of political volatility. As Gen Z and Millennials become the dominant voting bloc, we can expect increased pressure for policies addressing housing affordability, student debt relief, and wealth redistribution.

Conclusion

Building wealth in 21st-century America is no longer a simple matter of working hard and saving. It is a complex navigation of rising costs, generational timing, and family infrastructure. While the optimism of the youth remains a glimmer of hope, the data suggests that unless systemic issues—specifically housing and the cost of living—are addressed, the "generation gap" in wealth building will only continue to widen, leaving the American Dream as an exclusive inheritance for the few rather than a possibility for the many.