For the average American consumer, the price of a six-pack or a pint at a local brewery appears straightforward—a simple exchange of currency for a product. Yet, beneath the surface of every retail transaction lies a labyrinthine regulatory and fiscal framework that shapes the price, availability, and production of beer across the United States. As we move into 2026, the intersection of shifting consumer habits, economic pressures, and arcane state-by-state tax policies has created a challenging environment for both brewers and drinkers.

The Architecture of Beer Taxes: More Than Meets the Eye

When a consumer pays for a beer, the price they see is rarely the price of production and profit alone. Instead, it is an aggregate of manufacturing costs, distribution logistics, and a heavy, often invisible, layer of excise taxes. Unlike sales taxes, which are clearly itemized on a receipt, beer excise taxes are generally levied at the point of manufacture or wholesale. Consequently, these costs are "baked into" the final retail price, leaving the average consumer largely unaware of the extent to which government policy influences their beverage of choice.

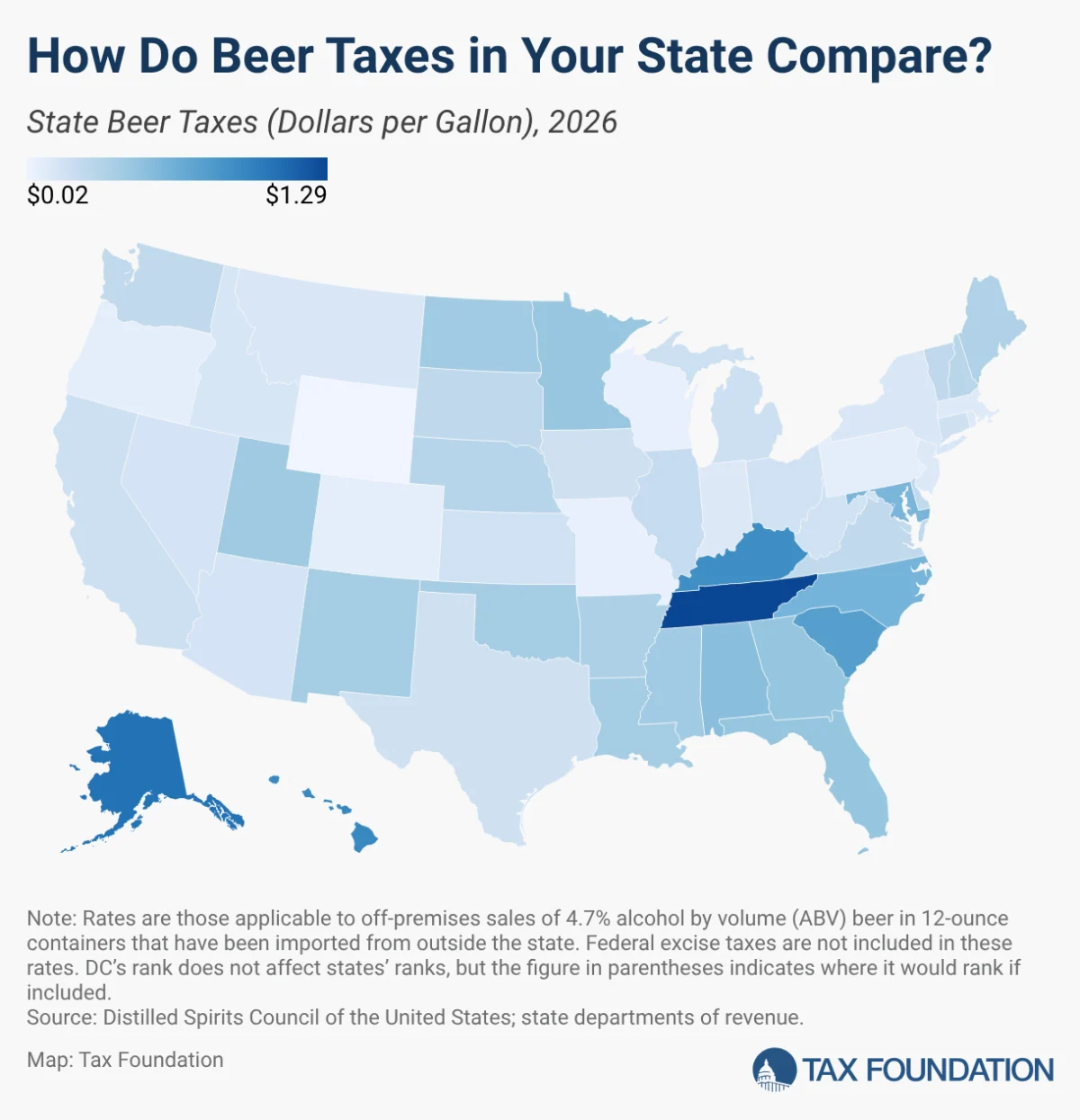

At the core of this complexity is the fact that beer taxes are rarely uniform. While there is a federal excise tax, the true volatility exists at the state and local levels. The tax rate for a standard 12-ounce container of beer (based on a 4.7% alcohol by volume, or ABV) varies wildly across the map. In 16 states, these rates are not flat; they are dynamic, shifting based on factors as disparate as the place of production, the size of the container, the specific alcohol content, and even the type of establishment where the purchase occurs.

Chronology of Regulatory Shifts and State-Level Maneuvering

The landscape of 2026 is defined by a series of legislative actions that have altered the fiscal geography of the industry over the past few years.

- 2023–2024: The Push for Local Autonomy: Several states, looking to bolster municipal budgets, moved to grant local governments more power to levy "supplemental" alcohol taxes. This led to a patchwork of local surcharges, such as the 5% additional sales tax on alcohol implemented by the Municipality of Anchorage.

- 2025: The Rise of Domestic Incentives: Recognizing the economic hardship faced by craft breweries due to rising tariff costs and supply chain instability, states like Missouri took legislative action. By cutting taxes on beer manufactured within state-recognized American breweries to as low as $0.02 per gallon, Missouri signaled a pivot toward protectionist fiscal policy intended to insulate local industries from global economic headwinds.

- 2026: The Modernization Debate: As we enter 2026, the conversation has shifted from mere tax collection to structural reform. Policy analysts and industry advocates are increasingly calling for the abandonment of the "categorical" system—which treats beer, wine, and spirits as distinct entities—in favor of a neutral, ABV-based taxation model.

Supporting Data: A State-by-State Breakdown

The lack of uniformity in taxation creates a "tax border" effect. For instance, Virginia maintains a tiered system where the tax burden shifts significantly depending on container size—distinguishing between bottles under 7 ounces, those up to 12 ounces, and those exceeding 12 ounces. This requires retailers and distributors to manage complex inventory tracking systems just to comply with local regulations.

Idaho presents a different regulatory hurdle. The state enforces a "triple tax" threshold for products exceeding 5% ABV. By statutorily reclassifying higher-alcohol beers to match the tax treatment of wine, the state effectively raises the tax from $0.15 per gallon to $0.45 per gallon. This creates a significant "cliff" for craft brewers who specialize in IPAs or stouts that naturally exceed the 5% threshold, forcing them to either absorb the cost or pass it on to consumers, potentially pricing them out of the market.

Furthermore, some jurisdictions have moved toward "uniform local taxes." Alabama and Georgia, for example, have implemented statewide uniform local taxes that add approximately 50 cents per gallon to every beer sale. These fees are in addition to state-level excise taxes and any municipal sales taxes, creating a triple-layered tax stack that significantly inflates the cost of a standard beverage.

Official Responses and Industry Sentiment

The brewing industry, represented by groups such as the Brewers Association, has sounded the alarm regarding the sustainability of the current model. The industry is currently grappling with a "perfect storm" of challenges: tariff-related cost increases on aluminum and raw materials, combined with a cultural shift toward "sober-curious" lifestyles.

"The 2025 year in beer was defined by resilience, but also by the realization that current tax structures are becoming untenable," notes one industry analyst. "When you pair a decline in per-capita consumption with taxes that don’t account for the reality of modern brewing innovation, you create a squeeze that hurts smaller, independent brewers the most."

Policymakers, however, remain divided. Some argue that excise taxes serve as a necessary tool to manage public health and generate essential revenue for state general funds. Others, such as those advocating for the Tax Foundation’s modernization proposals, argue that the current categorical system is "arcane." They contend that by moving to a system that taxes based strictly on the actual alcohol content, states could achieve greater neutrality, simplify compliance for businesses, and reduce the distortions caused by outdated statutory categories.

Implications: The Risks of an Outdated Model

The reliance on beer taxes as a primary revenue stream presents a long-term danger for state governments. There are two primary risks inherent in the current structure:

- The Erosion of Ad Quantum Value: Taxes levied on volume (the amount of liquid) lose their real-world value over time due to currency debasement and inflation. If a state sets a tax of 10 cents per gallon, that dollar amount buys less public service today than it did a decade ago.

- The Volatility of Ad Valorem Taxes: Taxes based on value (price) are highly susceptible to market shifts. As younger consumers move toward low- or no-alcohol options, the total market value of beer sales may stagnate or decline. States that have tethered their budget projections to the steady growth of alcohol tax revenue may find themselves facing significant, unforeseen budget gaps in the coming years.

Conclusion: The Path Toward Reform

As 2026 progresses, the beer industry stands at a crossroads. The existing system is a product of post-Prohibition era thinking, designed for an era when the market consisted of a few large domestic producers and standardized products. Today’s market—characterized by diverse craft offerings, varying alcohol levels, and changing consumer preferences—simply does not fit into those 20th-century boxes.

For policymakers, the path forward requires a fundamental rethink of what these taxes are intended to achieve. If the goal is revenue, the current system is becoming inefficient and unpredictable. If the goal is social management, the current system is often arbitrary, penalizing certain product categories while leaving others untouched.

Modernizing the system by transitioning to a simplified, ABV-based tax framework would not only benefit the industry by reducing the administrative burden of compliance, but it would also provide a more stable and logical revenue stream for the state. As the industry continues to evolve, the framework governing it must be nimble enough to keep pace. For the consumer, understanding this hidden tax landscape is the first step in recognizing the true cost of their favorite drink—and perhaps, the first step in demanding a more equitable system.